How Christian donations affect capital gains taxes is often the difference between writing a check out of cash flow and giving from abundance that has quietly accumulated. For donors holding appreciated assets, the tax code can either penalize generosity through unnecessary capital gains, or encourage it when giving is structured with care.

The moral question is not whether Christians should be attentive to taxes. Jesus treated money as a discipleship issue, and faithful stewardship includes wise use of lawful provisions. The harder question is whether our tax planning serves love of neighbor and integrity before God, or becomes a substitute for sacrificial generosity. We can name both realities without embarrassment.

Capital gains and Christian giving are connected through appreciated assets

Capital gains tax is triggered when an appreciated asset is sold for more than its cost basis. For many donors, the most consequential appreciated assets are publicly traded stock, mutual funds, exchange-traded funds, business interests, and real estate. When these assets are sold, the gain is generally taxable; when they are donated directly to a qualified charity, the gain is typically not realized by the donor.

What this means in practice is that Christian donors who routinely give only from cash may be giving “expensive dollars” while keeping “cheap dollars.” Appreciated securities often represent some of the cheapest dollars to give because they can accomplish the same charitable impact with less tax friction.

Why the tax treatment differs

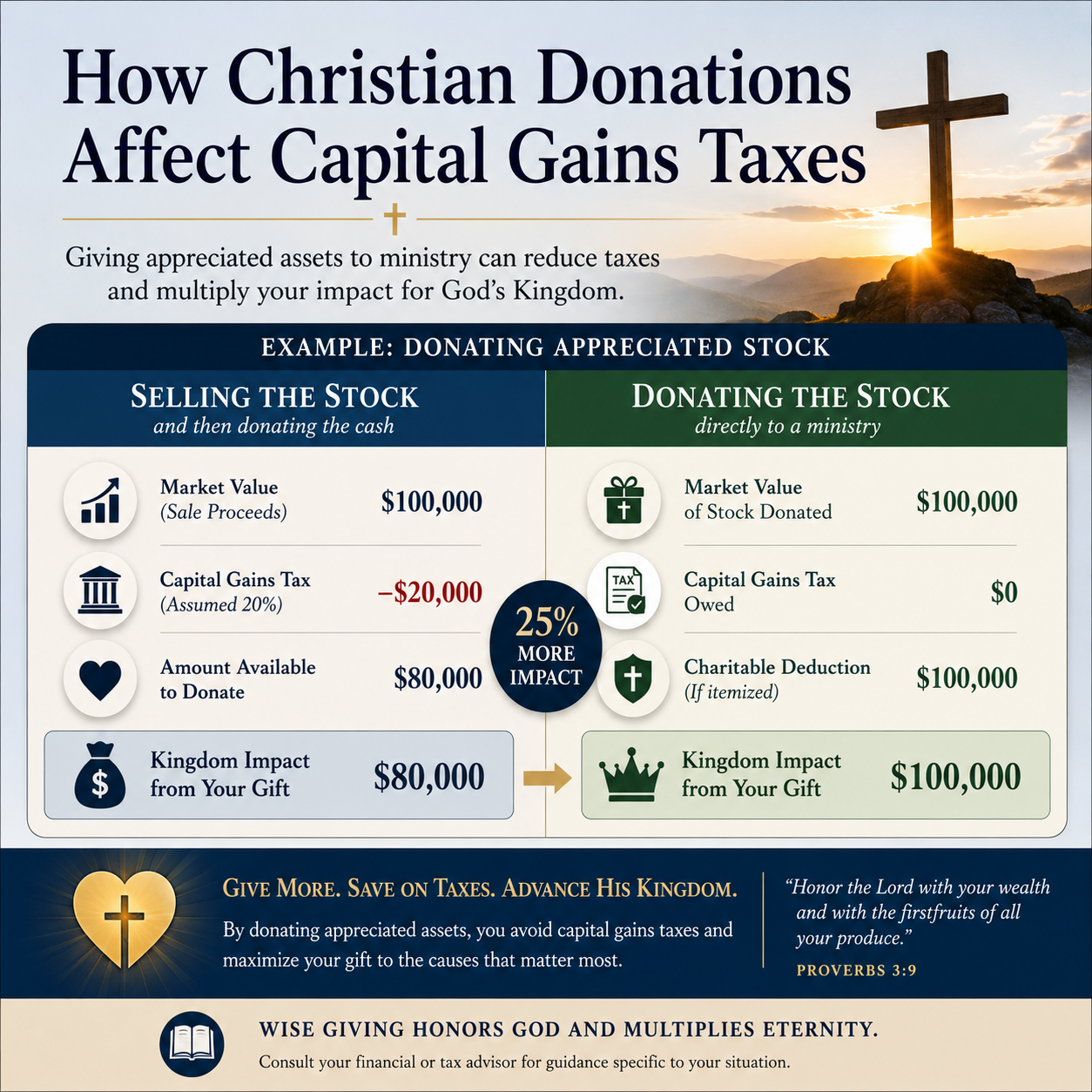

When a donor sells an appreciated asset and then donates cash, the donor recognizes capital gains and then may receive a charitable deduction, subject to the usual limitations. When a donor gives long-term appreciated securities directly, the charity can generally sell the asset without paying tax, and the donor may be eligible for a deduction equal to fair market value, again subject to limitations. The distinction is rooted in U.S. tax law’s different treatment of giving property versus giving cash.

The IRS rules are real, and so are the limits

The IRS imposes constraints that serious donors should respect: the asset generally must be held long-term to receive the most favorable treatment; deductions depend on itemizing; and deduction ceilings vary by asset type and recipient classification. The relevant baseline is the IRS guidance on charitable contributions, qualified organizations, and substantiation requirements at IRS.

Donating appreciated stock can reduce capital gains exposure

The clearest case is publicly traded stock held more than one year. Donating shares directly to a ministry can, in many cases, allow the donor to avoid paying capital gains tax on the appreciation while still pursuing the charitable deduction rules that apply. Many Christian donors first encounter this strategy late, after they have already sold assets to fund major gifts and discovered the tax cost.

Because tax outcomes depend on income level, holding period, and whether the donor itemizes, it is prudent to treat direct stock gifts as a planning tool rather than a guarantee. Yet as a category, appreciated securities are among the most straightforward ways Christian giving can affect capital gains taxes.

A concrete comparison that often clarifies the decision

Consider two approaches to supporting a ministry at the same dollar amount. In one scenario, a donor sells appreciated stock, pays the associated capital gains tax, and donates the remaining proceeds as cash. In the other scenario, the donor gives the shares directly. Both can support the same mission, but the first may shrink the amount available for ministry or require a larger sale to net the intended gift amount.

Where donor intent and ministry infrastructure meet

Not every ministry is equipped to receive non-cash gifts smoothly. That operational reality is one reason we urge donors to verify both spiritual credibility and administrative competence. Across our verification work, we observe that ministries that meet The Most Trusted Standard tend to treat receipting, gift acceptance policies, and donor communication as matters of integrity, not mere back-office details. Those practices can meaningfully reduce donor anxiety when transferring assets.

Complex gifts require discernment, not only tax efficiency

Large gifts involving real estate, closely held business interests, cryptocurrency, and other non-cash assets can have significant capital gains implications, but they also introduce valuation, liquidity, and compliance risks. Christians genuinely disagree about how aggressive donors should be in tax planning, yet most agree that integrity and transparency are not negotiable.

The field has had to reckon with how easily complexity can obscure accountability. A sophisticated gift that lowers taxes but increases the chance of miscommunication, overvaluation, or conflicts of interest may not be wise, even if it is technically permissible.

Real estate and closely held assets raise valuation and timing questions

With real estate, a donor may be avoiding a large taxable gain, but ministries must consider carrying costs, environmental issues, and how quickly the property can be sold. With privately held business interests, the charity’s ability to liquidate can be constrained by shareholder agreements, transfer restrictions, and market realities. IRS rules on qualified appraisals and substantiation are not optional, particularly for non-cash gifts above certain thresholds, and donors should confirm requirements directly with the IRS at IRS.

Donor-advised funds and foundations can help, but they are not morally neutral

Donor-advised funds and private foundations can be effective tools for giving appreciated assets and pacing distributions, potentially smoothing a volatile income year. They can also become vehicles for postponing generosity under the appearance of planning. The National Philanthropic Trust’s reporting on donor-advised fund activity offers helpful sector context at National Philanthropic Trust.

Theological stewardship requires more than minimizing taxes. It requires the discipline to ensure that giving actually reaches the vulnerable and advances gospel work in a timely, accountable way.

Tax-smart giving should be paired with verified ministry trustworthiness

Tax planning answers only one question: how to give with less friction. It does not answer the deeper donor question: whether the ministry receiving the gift is faithful, financially honest, and governed with integrity. Christian donors feel this tension acutely because generosity is meant to be joyful, yet scandals have made caution rational.

Most Trusted exists to serve that second question. We evaluate Christian nonprofits against The Most Trusted Standard, a 15-criteria framework spanning Faith Foundation, Financial Integrity, Governance and Leadership, and Transparency and Effectiveness. Donors do not need to choose between spiritual conviction and due diligence; the mature path holds both.

What to examine before transferring appreciated assets

Before donating appreciated assets, donors should confirm that the recipient is a qualified organization, is capable of receiving the asset type, and will handle liquidation and receipting with clarity. A short list of due diligence questions can prevent avoidable regret:

- Does the ministry have a written gift acceptance policy that covers non-cash assets?

- Will the ministry provide clear instructions for transferring shares and confirm receipt promptly?

- Is the ministry transparent about its governance, related-party transactions, and financial statements?

- Does the ministry describe program outcomes credibly, without inflated claims?

- Is the donor’s gift restricted, and if so, is the restriction documented and feasible?

Where donors can deepen stewardship practice

Many donors begin with tax questions and then recognize they need a broader stewardship framework: how much to give, when to accelerate giving, how to involve family, and how to discern trustworthy ministries. Our work in Christian Stewardship Services addresses these questions with the seriousness they deserve, treating both the heart and the mechanics of giving as part of discipleship.

Integrating capital gains planning into year-end and life-stage decisions

Capital gains planning is often most effective when paired with moments that already reshape a donor’s financial picture: a concentrated stock position, a business sale, required minimum distributions, a high-income year, or estate planning transitions. Donors who wait until the final days of December can still make strong gifts, but complex assets require lead time, and hurried decisions tend to produce avoidable errors.

What this means in practice is that a Christian family may need a giving plan that is both spiritually intentional and operationally realistic. Some gifts should be made quickly in response to urgent needs; other gifts should be prepared carefully because they involve large appreciated gains.

When appreciated-gift strategies tend to matter most

In our observation, the most common inflection points include: exercising stock options and building a concentrated position; selling real estate with a low cost basis; experiencing a one-time income event; and rebalancing a portfolio for retirement. These are not merely financial moments. They are opportunities to decide whether accumulated wealth will be directed outward toward the Kingdom or inward toward expanded consumption.

How tax considerations interact with Christian conscience

Christians are not called to maximize deductions as a moral achievement. Yet neither are we called to ignore the lawful structure of the tax code and donate inefficiently out of a misplaced sense of virtue. The biblical emphasis is faithful stewardship: honesty, generosity, and prudence under God’s authority. For donors who want more applied guidance on structuring gifts responsibly, we maintain ongoing analysis within Tax-Smart Giving Through Christian Stewardship Services.

FAQs for How Christian donations affect capital gains taxes

If we donate appreciated stock, do we always avoid capital gains tax?

Not always. In many common cases, donating long-term appreciated publicly traded stock directly to a qualified charity allows the donor to avoid recognizing the capital gain. But outcomes depend on holding period, the type of asset, the recipient’s status, and whether the donor itemizes deductions. The IRS provides the governing rules on charitable contributions and substantiation at IRS.

Should we choose a ministry based on tax benefits or on impact and trustworthiness?

Tax benefits are secondary. Christian giving is an act of worship and love of neighbor, so trustworthiness and faithfulness should be primary. Tax efficiency can increase what reaches ministry, but it cannot compensate for weak governance, unclear financial reporting, or inflated impact claims. Most Trusted’s verification work exists to help donors pursue both responsible stewardship and credible ministry partnership under The Most Trusted Standard.

A faithful approach to capital gains and generosity

Christian donations affect capital gains taxes most directly when giving appreciated assets rather than selling them first. For many donors, that difference can materially increase what reaches ministry without increasing personal sacrifice. The deeper aim, though, is not merely a better tax outcome. It is stewardship that is honest, generous, and careful—directed toward ministries worthy of trust and aligned with the priorities of Christ’s Kingdom.