What tax receipts military outreach ministries should provide is not a peripheral administrative question. For Christian donors, receipts are one of the clearest ways a ministry demonstrates truthfulness in the small things, and Scripture is unambiguous that integrity in small things is a measure of integrity in larger ones (Luke 16:10). When receipts are inconsistent, vague, or delayed, donors are left to infer what should have been stated plainly.

Military outreach often carries special complexity: care for deployed service members, support for spouses and children, programs on or near installations, chaplain partnerships, and sometimes international activity. None of that diminishes the need for clear, IRS-compliant acknowledgments. It increases it, because complexity creates more opportunities for confusion, and confusion erodes trust.

What the IRS requires and what wise donors should still expect

Donor receipts live at the intersection of biblical stewardship and federal law. The IRS sets minimum standards for “contemporaneous written acknowledgment” for certain gifts; prudent ministries go further, because the aim is not merely compliance but clarity.

When a written acknowledgment is required

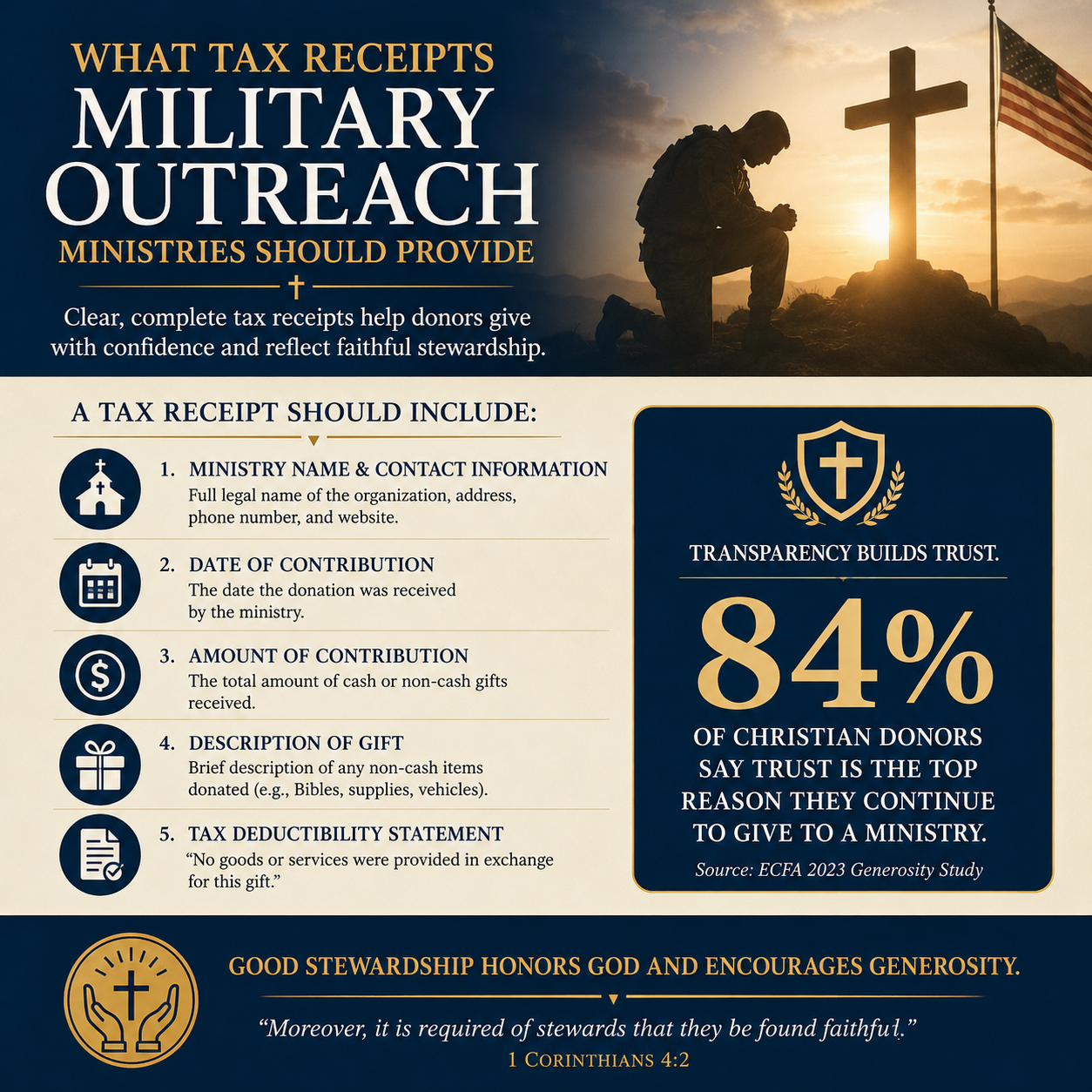

For any single contribution of $250 or more, the donor must have a contemporaneous written acknowledgment from the charity to claim a deduction. The IRS is explicit that a bank record alone is not sufficient at that threshold. Ministries that serve military communities should treat this as non-negotiable donor care, especially for year-end giving when documentation is time-sensitive. The controlling guidance is summarized by the IRS in its Charitable Contributions rules and publication materials (IRS).

What must be included in the acknowledgment

The required elements are straightforward: the organization’s name, the date and amount of cash contributions, or a description (not value) of noncash property; and a statement about whether goods or services were provided in exchange for the gift, with a good-faith estimate of value if they were. If none were provided, the receipt should clearly state that no goods or services were provided in exchange for the contribution. The IRS lays this out directly in its rules for acknowledgments (IRS).

What this means in practice is that “thank you” emails that omit the goods-and-services language, or year-end summaries that list totals but do not address quid pro quo, can leave a donor exposed. A ministry may be acting in good faith and still fail the standard of clarity.

Cash gifts, recurring giving, and the year-end statement

Many military outreach ministries now depend on recurring donors—monthly care packages, sponsorship for counseling sessions, underwriting for base-adjacent events. The administrative pattern for receipts should fit that reality: immediate acknowledgments for each gift where possible, and a clean annual summary that does not introduce ambiguity.

Receipts for one-time gifts

For a one-time cash gift, donors should expect a prompt email or letter that includes the required elements. “Prompt” is not a legal category, but ministries that operate with seriousness tend to acknowledge within days, not weeks. Delays create downstream problems: donors lose records, employers request documentation for matching gifts, and the ministry’s finance team ends up reissuing receipts under pressure.

Annual summaries for recurring donors

Annual giving statements can serve donors well, particularly when they list each gift with date and amount and include the goods-and-services statement. The risk is that a year-end statement becomes a replacement for proper acknowledgments without meeting the IRS standards. Wise donors should look for specificity rather than a single aggregated number if they want an easier audit trail.

Across our verification work at Most Trusted, the ministries that meet The Most Trusted Standard tend to treat donor documentation as part of their transparency discipline, not merely as a finance function. That culture shows up in clean receipts, consistent naming, and year-over-year continuity in how acknowledgments are issued.

Noncash gifts and the limits of what a ministry should claim

Military outreach invites many noncash gifts: donated airline miles, vehicles, equipment for events, books and Bibles, gift cards, or donated professional services. These gifts can be meaningful, but they are also where receipts commonly become misleading.

What a ministry should say and not say about value

For noncash property, the ministry should describe the item(s) donated without assigning a dollar value. That boundary protects both the donor and the ministry. Donors may be eager for the ministry to “put a number on it,” but the IRS places valuation responsibility on the donor, not the charity, in most cases. A receipt that assigns values casually can create tax problems and signals a lack of rigor. The IRS guidance addresses this division of responsibility in its charitable substantiation rules (IRS).

Special caution with services, gift cards, and restricted items

Donated services are generally not deductible as charitable contributions, even when the service is skilled and costly. A ministry should still acknowledge the service as gratitude and recordkeeping, but it should not present that acknowledgment as a tax receipt for a deductible contribution. Gift cards are often treated like cash equivalents; practices vary, and donors should proceed carefully and seek tax counsel when in doubt.

When gifts relate to military contexts—equipment, travel, or items intended for deployed settings—another layer appears: compliance with base policies, export restrictions, and safety requirements. A ministry that is careful here will be careful in its documentation as well, and donors should expect that steadiness.

Quid pro quo and events where donors receive something back

Military outreach ministries often host banquets, golf tournaments, conferences for spouses, fundraising dinners, or ticketed events featuring speakers. These can strengthen community and raise essential funds. They also create “quid pro quo” situations where donors receive goods or services in exchange for payment, which requires specific disclosure.

When the ministry must disclose value

If a donor makes a payment of more than $75 and receives goods or services in return, the organization must provide a written disclosure statement describing the goods or services and providing a good-faith estimate of their value. This is separate from the $250 acknowledgment rule and is commonly overlooked. The IRS describes these disclosure requirements in its guidance for charities (IRS).

How this often fails in practice

The most common failure is a receipt that thanks the donor for the full ticket price without stating the fair market value of the dinner or benefits received. Another failure is a “sponsorship” package that includes advertising, reserved seating, or other tangible benefits, with no valuation described. This is not merely technical. It communicates that the ministry is comfortable with ambiguity where the donor needs clarity.

Donors who want to understand the broader ministry landscape—how military outreach is structured, where programming is most effective, and what strong accountability looks like across the field—often begin with Military Outreach Ministries. Documentation standards should be assessed alongside mission clarity and spiritual accountability, not apart from them.

What donors should request and what strong ministries provide by default

Some donors hesitate to ask for documentation because they do not want to burden ministries serving service members. But transparency is not a distraction from mercy. It is part of faithful administration, and in a sector that relies on trust, it is part of protecting the ministry’s witness.

A short checklist donors can use

- Receipt includes the legal organization name and the date and amount of the gift.

- Receipt states whether any goods or services were provided, and if so, estimates their value.

- Noncash gifts are described without assigning a dollar value.

- Year-end statement itemizes gifts and repeats the goods-and-services language.

- Event and sponsorship receipts separate the deductible portion from the value received.

How this fits with wise Christian giving

Christians genuinely disagree about how much administrative rigor is “enough,” particularly for smaller ministries with limited staff. The stronger question is whether the ministry is candid about its limits and whether it is building toward faithful practices. A small ministry can still issue correct receipts; a large ministry can still evade clarity. Size does not determine integrity.

At Most Trusted, we evaluate ministries against The Most Trusted Standard, with attention to financial integrity, governance discipline, and transparency that respects donors as stewards. Donors who want to think carefully about giving practices in this space often find it helpful to read within How to Give Wisely to Military Outreach Ministries, because receipt quality is rarely an isolated issue; it tends to correlate with other verifiable patterns of accountability.

FAQs for What tax receipts military outreach ministries should provide

Is an email receipt acceptable for a donation over 250 dollars?

Yes. The IRS allows contemporaneous written acknowledgment in electronic form, as long as it includes the required elements: the organization’s name, the amount and date (for cash gifts), and the statement about goods or services provided in exchange for the contribution. The key is completeness, not paper versus email (IRS).

What should a military outreach ministry write if no goods or services were provided?

The receipt should explicitly say that no goods or services were provided in exchange for the contribution. That sentence is not filler; it is an IRS-required element for substantiation and it protects the donor’s ability to claim a deduction for qualifying gifts (IRS).

Receipts are a test of truthfulness

Military outreach ministries operate close to sacrifice, grief, courage, and moral injury. Donors give because they want the Church to serve those who bear the sword on the nation’s behalf, and to care for the families who endure the long separations. The administrative work of issuing accurate receipts can feel small beside those realities, but Scripture does not permit a divide between spiritual seriousness and honest accounting.

When a ministry provides clear, timely, IRS-compliant receipts—especially around events, noncash gifts, and recurring giving—it offers donors more than documentation. It offers a measurable sign that the ministry intends to walk in the light, where confidence is not demanded but earned.