Giving appreciated stock vs. cash is not merely a tax question. For Christian donors, it is a stewardship question: how to direct resources entrusted by God in a way that strengthens faithful ministry, avoids avoidable loss, and sustains long-term fruit. Scripture consistently treats material decisions as spiritual decisions, and it does so with an unembarrassed clarity about accountability and wisdom.

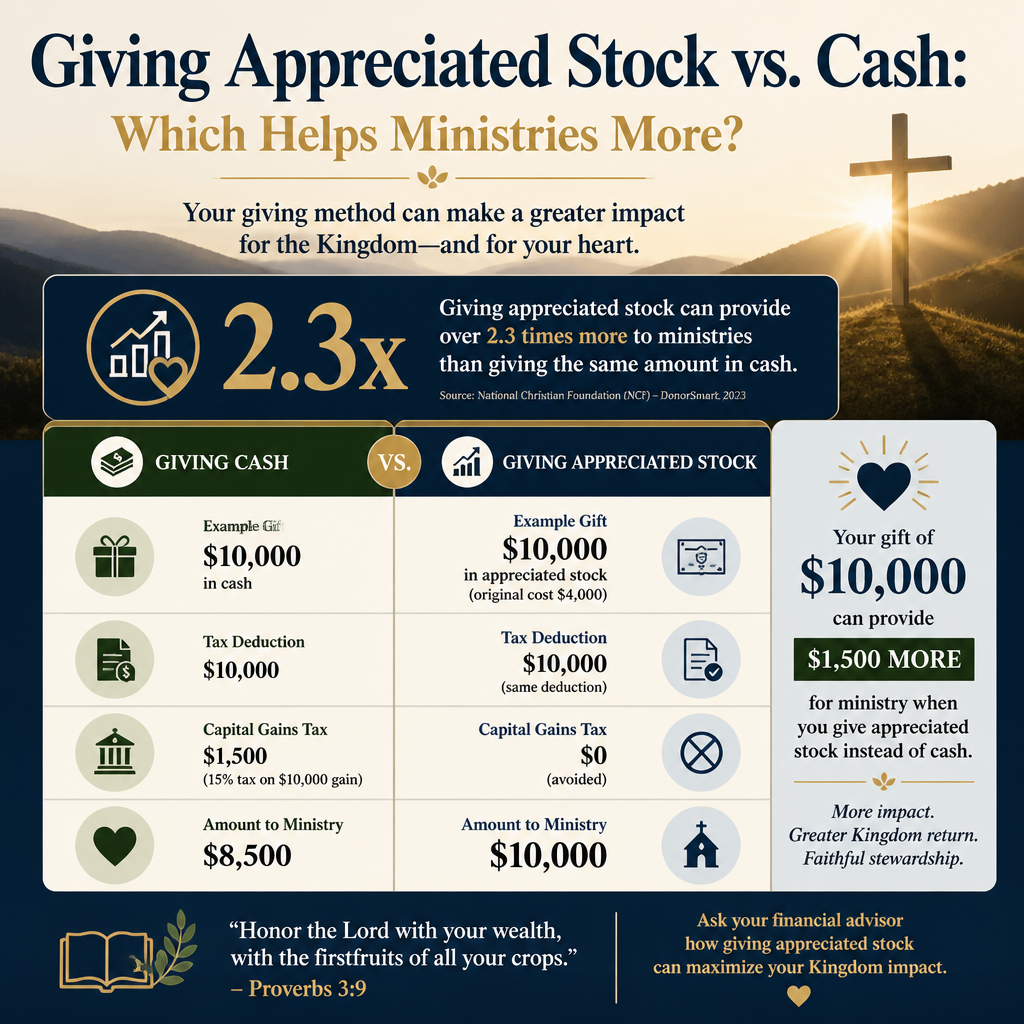

In most cases, giving appreciated stock helps ministries more than giving the same value in cash, because it can reduce the “friction” of taxes and preserve more of the gift for mission. But that general rule has meaningful exceptions. Some ministries cannot easily receive securities. Some gifts create cash-flow pressure if the ministry sells the shares poorly. And some donors use stock giving as a way to give more without the harder work of reordering everyday spending habits. Christian giving requires both generosity and prudence.

What follows is a practical comparison that takes ministries seriously, takes donors seriously, and takes the moral weight of stewardship seriously. The goal is not to win an argument for a particular giving vehicle. The goal is to help donors give with fewer hidden losses and greater confidence that a ministry is equipped to receive and use the gift well.

Why appreciated stock often benefits both donor and ministry

The basic mechanics are straightforward. When a donor gives appreciated publicly traded stock that has been held long enough to qualify for long-term capital gains treatment, the donor may be able to claim a charitable deduction for the fair market value and avoid paying capital gains tax that would have been owed if the stock were sold first. That is not a loophole; it is a long-standing feature of U.S. charitable tax policy.

For ministries, the benefit is not theoretical. If the donor sells stock, pays capital gains, and then gives cash, the ministry receives a smaller net gift than it might have received if the shares were given directly. When appreciated stock is donated and then liquidated by the ministry (or by a broker acting on its behalf), more of the economic value can remain available for ministry rather than being lost to taxation.

Stewardship is not synonymous with tax minimization

Christian donors sometimes hesitate to talk about tax efficiency because they fear it sounds self-interested. That concern is not frivolous; Jesus’ warnings about money are severe, and the human heart is skilled at justifying itself. Yet the biblical tradition also insists that wisdom and prudence are virtues, not vices. The parable of the talents commends faithful management of entrusted resources (Matthew 25:14–30). Avoiding unnecessary leakage is one way of treating a gift as something holy—set apart for God’s purposes.

Tax benefits do not make a gift righteous, but neither do they make it suspect. What matters is whether the gift is offered in faith, with integrity, and with honest attention to outcomes.

The IRS framework donors are actually using

From a compliance perspective, stock giving is not improvised. The IRS outlines how charitable contributions work, including the different treatment of cash and noncash property and the substantiation requirements that follow. Donors should read the primary source rather than relying on hearsay from fundraising materials. IRS: Charitable contributions.

For appreciated property, the IRS also provides specific guidance on when fair market value deductions apply and when special rules limit the deduction. Those details matter when gifts are significant and when donors are concentrated in a single holding. IRS Publication 526: Charitable Contributions.

When cash is the better gift

Cash is not the inferior option. It is the most flexible and, for many ministries, the most administratively straightforward. In particular situations, cash is the more faithful and more useful gift because it reduces complexity and timing risk for the ministry.

When the ministry’s need is immediate and operational

Ministries run on payroll, rent, utilities, insurance, and vendor contracts. If a ministry’s need is urgent and near-term, the lag time for receiving and liquidating stock may create real stress, even if the total value is higher. A donor who wants to keep a food pantry open next week is not serving the mission by choosing a giving vehicle that introduces delay.

This is not a moral indictment of stock gifts; it is a cash-flow reality. Many Christian nonprofits are not capitalized like endowments. A gift that arrives with operational immediacy can be a form of mercy.

When a ministry cannot accept securities without undue burden

Some ministries lack brokerage accounts, policies, or internal controls for receiving and promptly selling securities. Others rely on third-party processing that is expensive or slow. In those cases, the “more efficient” gift on paper can be less efficient in practice.

There is also governance risk. A ministry that does not have clear written policies for handling noncash gifts can drift into ad hoc decisions and internal confusion. Those weaknesses rarely remain isolated; they often correlate with broader patterns of weak financial oversight.

When the donor’s stock position is entangled with restrictions

Restricted stock, closely held shares, and complex securities can create valuation challenges and legal exposure. Even with publicly traded stock, donors sometimes want to give shares that have sentimental attachment or that are associated with employment relationships that generate confidentiality concerns. In those cases, cash may protect both donor privacy and ministry simplicity.

Complex gifts can be excellent gifts, but only when both sides are equipped to handle the complexity with integrity.

What ministries experience when donors give stock

Many donors assume that a stock gift lands in a ministry’s account the way a check does. In reality, receiving appreciated stock typically involves coordination among the donor, the donor’s broker, the receiving ministry, and the ministry’s brokerage custodian. The ministry then needs a policy-driven process for acknowledging the gift, liquidating it, and documenting the outcome.

When that process is mature, stock gifts can be transformative. When it is immature, stock gifts can become a distraction, or worse, a governance vulnerability.

Speed and execution matter for ministry outcomes

One often-overlooked question is how quickly a ministry sells donated stock. Many nonprofits follow a “sell immediately” policy to reduce market risk. That is generally prudent because the ministry is not called to speculate with donated assets. A gift intended for gospel work can be unintentionally converted into a bet on market timing if the ministry holds the shares.

Donors can respectfully ask: Does the ministry have a written policy to liquidate promptly? Who is authorized to execute sales? How is that decision documented? A ministry that answers clearly is usually a ministry that treats stewardship as a matter of obedience rather than convenience.

A stock gift can expose hidden weaknesses

Across our verification work at Most Trusted, we observe that strong ministries tend to have boring, consistent processes: documented gift acceptance policies, separation of duties, clear accounting practices, and transparent donor communication. Those habits become visible when a donor offers something other than cash. A ministry that handles a stock gift with competence often has competence in other areas that donors care about.

Conversely, when a ministry seems unsure how to receive a stock gift, it may simply be small and under-resourced. But it may also be revealing a lack of financial controls or governance clarity. Mature donors do not need to assume the worst; they should assume the need to verify.

Donor intent and restriction require careful handling

Some stock gifts are unrestricted, and that freedom is often what ministries need most. Other gifts are designated to a project, campus, or program. Restrictions can be appropriate, but they also raise the bar for accounting and reporting. A ministry should be able to show that designated gifts are tracked and used as promised, and that any changes are communicated and approved.

Christian donors are right to care about alignment between intent and execution. Scripture is unsparing about vows, integrity, and truthful dealing (Ecclesiastes 5:4–5). Donor restrictions are not vows, but they do create moral and relational obligations that should not be treated casually.

Donor guidance for choosing stock or cash with integrity

Most donors do not need a complex giving plan to make a faithful decision. They need a set of disciplined questions that clarify what will genuinely help a ministry and what will merely feel sophisticated. The aim is not to give in a way that flatters the donor’s self-understanding, but to give in a way that strengthens the ministry’s work.

Begin with the ministry’s real needs and timeline

If a ministry has acute near-term needs, cash may be the truest expression of care. If the ministry is building long-term capacity, expanding programs, or strengthening reserves, appreciated stock may allow a donor to give more effectively. Either way, a donor should ask the ministry a simple question: “If this gift arrives as stock, how quickly will you be able to use it for mission?”

A mature ministry will answer concretely: the brokerage details, the expected timeline, and the internal policy that guides liquidation. Vagueness is not a disqualifier, but it is a signal to slow down and verify.

Verify gift readiness and financial controls

For significant gifts, it is reasonable to ask for the ministry’s gift acceptance policy, including how it handles noncash gifts and who approves exceptions. A ministry that receives gifts without written policies is not necessarily unfaithful, but it is operating with avoidable risk.

This is one reason verification matters. At Most Trusted, our evaluations against The Most Trusted Standard examine ministries across faith commitments, financial integrity, governance practices, and transparency. Donors are not merely choosing where to give; they are choosing whom to trust with funds intended for the Lord’s work. Verification does not replace discernment, but it reduces guesswork.

Consider donor-advised funds and other intermediaries with caution

Many donors use donor-advised funds to contribute appreciated stock and then recommend grants to ministries over time. That can simplify administration and allow a donor to give thoughtfully. It can also distance the donor from the ministry and turn giving into an abstract portfolio exercise. The heart-level risk is not administrative; it is relational and spiritual.

Donors who use intermediaries should intentionally preserve the biblical texture of generosity: meaningful attention to the people served, honest engagement with outcomes, and prayerful discernment about where giving should be concentrated. Administrative convenience should not become a substitute for love of neighbor.

Scrutinize how the ministry communicates impact and limitations

Strong ministries do not only report successes. They acknowledge limits, describe trade-offs, and show how learning shapes practice. In the broader nonprofit field, leaders have publicly challenged simplistic metrics and shallow donor expectations. The “Overhead Myth” statement—signed by Charity Navigator, GuideStar, and BBB Wise Giving Alliance—argues that judging charities by overhead ratios alone is misguided and can harm effectiveness. The Overhead Myth.

For Christian donors, the question is not whether a ministry spends “too much” on administration, but whether it demonstrates integrity, competence, and outcomes consistent with its mission and claims. Stock gifts and other complex giving vehicles make these questions more pressing because they require stronger internal systems.

How The Most Trusted Standard clarifies what stock giving requires

Giving appreciated stock vs. cash is partly about tax efficiency, but it is also about whether the receiving ministry has the maturity to handle complexity without compromising integrity. The Most Trusted Standard provides a disciplined way to assess that maturity across multiple dimensions that donors should care about.

In our verification work, several criteria tend to matter most when a ministry receives stock gifts or other noncash contributions: governance oversight of financial decisions, the clarity of written policies, the credibility of financial reporting, and transparent communication with donors. When these elements are weak, donors can unintentionally fund confusion rather than mission.

Financial integrity without theatrics

Noncash gifts require clean accounting. A ministry should acknowledge the gift according to appropriate standards, refrain from assigning valuations it is not qualified to assign, and issue donor receipts that are accurate and compliant. Donors, for their part, should not ask ministries to do things they should not do, such as providing appraisals or tax advice beyond basic procedural information. The IRS provides clear guidance on substantiation and the donor’s responsibility for valuation in many cases. IRS Publication 561: Determining the Value of Donated Property.

When a ministry is disciplined here, it typically reflects a broader seriousness about truthfulness—an ecclesial virtue with financial implications.

Governance that can say no

One underappreciated hallmark of strong governance is the ability to decline a gift that would create disproportionate risk or distraction. A ministry that accepts every offered asset is not necessarily generous; it may be undisciplined. A gift acceptance policy gives a board and leadership team a framework to protect the mission and the donor.

Christian donors sometimes interpret any reluctance as ingratitude. In practice, reluctance can be wisdom. A ministry that can say, “We are not equipped to receive that asset responsibly,” may be demonstrating integrity rather than weakness.

Transparency that treats donors as responsible adults

Mature donors are not asking for perfection. They are asking for honest information and credible processes. Ministries should be able to explain how stock gifts are received, sold, recorded, and used. They should be able to articulate whether they hold securities, why, and under what oversight. Transparency is not merely a fundraising tactic; it is a moral posture consistent with walking in the light (1 John 1:7).

When donors see that posture consistently—financially, theologically, and operationally—they can give with deeper freedom.

FAQs for Giving Appreciated Stock vs. Cash: Which Helps Ministries More?

Is it always better to give appreciated stock instead of cash?

No. Appreciated stock is often more tax-efficient, but cash can be more helpful when a ministry needs immediate operating support, when it cannot receive securities efficiently, or when the stock gift would create administrative complexity that consumes staff time. The most faithful gift is the one that genuinely strengthens the ministry’s capacity to serve.

Should a ministry hold donated stock or sell it immediately?

Many nonprofits adopt a policy to liquidate donated securities promptly to reduce market risk and avoid turning a charitable gift into an investment decision. Donors can ask whether the ministry has a written “sell promptly” policy and who is authorized to execute sales. Prudence and accountability are appropriate expectations for Christian donors.

What documentation should donors expect when giving stock?

Donors should expect a contemporaneous written acknowledgment from the ministry that describes what was donated and the date received, without the ministry assigning a value it is not responsible to provide. Donors should also ensure they meet IRS substantiation requirements and understand when additional forms apply. The IRS charitable giving guidance is the authoritative reference point. IRS: Charitable contributions.

How can donors evaluate whether a ministry will handle stock gifts responsibly?

Donors can ask for the ministry’s gift acceptance policy, confirm that there is board-level oversight of financial controls, and look for transparent financial reporting that matches public claims. Verification work, such as Most Trusted’s evaluations against The Most Trusted Standard, is designed to reduce uncertainty by assessing governance, financial integrity, and transparency practices that become especially important with noncash gifts.

Giving with fewer hidden losses and greater confidence

Giving appreciated stock vs. cash is ultimately about aligning means with mission. Appreciated stock can preserve more value for ministry by reducing avoidable tax loss, but only when the receiving ministry has the readiness and integrity to receive and liquidate the gift responsibly. Cash can be the truest form of help when time, simplicity, and operational stability are the ministry’s immediate needs.

Christian donors are not called to guess. We are called to wise stewardship, truthful dealing, and love of neighbor expressed through concrete, accountable generosity. When donors choose the giving vehicle that best serves the ministry’s work—and verify that the ministry can handle the gift with integrity—generosity becomes not only larger, but cleaner.