How do Christian donors maximize charitable deductions without turning generosity into a tax tactic? The question matters because Scripture treats money as spiritual formation, not a neutral tool, and yet tax law is one of the ordinary structures through which Christians can fund long-term faithfulness.

Wise planning does not replace cheerful giving; it removes avoidable friction so more resources can reach faithful work. The harder question is integrity: giving in ways that honor the Lord, withstand scrutiny, and strengthen ministries rather than incentivizing shortcuts. That is where disciplined documentation, careful selection of recipients, and sober attention to IRS rules belong in a Christian stewardship practice.

Begin with a theology of stewardship that can bear weight

Tax planning is secondary but not trivial

Jesus’ warnings about mammon were not aimed at accounting competence. They were aimed at divided allegiance. Christian donors therefore do not pursue charitable deductions as a proxy for generosity, and we do not excuse stinginess by pointing to a tax receipt. At the same time, Scripture commends prudence: counting the cost, planning ahead, and ordering one’s household well. Tax law is part of that “counting,” and Christians can treat it as a legitimate context for stewardship rather than an embarrassment.

What this means in practice is that deduction strategy should follow convictions about mission. Deduction strategy should not determine mission. When that order is reversed, donors often drift into funding what is easiest to document, easiest to explain, or most emotionally compelling, rather than what is most faithful and effective.

Give in ways that strengthen trust, not only budgets

Across our verification work at Most Trusted, we observe that donor confidence rises when ministries can demonstrate clear faith commitments, sound governance, responsible financial management, and honest reporting. Those priorities align with The Most Trusted Standard, and they also protect donors from the quiet moral hazard of “tax-smart giving” to organizations that cannot account for funds with rigor.

Maximizing deductions should therefore sit inside a broader aim: giving that is defensible before God and neighbor. For donors who want a wider frame for this work, the broader context of Christian Stewardship Services is where many begin to put the pieces together in a coherent practice.

Know the IRS rules that shape what is deductible

Itemizing, standard deductions, and when deductions matter

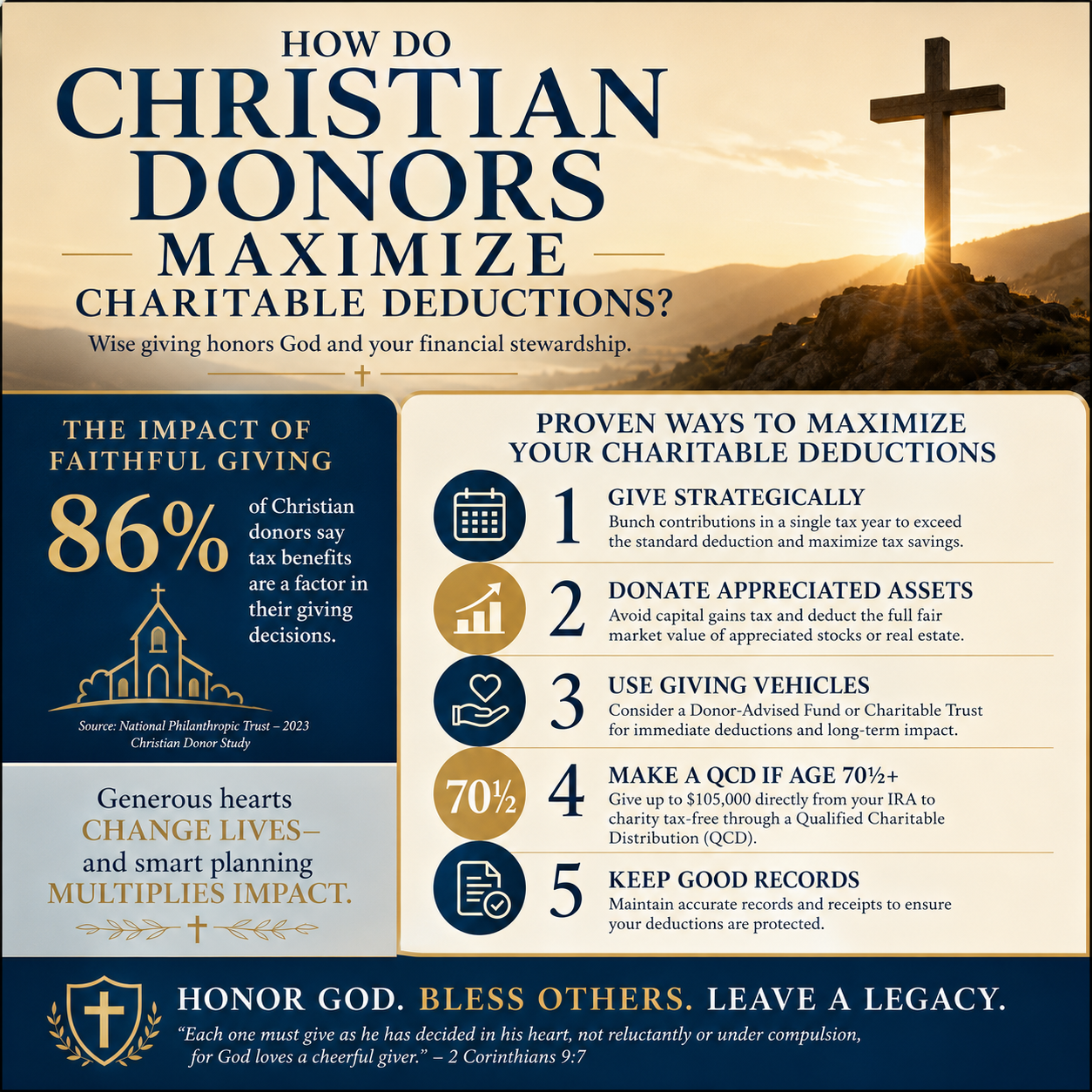

For many households, charitable giving does not change federal taxable income because they take the standard deduction rather than itemizing. Since the Tax Cuts and Jobs Act, the share of taxpayers who itemize has dropped sharply; the Tax Policy Center estimated that about 10% would itemize under the post-TCJA framework, down from roughly 30% prior to the law (Tax Policy Center). Christian donors who want to maximize deductions should therefore start with a clear annual projection: will we itemize this year, and if not, what planning options could legitimately move us into itemizing without distorting our giving?

“Bunching” is one common approach: concentrating multiple years of giving into a single tax year to exceed the standard deduction threshold, then taking the standard deduction in the intervening years. This can be paired with donor-advised funds or other giving vehicles, but the moral question remains: does the timing change the ministry’s cash flow in harmful ways? Mature donors consider the ministry’s operating reality, not only the donor’s return.

Documentation is not bureaucracy, it is accountability

The IRS largely treats charitable deductions as a documentation problem. The rules are specific: for any cash contribution, the donor must keep a bank record or written communication from the charity showing the charity’s name, the date, and the amount. For any single contribution of $250 or more, the donor must have a contemporaneous written acknowledgment from the charity before filing the return (IRS Publication 526).

That paperwork burden can feel spiritually misaligned, but it has a constructive side. When ministries issue timely, accurate acknowledgments—and when donors keep records carefully—both parties practice transparency. It becomes harder to launder personal expenses through “ministry” giving, harder to inflate valuations, and harder for poorly governed organizations to skate on ambiguity.

Choose giving methods that increase after-tax impact

Give appreciated assets when appropriate

Many Christian donors unintentionally give in the least efficient form: cash, even when they hold highly appreciated assets. In many cases, donating long-term appreciated securities can allow a donor to deduct fair market value (subject to IRS limits) and avoid capital gains tax that would be triggered by selling first. The specific outcome depends on income level, holding period, and the nature of the recipient organization, so donors should coordinate with a CPA or qualified advisor.

The key stewardship insight is straightforward: if two gifts fund the same ministry work, but one transfers a larger portion of the asset’s value to the mission rather than to taxes, that method can be more faithful. The caution is equally important: complex asset gifts require competent processing by the receiving organization, and not every ministry is set up to receive them well.

Use qualified charitable distributions for certain retirees

For donors age 70½ or older, qualified charitable distributions (QCDs) from IRAs can be a powerful tool. QCDs can satisfy required minimum distributions and keep the distribution out of taxable income, which can matter for Medicare premium calculations and taxation of Social Security benefits. The rules are technical and timing-sensitive, and the gift must go directly from the IRA custodian to a qualified charity; donor-advised funds are generally not eligible recipients for QCDs. Donors should confirm current rules with the IRS and their advisor (IRS IRA distribution FAQs).

Christians genuinely disagree about how much energy to spend on these tools. Some prefer simplicity and accept tax inefficiency as part of their sacrifice. Others see careful planning as a way to increase giving capacity. Both positions can be held with integrity; what should not be lost is the responsibility to comply carefully with the law and to avoid self-deception about motives.

Match tax strategy with verified ministry integrity

Tax deductibility is not moral credibility

In the United States, 501(c)(3) status is a legal classification, not a theological endorsement and not a guarantee of operational integrity. Deductibility tells a donor that the IRS recognizes an entity as eligible for tax-deductible contributions. It does not tell a donor whether the ministry handles funds honestly, whether governance is independent, whether reporting is candid, or whether programs produce fruit consistent with stated mission.

That gap matters for Christian donors precisely because giving is discipleship. A donor who plans carefully for deductions but gives to an unaccountable ministry has not practiced full stewardship; they have simply arranged their paperwork efficiently.

Do due diligence that respects both faith and evidence

Most ministries are sincere, and many do difficult work under real constraints. The field has also had to reckon with recurring failures: weak boards, opaque related-party transactions, inflated impact reporting, and doctrinal ambiguity masked by marketing. Discernment is not cynicism; it is love of neighbor expressed through truth.

In our work, The Most Trusted Standard evaluates ministries across 15 criteria covering faith commitments, financial integrity, governance and leadership, and transparency and effectiveness. The aim is not to replace prayerful discernment, but to discipline it with evidence. This is the same posture we commend when donors pursue tax-smart giving: spiritual seriousness joined to verifiable accountability.

Plan annually with clarity and humility

Coordinate giving, cash flow, and family discipleship

Maximizing charitable deductions is not only an April problem; it is a year-round practice. Households that plan well typically decide, early in the year, how giving fits into a broader budget, what ministries will be prioritized, and what vehicles will be used. They also account for cash flow realities of the ministries they support. A small church or frontline mission often cannot absorb extreme year-to-year volatility without program disruption.

There is also a discipleship dimension: spouses should plan together, and when children are old enough, they should understand why the household gives, not only where it gives. The aim is not to produce mini-accountants; it is to form Christians who can connect money, worship, and neighbor-love.

A practical year-end checklist

The following actions are often where mature donors prevent avoidable loss of deduction value and avoid compliance errors:

- Confirm whether you will itemize this year and whether a deliberate timing plan is appropriate.

- Collect contemporaneous written acknowledgments for any single gift of $250 or more, before filing.

- Review whether appreciated asset gifts or QCDs fit your situation and whether the recipient can receive them cleanly.

- Verify recipient eligibility and integrity, especially for smaller or newer ministries with limited public reporting.

- Align giving commitments with ministry cash flow needs, not only year-end tax timing.

Many donors also find it useful to place their tax-planning decisions inside a wider stewardship practice that includes due diligence and disciplined generosity. The specific tools and constraints that shape Tax-Smart Giving Through Christian Stewardship Services can support that kind of integrated approach when handled with care.

FAQs for How do Christian donors maximize charitable deductions

Should Christians change their giving timing to get a bigger deduction?

It can be appropriate, especially when bunching gifts into an itemizing year meaningfully increases after-tax resources available for ministry. The moral test is whether the timing change harms the ministries you support or subtly reshapes your priorities toward what is most tax-efficient rather than most faithful. When timing strategies create instability for a ministry’s operating budget, donors can pair a larger year-end gift with a communicated plan for predictable support.

Is giving to any 501c3 enough, or should donors do deeper due diligence?

501(c)(3) status is a baseline legal threshold, not a measure of spiritual or operational integrity. Christian donors have reason to look for evidence of sound governance, clear faith commitments, and transparent reporting, especially when gifts are substantial or when a ministry has limited public documentation. Verification frameworks, audited financials, independent boards, and candid impact reporting are all signals that a ministry takes stewardship seriously.

A faithful approach to deductions keeps the mission first

Christian donors maximize charitable deductions most responsibly when tax planning serves discipleship rather than substituting for it. The goal is not to “win” against the IRS or to sanctify self-interest, but to remove avoidable waste, comply carefully with the law, and direct resources toward ministries that can be trusted with them. When generosity is guided by Scripture and disciplined by evidence, tax strategy becomes one small part of a larger vocation of stewardship.