What tax forms Christian donors need for gifts is not an administrative afterthought; it is part of faithful stewardship. The same Scripture that calls us to give “not reluctantly or under compulsion” (2 Corinthians 9:7) also commends honesty and order, including in the way we report and substantiate our generosity.

The modern tax code can feel spiritually distracting, as though paperwork is competing with worship. Yet the discipline of good records protects givers and ministries alike. It reduces confusion, prevents unforced errors, and discourages the kind of financial opacity that discredits gospel work.

Start with the core question: what did you give and what did you receive

For U.S. federal taxes, the documentation you need depends less on your intentions than on the form of your gift and whether you received anything of value in return. The IRS distinguishes between a charitable contribution and a transaction with a partial benefit. That distinction shapes which receipts you need and what a ministry must disclose.

At a high level, donors generally rely on two streams of documentation: what the ministry provides (a contemporaneous written acknowledgment) and what you retain (bank records, payroll records, appraisals, and, for noncash gifts, certain tax forms). Most donors do not need a “tax form from the charity” in the way they expect a W-2 from an employer; the burden is largely substantiation and reporting.

The baseline records most donors should keep

- Bank record for any cash gift (cancelled check, bank statement, or credit card statement)

- Payroll record for any paycheck withholding gift (pay stub, W-2, or employer record)

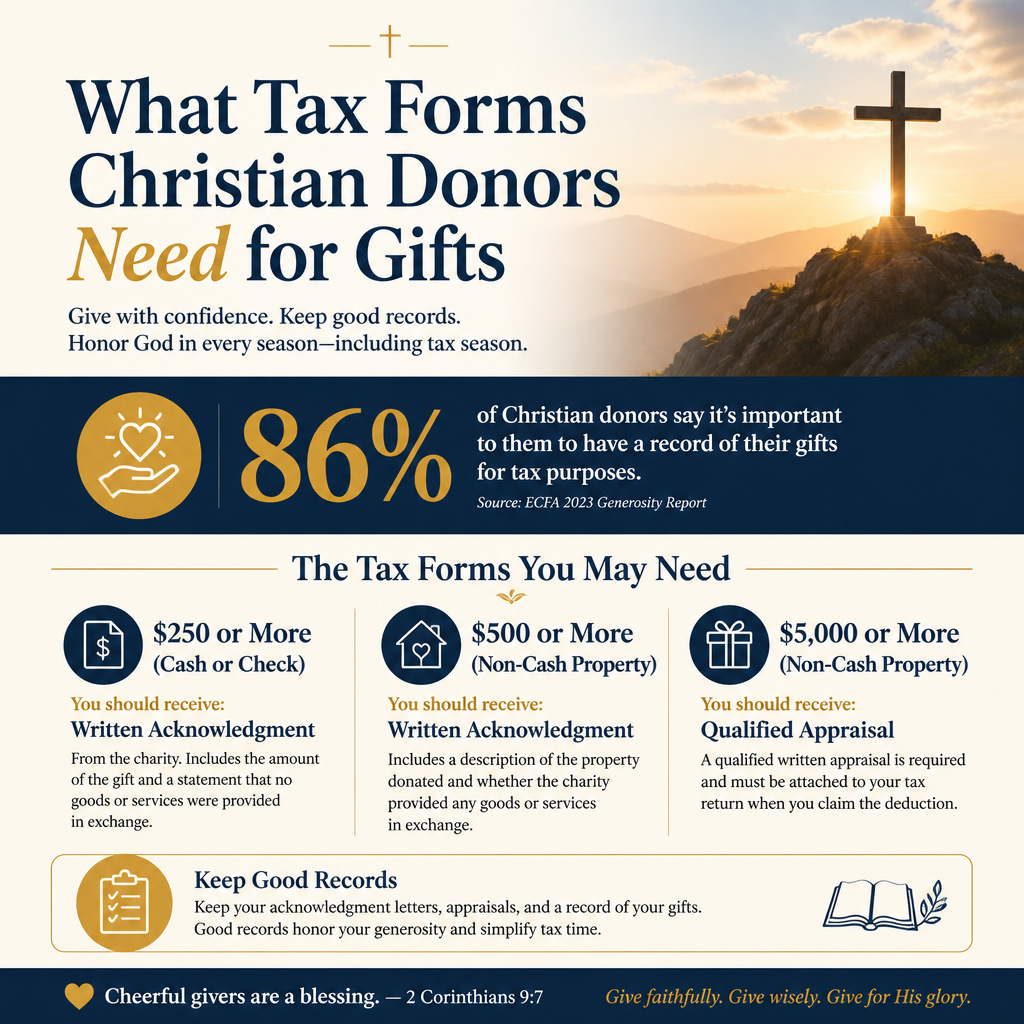

- Written acknowledgment from the ministry for gifts of $250 or more

- Written disclosure from the ministry when a gift includes a goods-or-services benefit

- For noncash gifts, a clear description of what was donated and how value was determined

What this means in practice is that your “file” for charitable giving is built across the year, not recreated at tax time. Mature ministries help by issuing clear, timely year-end statements, but the IRS standard is not “a year-end statement exists.” It is whether you can substantiate the gift under the specific rule that applies.

Itemizing remains a gating question

Under current law, most households take the standard deduction, which means many donors receive no federal income tax benefit from their charitable giving in a given year. The IRS publishes annual updates to standard deduction amounts and other parameters; donors should consult current figures when planning year-end giving and tax strategy. See the IRS’s official guidance at IRS.gov.

Christians genuinely disagree about how much tax strategy should shape giving decisions. The better question is whether our approach makes generosity more consistent and more discerning without turning ministry into a tax shelter. Tax documentation serves the integrity of giving, not the other way around.

Cash gifts: bank records, plus acknowledgments for larger gifts

For cash gifts made by check, card, or electronic transfer, the IRS expects a bank record showing the name of the charity, the date, and the amount. For gifts of $250 or more to a single organization, you also need a contemporaneous written acknowledgment from the charity. This acknowledgment must include the amount contributed and a statement that no goods or services were provided in exchange, or a good-faith estimate of their value if they were. The IRS outlines these requirements in its charitable contributions guidance at IRS Charitable Contributions.

What a proper acknowledgment should contain

Donors sometimes assume that a year-end statement is always sufficient. Often it is, but the content matters. A compliant acknowledgment generally includes the donor’s name (not required by the IRS but common), the date and amount of the contribution, the charity’s name, and the required “goods and services” language. If you purchased a banquet seat, received merchandise, or received another benefit, the charity should disclose the deductible portion and estimate the fair market value of what you received.

Quid pro quo gifts: when a benefit changes the documentation

If you make a payment partly as a contribution and partly in exchange for goods or services—such as a fundraising dinner—your deduction is generally limited to the amount exceeding the fair market value of the benefit received. Ministries have disclosure obligations for certain quid pro quo contributions. The IRS provides the governing framework at IRS Quid Pro Quo Contributions.

Many Christian ministries work hard to keep fundraising benefits modest and to disclose them clearly. That discipline reflects more than compliance; it reflects an ethical posture that refuses to blur the line between Christian giving and religious consumerism.

Noncash gifts: when you need Form 8283 and, sometimes, a qualified appraisal

Noncash giving often aligns with thoughtful stewardship—giving appreciated assets rather than cash, donating property that can be put to use, or clearing an estate with purpose. It is also where documentation becomes more technical. Donors should expect to shoulder more of the substantiation burden, especially as gift values rise.

Form 8283: Noncash Charitable Contributions

If you claim a deduction for noncash charitable contributions above certain thresholds, you may need to file IRS Form 8283 with your return. Depending on the type and value of the property, the form may require a signature from the receiving organization and, for some gifts, information from a qualified appraisal. The IRS provides the form and instructions at About Form 8283.

The harder question is not whether Form 8283 is inconvenient, but whether your giving plan is disciplined enough to treat complex gifts with appropriate care. When documentation is rushed, donors can lose legitimate deductions, and ministries can face avoidable follow-up and reputational strain.

Qualified appraisals and special property rules

Donations of closely held business interests, certain real estate, valuable collectibles, and other property classes can require a qualified appraisal and additional substantiation. Separate rules apply to vehicles and to certain inventory or intellectual property. These are not merely technicalities. They are the mechanisms the tax code uses to prevent inflated valuations and to ensure donors and charities report consistently.

Because the rules vary by asset class, donors should consult the IRS guidance and work with a tax professional when making significant noncash gifts. The IRS provides a central overview of substantiation requirements at IRS Publication 526.

Required Minimum Distributions and retirement giving: when the form is not the receipt

Retirement assets are a common source of late-life generosity. They are also one of the most misunderstood areas of charitable documentation. A Qualified Charitable Distribution (QCD) from an IRA can be a powerful way to give, but it is not deducted the same way as a cash gift from a checking account. Instead, it is generally excluded from income when done correctly, subject to IRS rules.

QCD documentation: what you should actually expect

For a QCD, you typically receive Form 1099-R from your IRA custodian, reporting the distribution. The custodian does not generally designate it as charitable on the 1099-R; you and your preparer reflect the exclusion on your tax return. You still need a written acknowledgment from the receiving charity, similar to other charitable gifts. The IRS provides QCD guidance at IRS IRA distribution FAQs.

Donors sometimes assume that because the funds never touched their checking account, a receipt is unnecessary. In practice, the same discipline applies: obtain the ministry’s acknowledgment and keep records showing the transfer was completed.

Employer matching and donor-advised funds: know who the donor is for tax purposes

When a gift is made through a donor-advised fund (DAF), the donor for tax purposes is typically the sponsoring organization, not the individual recommending the grant. Your personal deduction generally occurs when you contribute to the DAF, not when the DAF grants to a ministry. Similarly, if your employer matches your gift, you generally deduct your own contribution, while the employer’s match is the employer’s contribution. These arrangements can deepen generosity, but they also require clarity about who receives which receipt and which entity claims a deduction.

Many donors engaging in these structures also care deeply about ministry credibility and reporting standards. That is one reason our team at Most Trusted evaluates ministries against The Most Trusted Standard, a 15-criteria framework that includes financial integrity, governance, and transparency. Discernment about where to give and discipline about how to document giving belong together.

What to expect from healthy ministries: receipts, disclosures, and governance that support compliance

Donors cannot control a ministry’s internal systems, but donors can decide what they will tolerate. Across our verification work, we observe that ministries with mature financial operations tend to issue acknowledgments promptly, explain quid pro quo benefits without evasiveness, and provide year-end summaries that reconcile to actual gifts received. These practices serve both donor confidence and regulatory compliance.

Receipting practices that signal maturity

Receipts are not proof of holiness, but chronic sloppiness is rarely confined to receipting. When acknowledgments omit required language, when values are inflated, or when a ministry cannot reconcile donor statements to deposits, donors should pause. Such patterns can indicate weak internal controls or an organizational culture that treats accountability as optional.

Transparency is not a substitute for faithfulness, but Scripture does commend taking care to do what is right “not only in the eyes of the Lord but also in the eyes of man” (2 Corinthians 8:21). That text is not about public relations. It is about preventing avoidable suspicion and protecting the integrity of gospel work.

Where Most Trusted fits within donor diligence

Tax documentation answers the question, “Can we substantiate what we gave?” Verification answers a different question: “Is this ministry credible, governed responsibly, and financially transparent?” Donors who want to take stewardship seriously often attend to both. For the broader context of evaluating ministries and stewardship practices, see Christian Stewardship Services.

When giving decisions intersect with tax planning—especially year-end giving, noncash assets, or retirement distributions—donors also benefit from understanding the particular risks and opportunities that come with tax-smart generosity. The relevant considerations are addressed in Tax-Smart Giving Through Christian Stewardship Services.

FAQs for What tax forms Christian donors need for gifts

Do charities send donors a tax form like a W-2 or 1099 for donations?

Typically no. For charitable contributions, donors generally rely on their own bank or payroll records, plus a contemporaneous written acknowledgment from the charity for contributions of $250 or more. For certain noncash gifts, donors may also file Form 8283 with their tax return. The IRS explains substantiation requirements in its charitable contributions guidance at IRS Charitable Contributions.

What form do we need if we donated noncash items or property?

Depending on the type and value of the noncash gift, you may need to file IRS Form 8283 and, for some gifts, obtain a qualified appraisal and a charity signature on the form. Documentation requirements vary by property type and valuation thresholds. The IRS provides the form and instructions at About Form 8283.

Giving that is generous and orderly

Christian donors should not have to choose between heartfelt generosity and careful documentation. The tax forms and receipts involved in charitable giving exist to substantiate truth: what was given, to whom, and under what conditions. When we keep records carefully and support ministries that operate transparently, we strengthen the credibility of our giving and the witness of the work it funds.