Form 990 for Christians is not merely a compliance document. It is one of the few standardized windows a donor has into how a ministry governs itself, compensates leaders, describes results, and handles conflicts of interest. Scripture assumes that those who handle sacred gifts must do so in a way that is both faithful and publicly defensible. Paul’s concern was not only that funds be handled honestly, but that they be handled “honorably” in the eyes of others (2 Corinthians 8:20–21).

That is the right frame for the Form 990: not suspicion, and not naïve trust, but sober stewardship. Christian donors routinely face two pressures at once. The first is moral urgency: the needs are real, and delay feels like disobedience. The second is information asymmetry: ministries know far more about themselves than donors can know. The Form 990 does not solve that asymmetry, but it can narrow it.

The harder question is how to read the 990 without misreading it. Some donors treat a single number as a proxy for faithfulness. Others treat the form as legalese and ignore it entirely. Both approaches fail mature Christian stewardship. The goal is to read the 990 as one piece of verifiable evidence, interpreted with theological seriousness, financial literacy, and a clear view of governance.

Why the Form 990 matters for Christian stewardship

Christian giving is never only transactional. We are offering resources entrusted by God for the good of neighbors and the witness of the church. That means donors cannot reduce due diligence to “How inspiring is the story?” or “How famous is the leader?” Scripture repeatedly warns against partiality and the kind of credulity that confuses charisma with character (Proverbs 14:15; James 2:1–4).

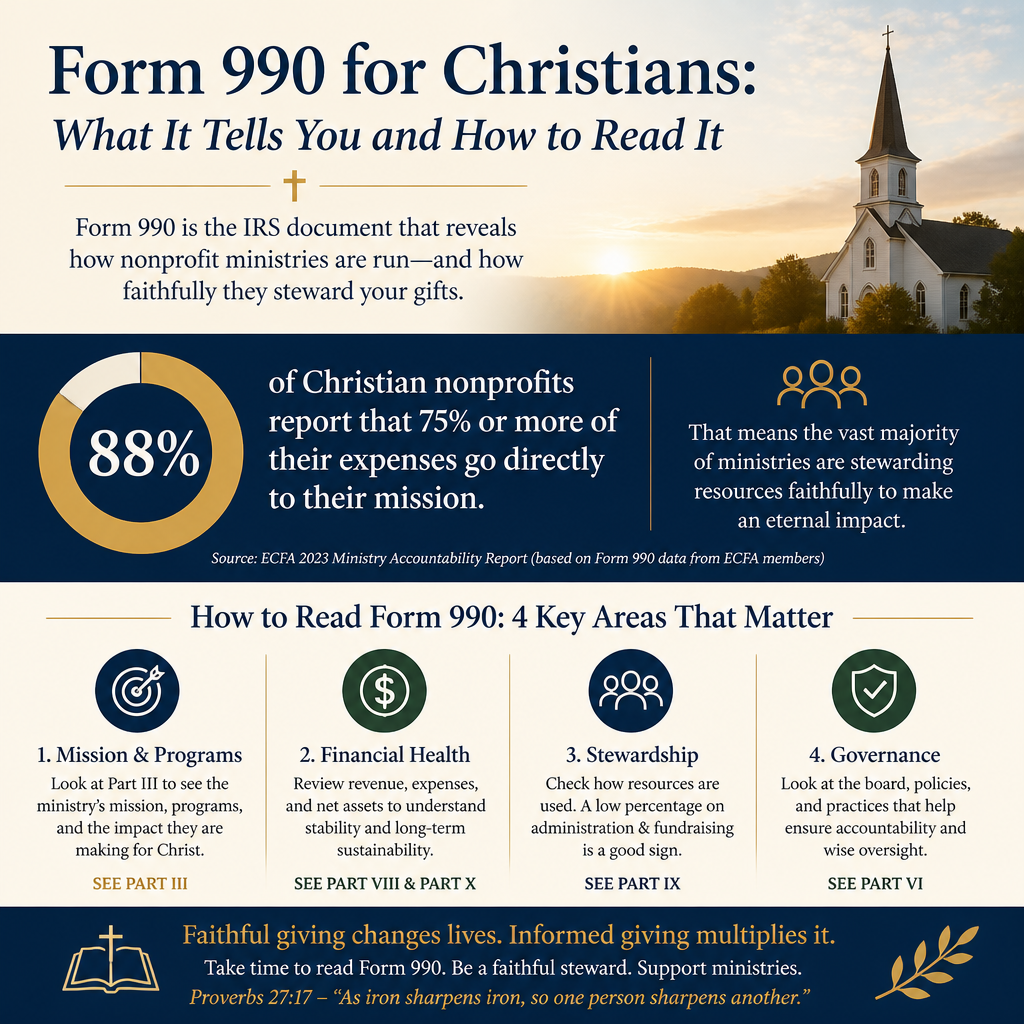

For many U.S. ministries, the Form 990 is the closest thing to an audited, comparable disclosure that donors can access. Most organizations recognized as tax-exempt under section 501(c)(3) must file an annual information return with the IRS, though there are meaningful exceptions. Churches and many church-affiliated entities are not required to file, and smaller nonprofits may file a simplified version. Those limitations matter because “no 990” is not automatically a red flag; in some cases it is a normal result of legal classification.

What the 990 can do, consistently, is surface patterns that correlate with trustworthy operations: independent governance, clear conflict-of-interest processes, a disciplined approach to compensation, defensible financial statements, and a posture of transparency. These are not secular add-ons to ministry. They are practical expressions of the biblical demand that those entrusted with resources be “found faithful” (1 Corinthians 4:2).

A common donor fear is that scrutiny will undermine generosity. Yet the New Testament treats careful administration as an ally of generosity, not its enemy. Paul organized collections with multiple accountable handlers precisely to protect the integrity of the gift and the reputation of the gospel (2 Corinthians 8:18–21). A 990 is one of the modern tools that helps donors approximate that same integrity from a distance.

How the Form 990 is built and what it can and cannot tell you

The Form 990 is structured as a blend of narrative disclosures, governance and policy questions, and summarized financial statements. It is designed for regulators, but it is also designed to be read by the public. Donors should treat it as a high-level map: it points to where deeper questions may be warranted, but it rarely provides the entire story by itself.

The 990 is standardized, but not standardized enough

The primary value of the 990 is consistency: most filers report similar categories in similar places. The primary weakness is that nonprofit accounting has room for judgment calls. Two faithful ministries can categorize expenses differently while pursuing similar work. That is why simplistic comparisons—especially across very different ministry models—often mislead.

For example, a ministry that funds local churches and indigenous leaders may show a high proportion of “grants and assistance,” while a ministry that operates a U.S.-based counseling center may show higher personnel costs. Neither pattern is automatically virtuous or suspect. The question is whether the pattern matches the ministry’s stated mission, and whether governance and controls make misclassification less likely.

The 990 is about governance, not only money

Donors often approach the 990 as a financial ratio exercise. Yet the most revealing parts are frequently the governance disclosures: independent board oversight, conflicts of interest, whistleblower processes, document retention, and whether the board reviews the form before it is filed. These details are mundane, and that is precisely why they matter. Mature integrity tends to show up in the mundane.

The 990 is limited by timing and context

A Form 990 is backward-looking and typically published months after a fiscal year ends. It will not capture current developments, emerging crises, or rapid growth pains. It also will not tell you whether a ministry’s theology is orthodox or whether its discipleship is sound. Those are theological questions that require other evidence: doctrinal statements, church accountability, and the fruit of ministry over time.

Still, a ministry that insists it is above financial disclosure is asking donors to accept a standard the apostles did not accept for themselves. Transparency is not identical with faithfulness, but secrecy is rarely a long-term friend of faithfulness.

Key sections of the Form 990 and what Christian donors should notice

Donors do not need to read every line to read wisely. A disciplined approach is better: focus on the sections most likely to surface governance strength, financial integrity, and clarity about mission. The following areas are where our team most often sees signals—both healthy and concerning—across nonprofit disclosures.

Part I and mission clarity

Part I summarizes the organization’s mission and the year’s activities. The question is not whether the language is inspiring, but whether it is concrete. Ministries with disciplined operations tend to describe outputs and activities with specificity. Ministries that rely primarily on emotional appeal often remain vague.

Clarity here also sets up coherence later. If a ministry claims its central work is international church planting, but its expense profile suggests something very different, the 990 may be the first place that inconsistency appears.

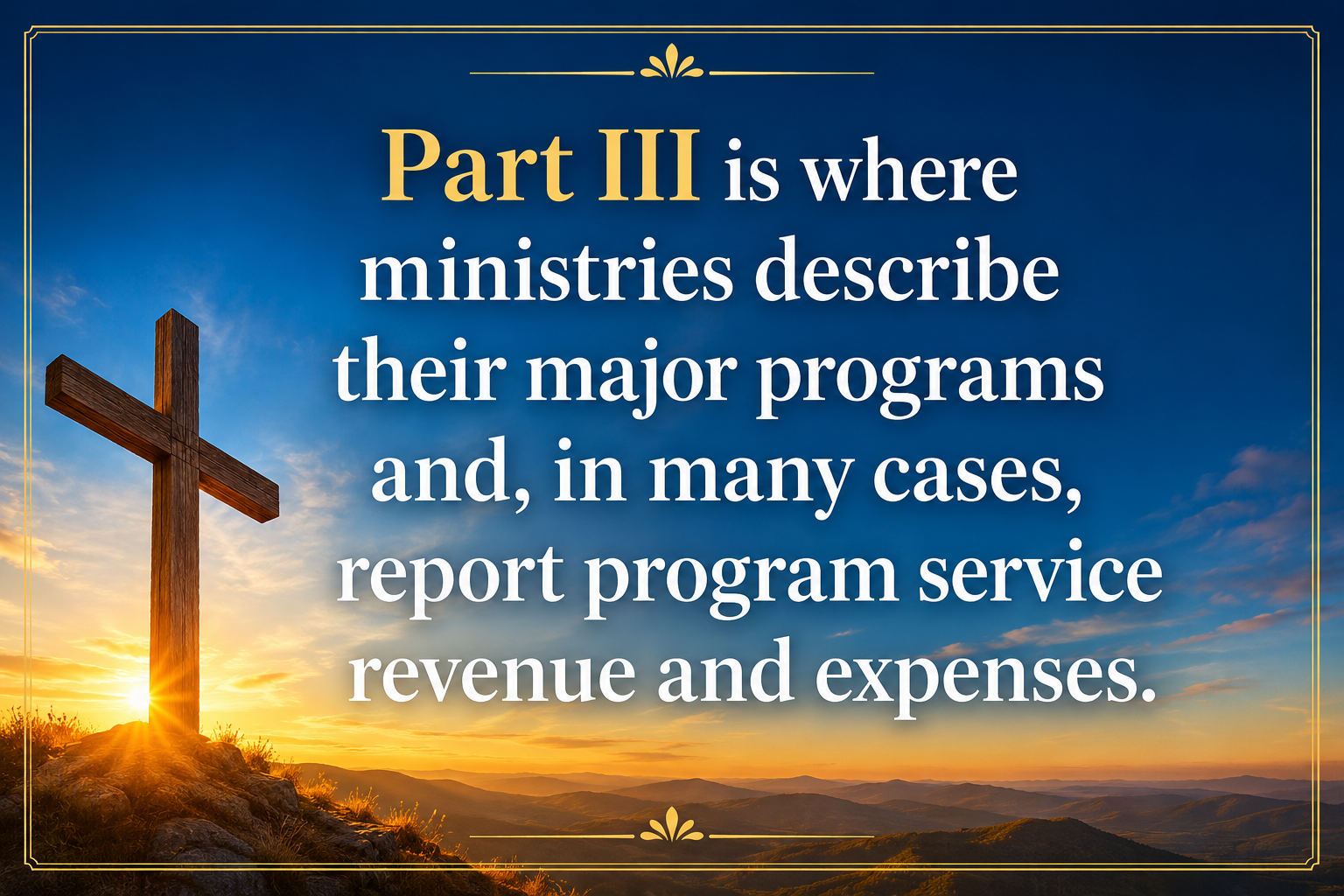

Part III and program service accomplishments

Part III is where ministries describe their major programs and, in many cases, report program service revenue and expenses. This section is often more revealing than donors expect. It can show whether a ministry treats outcomes as reportable realities or as marketing language.

Christians genuinely disagree about what should count as “results” in ministry. Some outcomes are quantitative (meals served, students enrolled, Bibles distributed). Others are spiritual and slower to measure (discipleship depth, church health, reconciliation). The goal is not to force sanctification into a spreadsheet. The goal is to see whether the ministry’s claims are accountable to any credible form of evaluation, and whether it avoids inflated, unverifiable assertions.

Part VI and governance disclosures

Part VI is a governance and management section that donors should treat as central. It includes questions about the board’s independence, whether the organization has conflict-of-interest and whistleblower policies, and whether the board reviews the 990 before filing.

These may sound procedural, but they map closely to moral hazards that regularly damage ministries: founder dominance, insider transactions, unchallenged compensation decisions, and a culture where staff cannot safely report concerns. A conflict-of-interest policy is not a guarantee of righteousness. But the absence of one is an unnecessary vulnerability, especially when large donations and strong personalities are involved.

Part VII and compensation

Part VII reports compensation for officers, key employees, and highest compensated employees. Compensation is one of the most emotionally charged aspects of nonprofit evaluation, and it is easy for donors to either ignore it or fixate on it.

Wise reading asks several questions at once: Is compensation concentrated in ways that suggest insider enrichment? Is it aligned with organizational size and complexity? Is it transparently reported and explained? Does the organization describe a process for setting compensation that uses comparability data and independent oversight?

Donors should resist two errors. The first is assuming that low compensation is always a virtue; underpaying can drive instability, weak hiring, and hidden side arrangements. The second is assuming that high compensation is always theft; some organizations operate at a scale where compensation is legitimately higher. The moral question is whether compensation is set through a disciplined process, publicly disclosed, and consistent with the ministry’s stated posture of stewardship.

Part IX and the expenses behind the story

Part IX breaks down functional expenses: program services, management and general, and fundraising. This is the section most often distorted by simplistic “overhead ratio” thinking.

The broader philanthropic sector has repeatedly cautioned donors against treating overhead as the primary indicator of effectiveness. Charity Navigator, Candid (GuideStar), and the BBB Wise Giving Alliance jointly argued that overhead ratios can mislead donors and pressure nonprofits into underinvesting in infrastructure and evaluation, a dynamic sometimes referred to as the “overhead myth.” Overhead Myth campaign.

That caution is warranted, and Christian donors should take it seriously. Still, overhead patterns can surface concerns when they are extreme or when they conflict with a ministry’s narrative. A fundraising-heavy operation that claims extraordinary field impact deserves careful scrutiny. A ministry with rapidly rising “management and general” expenses may simply be professionalizing, but it may also be masking disorganization. Ratios are prompts for questions, not verdicts.

Schedule A and public support

Schedule A helps the IRS determine whether a nonprofit qualifies as a public charity rather than a private foundation. For donors, it can provide a window into how dependent the organization is on a small number of major donors versus broad public support.

Donor concentration is not automatically wrong; many faithful ministries begin with a few significant givers. But high concentration can create fragility and, at times, unhealthy influence. A mature ministry is not one that never receives large gifts, but one that governs itself so that no single donor becomes functionally sovereign.

Donor guidance for reading a Form 990 with discernment

Form 990 review should feel less like detective work and more like pastoral prudence applied to financial realities. We are not seeking perfection; we are seeking credible signs of honesty, competence, and accountability. The following practices help Christian donors use the 990 without being ruled by it.

Start with coherence, not ratios

Begin by comparing three things: the stated mission (Part I), the program descriptions (Part III), and the expense profile (Part IX). Coherence across these sections is a basic sign of integrity. If the narrative is about frontline work but the expenses suggest something else, the appropriate response is not immediate condemnation, but questions that require real answers.

Coherence also applies over time. A single year can be anomalous due to a capital campaign, a program closure, or a crisis response. Patterns across multiple years are harder to dismiss and more likely to reveal operational character.

Take governance questions seriously

Many donors assume that governance is “internal” and therefore irrelevant. In practice, governance is one of the most reliable predictors of whether a ministry will endure without scandal. A board that is meaningfully independent, engaged, and willing to challenge leadership is not a luxury; it is a protection for the mission and for donors.

Where possible, donors should look for indicators of board independence in Part VI and for whether the organization reports a process for setting executive compensation. A ministry that cannot articulate how it avoids conflicts of interest is asking donors to rely on goodwill where Scripture calls for accountability.

Read fundraising and related-party disclosures without cynicism

Christian ministries often use direct mail, digital advertising, conferences, and media to raise support. Fundraising is not inherently manipulative. Yet some fundraising models can distort incentives, pushing ministries toward sensational stories, exaggerated metrics, or donor acquisition at the expense of pastoral honesty.

Donors should also pay close attention to related-party transactions disclosed in Schedule L, when applicable. Payments to insiders, loans, or business deals involving board members are not automatically corrupt, but they require clear disclosure and strong safeguards. The church’s witness is harmed when even the appearance of self-dealing is tolerated.

Use the 990 as a prompt for direct questions

A 990 cannot answer every legitimate concern. It can, however, equip donors to ask better questions. Examples of questions that serious ministries should be able to answer without defensiveness include:

- How does the board review financials and evaluate the executive leader?

- What safeguards prevent conflicts of interest in contracting and compensation?

- How are program claims validated, especially for spiritual outcomes that are harder to quantify?

- How does the ministry learn from failure without hiding it?

Donors sometimes fear that asking such questions is unspiritual. Yet Scripture consistently joins generosity with wisdom. “Let the wise hear and increase in learning” (Proverbs 1:5) is not suspended when the cause is urgent.

How Most Trusted uses Form 990 data within The Most Trusted Standard

At Most Trusted, we treat the Form 990 as an important source, but never the only source. The Most Trusted Standard is designed to evaluate ministries across four essential domains: theological faithfulness, financial integrity, governance and leadership, and transparency and effectiveness. The 990 contributes strongest evidence in the financial integrity and governance domains, and partial evidence in transparency and effectiveness.

In our verification work, the ministries that consistently meet The Most Trusted Standard tend to show several converging traits in their public filings and disclosures: independent governance with documented policies, compensation that is transparently set and explainable, financial statements that align with the ministry’s stated work, and a pattern of forthright communication rather than selective disclosure.

We also observe that some of the most damaging ministry failures were not primarily theological in origin. They were governance failures: unchecked authority, ambiguous accountability, and a culture in which questions were treated as disloyalty. A careful reading of governance disclosures cannot guarantee prevention, but it can reveal whether a ministry has built the kinds of guardrails that prudence demands.

Theologically, this is not a retreat into technocracy. It is an application of biblical wisdom to modern institutions. The New Testament’s concern for honorable handling of funds presumes structures, delegated responsibility, and transparent processes. The 990 is one instrument that helps donors see whether those processes plausibly exist.

FAQs for Form 990 for Christians: What It Tells You and How to Read It

Do all Christian ministries have a Form 990?

No. Churches are generally not required to file Form 990, and some church-affiliated entities may also be exempt depending on their classification. Many nonprofits do file, but smaller organizations may file a simplified version. The absence of a 990 should prompt clarification about legal status and transparency practices, not an automatic judgment.

Is a low overhead ratio a sign of a faithful ministry?

Not necessarily. Overhead ratios can be misleading and can incentivize underinvestment in governance, staff development, and evaluation. Leaders across the nonprofit sector have cautioned donors against using overhead as a primary measure of quality. Charity Navigator, Candid, and BBB Wise Giving Alliance on the overhead myth. What matters more is whether spending patterns are coherent with mission and whether the organization can explain its investments credibly.

What should concern a donor when reading executive compensation on the 990?

Concern is warranted when compensation is unusually concentrated, when related-party transactions appear without clear safeguards, or when the organization cannot describe an independent process for setting pay. Compensation should be evaluated in context of organizational size and complexity, but it should also be governed by transparent, accountable decision-making that aligns with the ministry’s stewardship claims.

Can the Form 990 tell whether a ministry is spiritually effective?

Only partially. The 990 can show whether a ministry reports program activities with clarity and whether it appears committed to evaluation, but it cannot measure spiritual fruit in any full sense. Donors should pair 990 review with theological due diligence, church accountability signals, and credible testimony from stakeholders closest to the work.

Stewardship that honors the gift and the Giver

A Form 990 will not tell the whole truth about a Christian ministry, but it can tell important truths that donors ignore at their peril. When Christians give without discernment, we risk funding dysfunction that eventually harms people made in God’s image and discredits the gospel we hope to commend. When Christians demand perfection before giving, we risk withholding support from imperfect servants doing real good.

The better path is informed generosity: giving with open hands and open eyes. The Form 990 is one instrument for that work. Used carefully—alongside prayer, theological clarity, and credible verification—it can help donors give with the confidence that their stewardship is both faithful before God and honorable before others.