“How Christian ministries actually spend money” is a stewardship question before it is a branding question. Donors are not merely buying outcomes; we are entrusting resources that ultimately belong to the Lord to institutions that will answer for how they handled them.

Scripture treats financial administration as a moral and spiritual matter. Paul took pains to arrange a collection for Jerusalem “so that no one should blame us about this generous gift that is being administered by us,” aiming to do “what is honorable not only in the Lord’s sight but also in the sight of man” (2 Corinthians 8:20–21). The impulse behind that passage is not cynicism. It is Christian realism about temptation, reputational risk, and the need for public integrity.

What this means in practice is that a ministry budget should tell the truth. It should tell the truth about mission, leadership, governance, risk management, the real cost of serving people well, and whether the organization is built to endure. The harder question is that the same budget line can represent faithfulness in one organization and dysfunction in another. Wise donors need categories, not slogans.

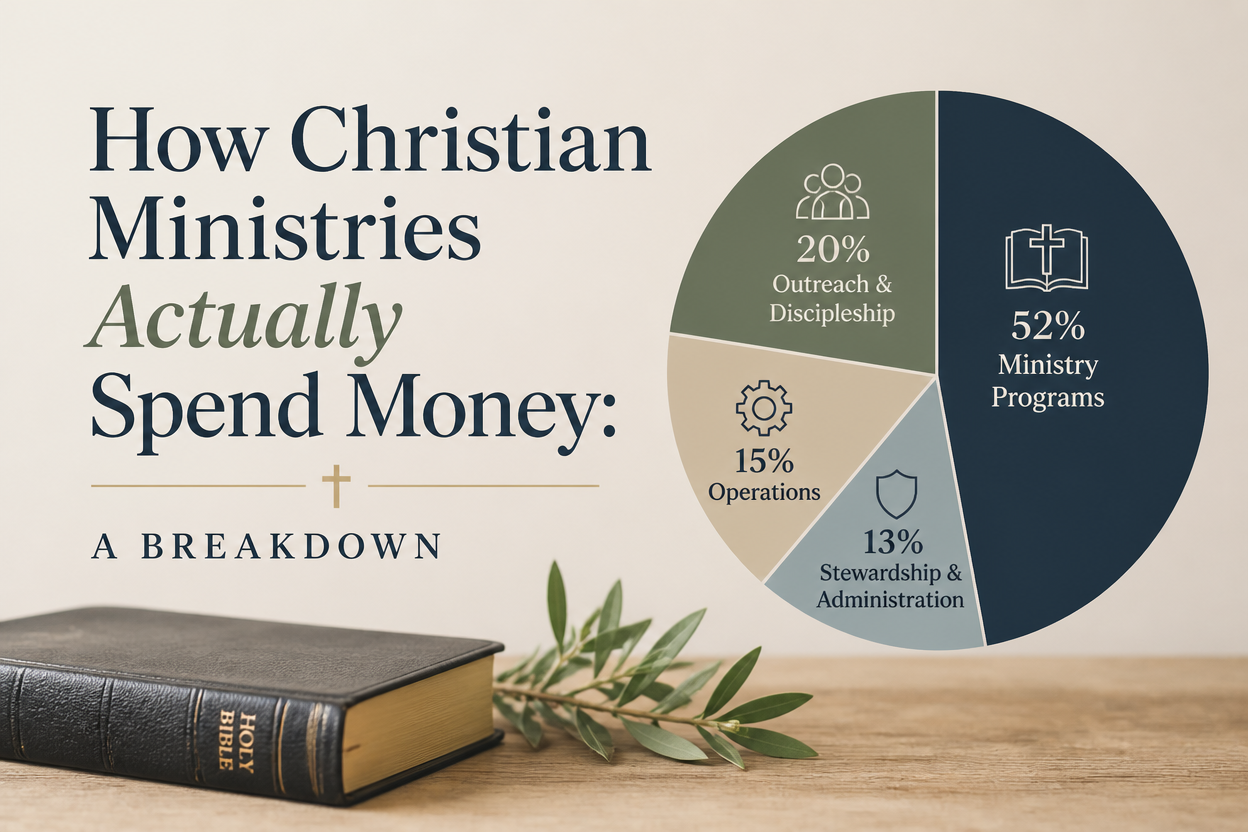

The main buckets ministries spend money on

Most Christian ministries’ spending can be understood in four broad buckets: program services, fundraising, administration, and reserves or capital investment. The labels differ across accounting systems, but the underlying realities are consistent.

In the United States, organizations that file an IRS Form 990 report “functional expenses” under three categories: program services, management and general, and fundraising. That framework is not perfect, but it is a useful starting point because it forces an organization to name what portion of spending is directly tied to mission delivery versus the infrastructure that supports it.

Program services

Program services include the direct costs of doing the work: missionaries’ support, pastoral training cohorts, prison chaplaincy programming, Bible translation field operations, pregnancy center medical services, or disaster response logistics. It often includes a portion of staff compensation, travel, facilities, and technology that directly enables those services.

Donors often assume “program” means “everything we emotionally associate with ministry” and “non-program” means waste. The reality is more exacting. A counseling ministry’s “program” may legitimately include licensed supervision, clinical documentation systems, and safeguarding training. A global relief organization’s “program” may include security protocols and third-party monitoring in high-risk environments. These are not distractions from mission; they are part of what it costs to serve without harming.

Fundraising

Fundraising includes the cost of acquiring and retaining donors: direct mail, email platforms, donor management systems, events, and development staff. The ethical question is not whether fundraising costs exist; it is whether they are proportionate, transparent, and consistent with the ministry’s theological posture toward manipulation and truth.

Fundraising also has a time horizon. Some fundraising spending is an investment that stabilizes future ministry capacity. Some is a treadmill that produces attention without durable donor trust. Mature donors evaluate fundraising the way Scripture evaluates speech: whether it is truthful, whether it respects the conscience of the listener, and whether it is ordered toward love rather than exploitation.

Administration and governance

Administration includes finance, HR, legal, compliance, leadership, board support, and general operations. Donors sometimes treat administration as an unfortunate necessity. Scripture treats competent oversight as part of faithfulness. The early church created structures to ensure equitable distribution so that the apostles could focus on prayer and the ministry of the word (Acts 6:1–4). That is not a modern corporate idea; it is an apostolic one.

Administration becomes suspect when it is bloated, opaque, or structured to protect leadership rather than to protect mission and people. It is also suspect when it is artificially minimized by pushing real costs into “program” categories to satisfy donor expectations. Both problems are common.

Reserves and capital

Many ministries also spend on reserves, debt service, capital projects, and long-term assets. Some donors view reserves as unspiritual. Yet Joseph stored grain in years of plenty to preserve life in years of famine (Genesis 41). Not every ministry should build large reserves, but the biblical category for prudent preparation is legitimate. The question is proportion and purpose: whether reserves exist to stabilize ministry in volatility, or to insulate leaders from accountability.

Why “overhead” is the wrong question and what to ask instead

Christian donors have been trained to ask one question: “What percentage goes to overhead?” That question is understandable, and it often comes from righteous frustration with scandals. But it is also vulnerable to manipulation, and it can punish exactly the kinds of ministries that invest in accountability, safety, and measurement.

The broader nonprofit field has challenged the obsession with overhead for similar reasons. Leaders from Charity Navigator, GuideStar, and the BBB Wise Giving Alliance publicly argued that “overhead is a poor measure of a charity’s performance” and urged donors to evaluate transparency, governance, and results rather than a single ratio Overhead Myth letter.

The difference between cost and waste

Cost is what it takes to do the work well. Waste is spending that does not meaningfully advance mission, integrity, or care for people. A ministry can have low administrative ratios and still be wasteful if it underinvests in internal controls, burns out staff, or substitutes emotional storytelling for honest reporting. A ministry can have higher administrative ratios and be exemplary if it is building systems that prevent harm and increase long-term effectiveness.

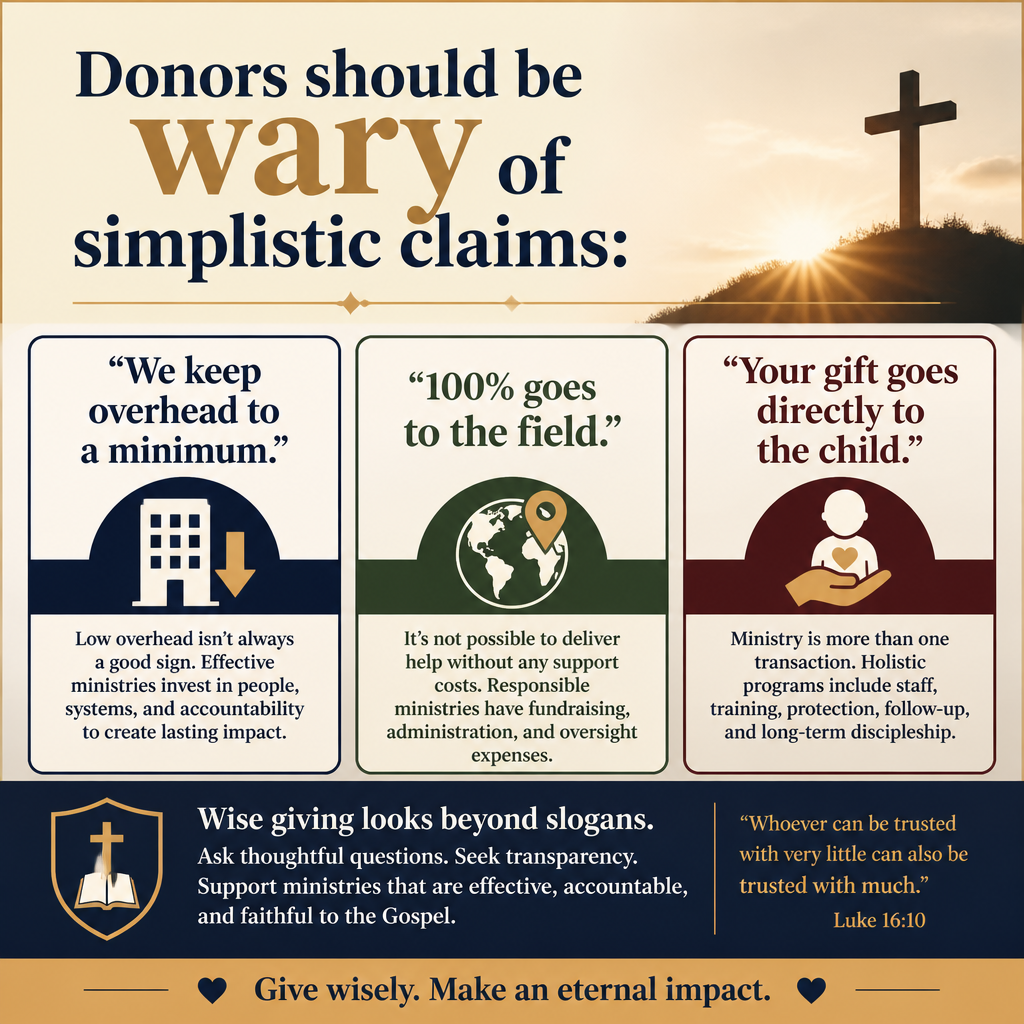

Donors should be wary of simplistic claims: “We keep overhead to a minimum,” “100% goes to the field,” or “Your gift goes directly to the child.” These phrases can be true in narrow accounting senses, yet misleading about the full cost structure. The more a ministry markets itself primarily on low overhead, the more it is tempted to treat financial presentation as donor management rather than truth-telling.

How overhead fixation distorts ministry behavior

When donors punish legitimate administrative spending, ministries often respond predictably: they underpay finance staff, delay audits, defer technology upgrades, and avoid investing in safeguarding. Over time, these “savings” become moral liabilities. The church has learned, painfully, that underinvestment in oversight can create environments where abuse, fraud, and deception flourish.

This is not an argument for indulgence. It is an argument for the right kind of scrutiny. Mature scrutiny asks whether overhead is buying integrity and resilience or merely supporting comfort and control.

What budgets reveal about theology and formation

A ministry’s spending is never merely technical. Budgets reveal what leaders believe about people, power, temptation, and truth. They also reveal whether an organization’s public posture matches its internal formation.

Compensation and the moral ecology of leadership

Christians genuinely disagree about what constitutes appropriate compensation for nonprofit leaders. Some donors insist on minimal pay as a sign of sacrifice; others recognize that complex organizations require seasoned executives, and that underpaying leadership can incentivize hidden benefits or lead to instability. Scripture condemns both greed and the kind of false piety that uses religious language to mask exploitation.

The donor’s question should be concrete: Is compensation governed by a real board, benchmarked responsibly, and disclosed with clarity? Is there evidence that pay practices support long-term leadership health rather than cultivating celebrity? Are related-party transactions prohibited or tightly controlled? These are governance questions more than moral postures, but they are inseparable from moral outcomes.

Fundraising practices and the ethics of persuasion

Christian fundraising inevitably involves persuasion. The question is whether it involves pressure. Ministries that traffic in exaggerated claims, selective stories, or crisis language as a steady-state strategy often produce distorted spending as well. They must continually spend to maintain urgency. They also often avoid rigorous evaluation because honest measurement can complicate a simple appeal.

Paul’s model again matters: “We have renounced disgraceful, underhanded ways. We refuse to practice cunning or to tamper with God’s word” (2 Corinthians 4:2). A ministry’s fundraising line items are not neutral; they are part of a theology of communication.

Measuring effectiveness without becoming utilitarian

Some Christian donors fear that effectiveness language smuggles in secular utilitarianism. That concern deserves respect. The church’s call includes faithfulness in places where outcomes are slow, hidden, or impossible to quantify. Yet the opposite error is also real: using spiritual language to avoid learning whether a program is helping, doing nothing, or causing harm.

Many of the most mature ministries invest in monitoring and evaluation not to imitate corporate dashboards, but to love their neighbors with competence. They track what can be tracked, they tell the truth about what cannot, and they remain accountable to Scripture and to the communities they serve.

How to read a ministry’s financials with donor seriousness

Donors do not need to become auditors to practice wise stewardship. But donors do need a disciplined way of reading financial signals. The aim is not suspicion; it is discernment.

Start with audited financial statements when available

An independent audit is not a guarantee of integrity, but it is a meaningful commitment to external scrutiny. If a ministry is large enough to justify an audit, donors should prefer audited statements over unaudited internal reports. For ministries that file a Form 990, donors can also review the organization’s public filings through the IRS. The IRS provides access to nonprofit filings and guidance for donors IRS Tax Exempt Organization Search.

When no audit exists, the donor’s question becomes: what compensating controls are in place? Are there independent board members with financial competence? Are there internal financial reviews? Are there clear conflict-of-interest policies that are actually enforced?

Read functional expenses, but do not stop there

Program, fundraising, and administration ratios can surface questions. They cannot answer them. A program ratio that is unusually high can indicate healthy focus, but it can also indicate underinvestment in controls or aggressive cost allocation. A fundraising ratio that is unusually low can indicate efficiency, but it can also mean the ministry is living off a small number of major donors and could be fragile.

Pay attention to year-over-year patterns. Are fundraising expenses rising faster than program outcomes? Are administrative costs climbing because the ministry is professionalizing, or because bureaucracy is expanding? Budget trends often tell a clearer story than a single year snapshot.

Watch for concentration risk and dependence

Some ministries depend heavily on one donor, one church network, or one signature event. That dependence can shape spending in subtle ways, including pressure to tell only good news. A diversified revenue base is not a sign of unbelief; it is often a sign of resilience and of accountability to a broad community of supporters.

Donors should also ask about government funding when relevant. There are faithful Christian organizations that accept government grants with clear boundaries, and there are others for whom such funding would compromise mission or messaging. The issue is clarity, not ideology.

Scrutinize restricted giving and designated projects

Restricted gifts can be a gift to a ministry, but they can also distort priorities. When donors restrict heavily to attractive projects, ministries may struggle to fund unglamorous but essential work: child protection policies, staff training, compliance, or the slow work of local partnership. Wise donors sometimes give unrestricted support precisely to strengthen integrity.

Donors should ask whether the ministry is honoring restrictions faithfully and whether it has the capacity to track restricted funds without confusion. Weak systems here can create both ethical and legal problems.

What Most Trusted evaluates and why it matters for spending

Most Trusted exists because donors need more than ratios. Across our verification work, we see that the most common failures are not always obvious from a pie chart. They are governance weaknesses, theological ambiguity, conflicts of interest, opaque reporting, and the absence of credible evidence that programs are doing what leaders claim.

The Most Trusted Standard assesses ministries across four domains: Faith Foundation, Financial Integrity, Governance and Leadership, and Transparency and Effectiveness. That framework is designed to answer the kinds of questions that financial statements alone cannot settle: whether a ministry’s theology is clear and operative, whether its board is independent enough to govern, whether financial controls are appropriate to risk, and whether the organization tells the truth about outcomes and limitations.

In practice, spending patterns correlate strongly with these deeper realities. Ministries that meet The Most Trusted Standard tend to spend in ways that reflect mature governance: clean separation of duties, transparent compensation oversight, sober fundraising practices, and prudent reserves. Ministries that struggle typically show predictable symptoms: heavy dependence on a charismatic leader, unusually opaque related organizations, inflated program claims with little documentation, and internal control gaps that donors only learn about after a crisis.

Donors should not outsource conscience to any framework, including ours. But donors should insist on verifiable evidence. Christian generosity is not meant to be naive. Jesus instructed his disciples to be “wise as serpents and innocent as doves” (Matthew 10:16). That wisdom includes asking for documentation, not just inspiration.

FAQs for How Christian Ministries Actually Spend Money: A Breakdown

What is a reasonable percentage for a ministry to spend on administration?

There is no universally “reasonable” percentage that applies across ministry types. A missionary-sending organization, a media ministry, and a residential recovery program have fundamentally different cost structures. Donors should ask whether administrative spending is buying real oversight, safeguarding, and financial control, and whether the organization can explain its allocations without defensiveness or marketing spin.

Is it a red flag if a ministry spends significant money on fundraising?

It can be, but not automatically. Some fundraising spending is a disciplined investment in donor stability and long-term mission capacity. It becomes concerning when appeals rely on manipulation, when fundraising costs rise without corresponding clarity about results, or when the organization seems to exist primarily to fundraise rather than to serve.

Should Christian donors prefer ministries that claim very low overhead?

Not as a rule. The nonprofit sector has repeatedly warned that overhead ratios can mislead and can incentivize unhealthy underinvestment in accountability systems Overhead Myth letter. Donors should prefer ministries that can document governance, controls, and results with clarity, even when that requires real administrative spending.

What documents should donors ask for if they want to understand how money is spent?

When available, request audited financial statements, the most recent Form 990 for U.S. nonprofits, an annual report with outcome reporting, and a clear explanation of how restricted gifts are tracked and honored. Donors can also verify filings through the IRS database IRS Tax Exempt Organization Search. The goal is not to create burdensome suspicion, but to practice the kind of honorable administration Paul commended.

Stewardship that insists on truth

Christian donors ask how ministries spend money because we know money has spiritual weight. The question is not whether a budget looks tidy, but whether it is truthful: truthful about the cost of doing good work, truthful about risk and governance, and truthful about outcomes. Donors who insist on that kind of truth do not weaken ministry. We strengthen it, for the sake of the people served, the credibility of the church, and the honor of Christ.