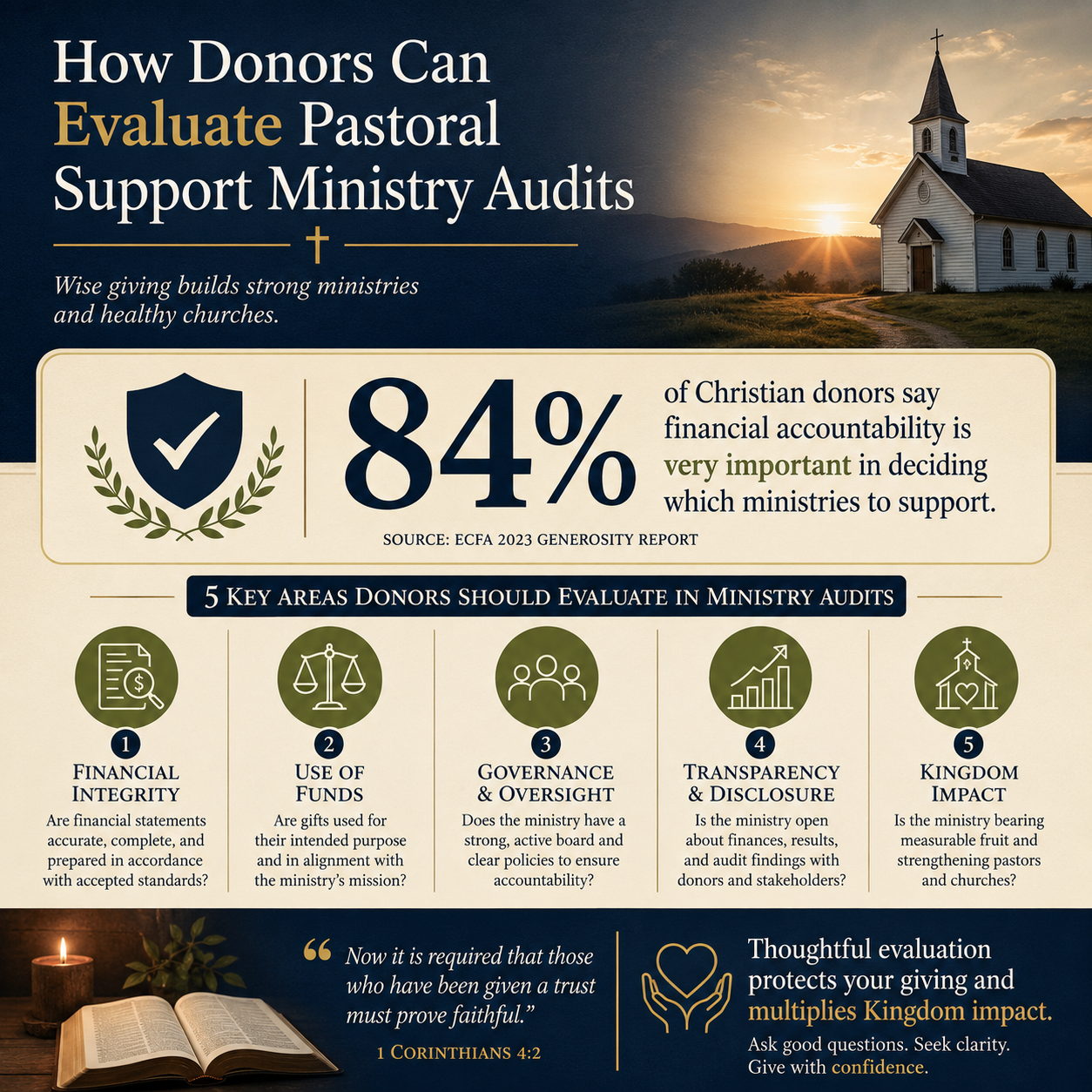

Evaluating pastoral support ministry audits is one of the clearest ways donors can honor both charity and truth. Pastors and their families live under spiritual and financial pressures that most congregations do not see, and faithful givers rightly want to ensure that a ministry’s care is real, accountable, and ordered toward long-term health rather than momentary relief.

The harder question is what an audit can and cannot tell you. An audit can verify whether financial statements are fairly presented and whether controls appear adequate. It cannot, by itself, prove that counseling was wise, that board oversight was spiritually mature, or that a ministry’s culture handles power safely. Mature donor discernment learns to read an audit as one strong instrument in a fuller evaluation.

Start with what an audit is and what it is not

Audit, review, compilation, and internal audit are not interchangeable

Donors frequently see the word “audit” used loosely. A financial statement audit performed by an independent CPA firm is the highest level of assurance among common engagements. A review provides limited assurance; a compilation provides no assurance. Some ministries also use internal audits or internal control reviews, which can be valuable but are not the same as an external audit because the independence and scope differ.

What this means in practice is that the first evaluation step is definitional: ask what engagement was performed, for what period, and by whom. If a ministry provides only internally prepared statements, donors should treat that as a reason to ask for stronger verification—not as proof of misconduct, but as a clear limit on what can be known from documents alone.

Pastoral care complicates conventional financial categories

Pastoral support ministries often blend benevolence, counseling, retreats, emergency assistance, training, and sometimes clinical referrals. That mixture introduces classification risks: restricted vs. unrestricted gifts, program vs. administrative categorization, and the proper accounting of designated support.

Christians genuinely disagree about the best models for funding pastoral care—direct subsidies, confidential emergency grants, member assistance programs, or long-term restoration plans. But donors can reasonably agree on this: whatever the model, funds must be handled with integrity, documented appropriately, and governed with safeguards that protect both the pastor receiving help and the donor who gave it.

Read the auditor’s report like a governance document

Look for the opinion, not the marketing summary

Ministries sometimes highlight “clean audit” language while omitting the auditor’s actual opinion and the accompanying financial statements. Donors should ask to see the full audited financials, including notes and the independent auditor’s report. The opinion is typically “unmodified” when the statements are fairly presented. Modified opinions, disclaimers, or adverse opinions matter because they indicate limits or disagreements about presentation.

If you are not accustomed to reading these reports, focus on whether the auditor is independent, whether the period covered is current, and whether the report references adherence to U.S. generally accepted auditing standards. When pastoral support work involves multiple funds or designated gift programs, the notes can be especially important, because they disclose restrictions, commitments, and related-party transactions.

Evaluate management letters and internal control findings with sober realism

Audits of nonprofits often include communications to those charged with governance about internal control deficiencies. Not every deficiency is catastrophic, and smaller ministries can have real capacity constraints. Yet repeated findings with no remediation plan should concern donors, because they suggest either lack of competence or lack of will.

Donors should also recognize that an audit is not designed to detect every fraud. The American Institute of Certified Public Accountants explains that audits provide reasonable, not absolute, assurance and that collusion can defeat controls AICPA. That limitation is one reason we treat audits as necessary but not sufficient when verifying ministries against The Most Trusted Standard.

Ask how the ministry safeguards the dignity and safety of pastors

Confidentiality must coexist with accountability

Pastoral support work often involves sensitive information: marital strain, pornography, burnout, depression, moral failure, or allegations of abuse. Confidentiality is a Christian duty in many contexts. Yet confidentiality can also become a shield against scrutiny if it is used to prevent any meaningful reporting.

A mature ministry can protect privacy while still providing donors with verifiable evidence: clear eligibility criteria, documented decision processes, aggregate reporting, and independent oversight. Donors can ask for de-identified outcome reporting and for written policies that define what information is protected, what must be reported to authorities, and what must be escalated to independent governance.

Mandatory reporting, clinical boundaries, and referral networks matter

Some pastoral support ministries provide coaching and spiritual care; others offer counseling by licensed clinicians or refer into clinical networks. Donors should ask what the ministry is actually providing, who provides it, and what the boundaries are. Where licensed counseling is involved, the ministry should be prepared to explain licensure, supervision, and ethical standards. Where it is not involved, the ministry should be prepared to explain how it avoids practicing therapy without appropriate qualifications.

The field has had to reckon with high-profile failures in church and parachurch contexts where inadequate governance and unclear boundaries harmed vulnerable people. Donors do not serve pastors well by funding ministries that treat professional standards as optional. Scripture’s warnings about shepherds and the vulnerable are not abstract. James cautions that teachers will be judged with greater strictness, a principle that should sober both boards and donors.

Trace dollars from donation to care with targeted questions

Restricted giving and designated funds require special discipline

Pastoral support often attracts designated gifts: “for counseling scholarships,” “for sabbaticals,” “for emergency housing,” or “for restoration.” Donors can legitimately ask whether the ministry uses restricted funds according to donor intent and whether it has a process to re-purpose funds when restrictions cannot be met. The notes to audited financial statements often disclose net assets with donor restrictions and the ministry’s policies for releasing restrictions.

For donors who want a more grounded sense of whether reported numbers reflect reality, a small number of precise questions can help. We recommend asking for documentation at the policy level rather than asking for private case files.

- What portion of program spending is direct aid to pastors versus services delivered by staff and contractors?

- What is the approval process for grants, including who can approve and what documentation is required?

- How does the ministry prevent conflicts of interest when supporting pastors within the same networks as leaders or board members?

- What is the policy for cash assistance, gift cards, or rent payments, and how is it tracked?

- How does the ministry verify eligibility without humiliating the recipient?

Overhead ratios are a poor shortcut, but controls are not

Many donors have been trained to treat low overhead as the primary signal of faithfulness. The sector has pushed back for good reasons. Charity Navigator, Candid, and the BBB Wise Giving Alliance argued that overhead ratios can mislead and can create perverse incentives to underinvest in systems that prevent harm Charity Navigator. Pastoral support work is especially vulnerable to this distortion because strong care requires trained staff, safeguards, and sometimes clinical partnerships.

But rejecting overhead shortcuts does not mean rejecting accountability. A ministry can have a respectable program ratio and still have weak segregation of duties, poor documentation, or inadequate board oversight. Donors should prioritize internal control strength, clarity of restricted-fund management, and evidence of competent financial leadership.

Use audits as one component in a fuller verification approach

Governance, theology, and effectiveness must be evaluated alongside financial integrity

An audit speaks primarily to financial statements. Donors are asking a broader moral question: is this ministry worthy of trust? For pastoral support, that question includes theological commitments, governance, leadership character, safeguarding practices, and whether care is effective and restorative rather than merely palliative.

Across our verification work at Most Trusted, ministries that meet The Most Trusted Standard tend to treat documentation as a form of love: clear policies, accountable boards, and transparent reporting that does not trade on sentiment. That posture aligns with the biblical conviction that “we aim at what is honorable not only in the Lord’s sight but also in the sight of man” (2 Corinthians 8:21).

Where to situate your next steps as a donor

Donors who are focusing specifically on pastoral support ministries may find it helpful to compare how different organizations think about pastoral restoration, confidentiality, and governance. Our broader coverage of Pastoral Support Ministries addresses patterns we observe across the field, including the pressures that make strong accountability both difficult and indispensable.

When your question is more specific—how money is categorized, how grants are administered, and how direct care is funded—our related work on How Pastoral Support Ministries Use Donations can help frame the operational realities behind financial statements. Donors should expect ministries to welcome these questions, not because donors are suspicious, but because Christian stewardship deserves daylight.

FAQs for How donors can evaluate pastoral support ministry audits

Should we require an audited financial statement before giving to a pastoral support ministry?

For larger ministries, audited financial statements are a reasonable expectation because scale increases complexity and risk. For smaller ministries, an audit may be financially burdensome, but donors should still expect meaningful accountability: an independent financial review, clear internal controls, board-level financial oversight, and transparent reporting. The right requirement should be proportionate to the funds raised and the complexity of the ministry’s programs.

What audit red flags matter most for pastoral support work?

Material weaknesses in internal controls, repeated unresolved findings, unclear treatment of restricted funds, significant related-party transactions without clear disclosure, and missing or outdated audited statements deserve careful attention. Donors should also treat vagueness as a warning sign: if the ministry will not explain how funds move from donation to care at a policy level, the audit alone will not provide the needed confidence.

Giving that strengthens the church requires verifiable trust

Pastoral support is not an optional kindness. The church depends on faithful shepherds, and faithful shepherds are finite people who can be wounded, tempted, exhausted, and sometimes disqualified. Donors serve the church best when generosity is paired with discernment that is both spiritually serious and operationally competent.

An audit is a valuable instrument for that discernment, but it must be read carefully and paired with questions about governance, safeguarding, and real-world practice. When donors insist on verifiable trust, they protect pastors from chaotic care, protect donors from misplaced confidence, and honor the God before whom every stewardship account will finally be rendered.