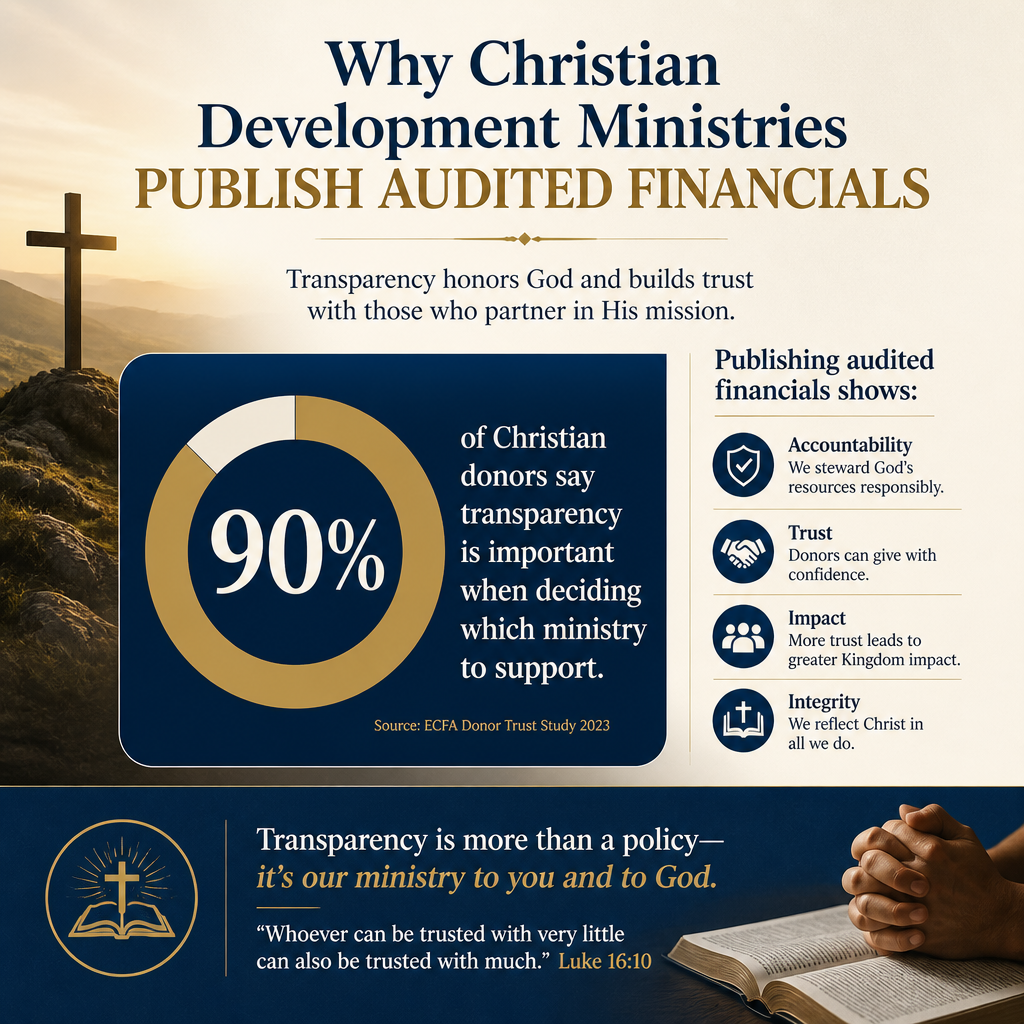

Why Christian development ministries publish audited financials is ultimately a question of stewardship: whether those entrusted with resources for the poor will submit their handling of those resources to disciplined, independent scrutiny. For Christian donors, audited financial statements are not a luxury good for large organizations; they are a tangible expression of accountability before God and neighbor.

Scripture treats money as moral terrain. Jesus’ warnings about mammon, the apostles’ insistence on honorable conduct, and the church’s historic concern for the vulnerable converge on a single principle: Christian compassion should be paired with integrity that can be shown, not merely claimed. Audited financials are one of the clearest ways a ministry can make that integrity verifiable without turning ministry into marketing.

Audited financials are a modern expression of an ancient biblical concern

Accountability protects the mission and the people served

Paul took pains to avoid even the appearance of mishandling funds collected for the poor. In arranging a delegation to accompany the offering, he wrote that he was taking these precautions “so that no one should blame us about this generous gift” and that the aim was what is honorable “not only in the Lord’s sight but also in the sight of man” (2 Corinthians 8:20–21). The passage does not describe a formal audit, but it does describe the underlying ethic: transparent processes that protect the ministry, the church, and the intended beneficiaries.

Audited financial statements sit in that same tradition. They do not prove spiritual maturity, and they cannot guarantee effectiveness. But they do establish that financial reporting is being tested against objective standards, and that leadership is willing to be examined rather than merely trusted.

Audit discipline is especially relevant in cross-cultural development

Christian relief and development work routinely operates across borders, currencies, partner networks, and complex compliance regimes. Those realities increase both operational risk and the opportunity for error or abuse. The stronger a ministry’s controls and reporting discipline, the more confidently a donor can support work that is geographically distant and therefore harder to observe directly.

Many donors begin with the category of Christian Relief and Development Ministries because the needs are urgent and the biblical mandate is clear. The same clarity should be applied to how funds are governed, recorded, and reported.

What an audit is and what it is not

Audit is independent assurance, not internal confidence

A financial statement audit is performed by an independent Certified Public Accountant firm. The auditor’s purpose is to provide reasonable assurance that the financial statements are free from material misstatement and prepared in accordance with an appropriate accounting framework, often U.S. GAAP for U.S.-based ministries. “Reasonable assurance” matters: an audit is designed to detect material issues, not every minor error, and it is not a guarantee that fraud is impossible.

That limitation is not a weakness; it is the nature of professional assurance. The presence of an audit should prompt better questions, not end inquiry. Sophisticated donors treat the audit as a starting point for understanding governance, controls, and transparency.

Review and compilation are different levels of assurance

Some ministries publish reviewed or compiled statements rather than audited financials. A review provides limited assurance, based primarily on inquiry and analytical procedures. A compilation provides no assurance; it is a presentation of information provided by management. There are legitimate reasons smaller ministries may begin with these steps, especially when budgets are tight. The donor question is not whether a ministry is “hiding something,” but whether its level of external scrutiny matches the scale and complexity of its operations.

In our verification work at Most Trusted, we see healthier patterns when ministries treat progression toward an audit as part of organizational maturation rather than as an optional public-relations exercise.

How audited financials protect donors from common failures

They expose weak controls before a scandal does

Many ministry failures are not the result of blatant malice; they begin with preventable weaknesses. Segregation of duties, approval workflows, cash handling, reimbursement policy, and vendor oversight all become fragile when an organization grows quickly or works in high-cash environments. Auditors test internal controls and financial assertions, and they often issue management letters that identify control deficiencies. A ministry that takes those findings seriously is typically strengthening its ability to serve beneficiaries over the long term.

The alternative is often a painful cycle: donors give generously, growth outruns internal systems, and the ministry experiences a crisis that harms both reputation and programs. Audited financials are one of the few tools that help ministries confront these risks early.

They clarify where costs actually go without feeding the overhead myth

Christian donors frequently want to know what portion of a gift reaches programs. That is a legitimate stewardship concern, yet the sector has also had to reckon with simplistic “overhead” judgments that penalize necessary investments in staff, systems, and compliance. In 2013, Charity Navigator, GuideStar, and the BBB Wise Giving Alliance publicly warned donors against using overhead ratios as the sole measure of charity performance, arguing that such pressure can lead nonprofits to underinvest in infrastructure and transparency (GuideStar).

Audited financials help donors hold two truths together: donors should not be manipulated by inflated “program percentage” claims, and donors should not assume that low overhead is automatically virtuous. A well-run development ministry may legitimately spend meaningful resources on monitoring and evaluation, safeguarding, partner due diligence, cybersecurity, and finance functions. These are not distractions from ministry; they are part of loving stewardship.

What donors should look for when a ministry publishes audited financials

The audit opinion and the notes, not only the summary numbers

A ministry can post audited statements and still leave donors confused if it does not help them read them responsibly. Donors do not need to become accountants, but several elements are worth attention:

- The auditor’s opinion: Unmodified is generally strongest; modified opinions require careful follow-up.

- Going concern language: Signals significant doubt about the organization’s ability to continue operating without major changes.

- Related-party transactions: Not inherently wrong, but they require clarity and strong governance safeguards.

- Restricted versus unrestricted net assets: Indicates how much of the ministry’s resources are flexible for general operations.

- Revenue concentration: Heavy dependence on a small number of donors or a single funding stream can increase vulnerability.

For Christian donors deciding how to give, these are not merely technicalities. They are indicators of whether a ministry has the stability and integrity to steward gifts through disruption, leadership transitions, and crises.

Consistency over time and congruence with public claims

We recommend reading at least two to three years of audited financials when available. Patterns matter more than one-year snapshots. Is the organization persistently drawing down reserves? Are fundraising expenses rising sharply without corresponding growth in revenue? Are administrative costs unusually low in a way that suggests underinvestment in basic controls?

Congruence also matters. If a ministry’s marketing emphasizes rapid scale, field expansion, and large capital projects, but audited statements show recurring losses or unstable cash flow, that mismatch warrants caution. Mature ministries speak plainly about both fruitfulness and constraints.

Why some ministries resist audits and how donors should respond

Cost is real, but so is the cost of not being audited

Audits are expensive, and for small ministries the cost can feel disproportionate. There is a legitimate tension here: every dollar spent on professional services is a dollar not spent directly on programs. Yet the moral question is not simply “audit or no audit.” The deeper question is what level of financial assurance is owed to donors and beneficiaries when a ministry asks the church to entrust it with significant resources.

For ministries operating in fragile contexts, the cost of weak systems can be far higher than the audit fee. Misstatements, compliance failures, or preventable fraud can disrupt programs, jeopardize partners, and damage the credibility of Christian witness. Donors can reasonably ask whether the ministry has a plan to reach audit-level accountability as it grows.

Some leaders fear misinterpretation, and donors should insist on clarity anyway

Another common resistance is that audited statements may be misunderstood by supporters or weaponized by critics. That concern is not imaginary. Financial statements can be read in bad faith, and complex organizations can be reduced to simplistic talking points. But withholding audited financials because they might be misread is not a mature solution. Mature leadership teaches donors how to read the documents, explains anomalies, and welcomes questions.

Donors who want to give responsibly often benefit from a broader set of evaluation signals, including governance practices, conflict-of-interest policies, leadership accountability, and transparency norms. Many donors pursue this through How to Give Wisely to Christian Relief and Development Ministries because it frames financial integrity as part of a larger Christian stewardship posture rather than as a narrow compliance exercise.

At Most Trusted, our evaluations are built around The Most Trusted Standard, a 15-criteria framework that examines faith foundation, financial integrity, governance and leadership, and transparency and effectiveness. Audited financials are not the whole story, but they are a durable piece of verifiable evidence that a ministry’s public claims about stewardship are anchored in accountable practice.

FAQs for Why Christian development ministries publish audited financials

Does a clean audit mean a Christian development ministry is trustworthy?

A clean audit is a meaningful positive signal, but it is not a comprehensive trust verdict. An audit provides reasonable assurance about whether financial statements are materially accurate, not whether programs are effective, whether leadership culture is healthy, or whether governance is strong. Wise donors treat audited financials as one component in a wider evaluation of transparency, oversight, and ministry fruitfulness.

What if a ministry is small and says it cannot afford an audit?

Cost can be a legitimate constraint, especially for newer organizations. Donors can ask what level of external financial assurance the ministry does provide, whether it has a finance committee or qualified oversight, and whether it has a time-bound plan to move toward an audit as revenue grows. When the scale of funds is significant or operations are complex, it is reasonable to expect the discipline and independence that an audit provides.

Stewardship that can be examined

Christian donors do not give merely to fund activity; we give to participate in mercy, justice, and witness in Jesus’ name. That calling warrants financial stewardship that can be examined with clarity and independence. When Christian development ministries publish audited financials, they are making a quiet but important confession: the resources of the church are holy trusts, and those who handle them should be willing to be held to account.