What tax receipts Christian ministries should provide is not a minor administrative detail. For Christian donors, the receipt is one of the few standardized documents that tests whether a ministry treats stewardship with the seriousness Scripture demands.

The Apostle Paul’s approach to financial administration in the collection for Jerusalem was not casual: “We want to avoid any criticism of the way we administer this liberal gift” (2 Corinthians 8:20). The impulse is not self-protection alone. It is a moral commitment to handle God’s people’s gifts in a way that is verifiable, orderly, and above reproach.

Why tax receipts are a discipleship issue, not only a tax issue

Most donors think of a receipt as paperwork for April. But a ministry’s receipting practice often reveals its posture toward truthfulness, donor care, and internal controls. A prompt, accurate receipt is a small signal that the organization can be trusted with larger responsibilities.

Receipts also matter because the tax system is one of the few external constraints that forces clarity. The IRS requires specific donor substantiation for charitable contributions, and ministries that treat those requirements lightly invite confusion for donors and risk for the organization.

Stewardship requires more than good intentions

Christian donors commonly give in response to urgent need: disaster relief, children at risk, pastors in crisis contexts, Bible translation, or long-term community development. Those causes are worthy. Yet urgency can tempt ministries to treat administration as a distraction from “real ministry.” Paul rejects that division. Good administration is part of moral integrity.

What this means in practice is that donors should expect ministries to issue receipts that meet legal standards, but also to communicate with a tone that honors the sacred trust involved in receiving gifts offered unto the Lord.

Receipts are one of the simplest verifiable signals donors can test

Across our verification work at Most Trusted, we observe that ministries that meet The Most Trusted Standard tend to have disciplined, consistent donor documentation. They do not treat receipting as an afterthought delegated without oversight. They treat it as part of financial integrity and transparency.

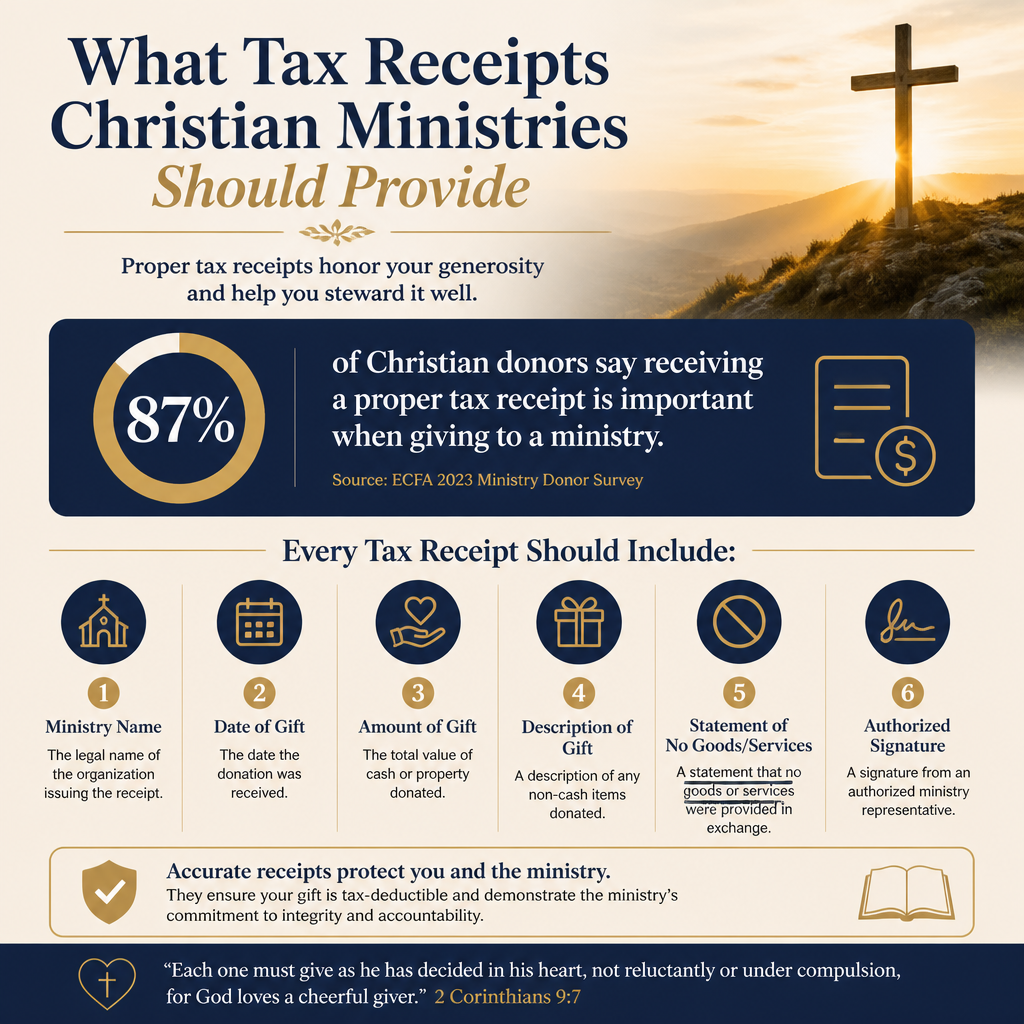

What a compliant donation receipt should include for cash gifts

For ordinary cash gifts, the baseline expectation is straightforward: the receipt should be accurate, complete, and clear about what was received and whether anything was provided in return. In IRS terms, “cash” includes checks, credit card donations, and electronic funds transfers, not only bills and coins.

Core elements donors should expect to see

A ministry receipt for a cash contribution typically includes the donor’s name, the date of the contribution, the amount given, and the ministry’s legal name. Donors should also expect a statement addressing whether any goods or services were provided in exchange for the gift.

- The organization’s legal name (and often EIN)

- The donor’s name

- Date of the contribution

- Amount of cash contributed

- A statement that no goods or services were provided in exchange for the contribution, if applicable

The IRS describes the donor’s substantiation requirements for charitable contributions, including what donors must retain and what written acknowledgments must contain for larger gifts. Donors and ministries alike should work from the same public standard rather than informal convention. See the IRS guidance on substantiation and written acknowledgments at IRS.

What changes for gifts of 250 dollars or more

Once a single contribution of 250 dollars or more is made, the donor must obtain a “contemporaneous written acknowledgment” from the charity to claim a deduction. Ministries should not make donors guess whether their email confirmation qualifies. The acknowledgment should be clear, durable, and timely.

Donors should also watch for overly vague language. A receipt that simply says “thank you for your support” without addressing quid pro quo is not careful. The standard language is not onerous, but it does need to be explicit.

Quid pro quo gifts, events, and donor benefits

The harder question is what happens when a donor receives something of value in return for a gift. Banquets, conferences, membership benefits, books, premiums, and other tangible benefits introduce a legal and ethical requirement: the ministry must help the donor distinguish the deductible portion from the value received.

Why this matters for Christian ministries

Many ministries host fundraising dinners or sell mission trip opportunities that blend a charitable purpose with tangible benefits. Christians genuinely disagree about some of the instincts that drive these models, but the tax principle is not ambiguous. Donors can generally deduct only the amount that exceeds the fair market value of what they received, and the ministry is expected to disclose that value in its acknowledgment where required.

The IRS explains the “quid pro quo” disclosure obligation and related rules for charitable organizations. Ministries planning events should align their receipting language with that standard. See IRS.

Practical examples donors recognize

If a donor gives 500 dollars to attend a fundraising banquet and the meal is valued at 60 dollars, the deductible portion is generally 440 dollars, and the receipt should state that. If a donor receives a book, a mug, or other premium with more than token value, the receipt should address the item and the value assigned. Precision here is not legalism; it is honesty.

Where ministries stumble is in treating everything as “donation” language, even when the transaction is partly a purchase. Donors should expect more careful accounting, especially from organizations that ask supporters to fund complex programs across multiple countries and compliance environments.

Noncash gifts, restricted gifts, and the limits of what a receipt can say

Some of the most generous Christian giving is noncash: stocks, cryptocurrency, vehicles, real estate, in-kind goods, and significant equipment gifts. These contributions require more careful documentation, and donors should not expect ministries to do what the law assigns to the donor.

Noncash gifts and valuation

For noncash gifts, the ministry generally should acknowledge what was received and the date, but it should not assign a dollar value for most property gifts. That valuation is typically the donor’s responsibility, sometimes supported by a qualified appraisal depending on the gift type and amount. A ministry that casually “values” donated goods on a receipt may be well-intentioned, but it can create problems for the donor’s substantiation.

The IRS provides guidance for noncash charitable contributions and the substantiation framework donors must follow, including forms and appraisal expectations. See IRS.

Restricted gifts and designated giving

Christian donors often want to designate gifts: a particular country program, clean water, Bible translation, trauma counseling, or a specific disaster response. Ministries can honor donor intent while still preserving the organization’s legal discretion to apply funds to the stated purpose. Receipts should not make promises the ministry cannot keep.

In practice, donors should be cautious of receipts or confirmations that read like a contract guaranteeing a specific individual beneficiary, especially in relief and development contexts where circumstances change. Wise ministries describe the intended use while maintaining appropriate discretion and compliance.

Donors seeking to compare ministries’ practices across this field will often find it helpful to review Christian Relief and Development Ministries, where transparency and documentation patterns vary significantly by size, geography, and operating model.

Red flags donors should treat seriously and what strong ministries do instead

Receipt problems are not always evidence of wrongdoing. Understaffed teams, outdated systems, and rapid growth can create real operational strain. Yet donors are not obligated to normalize weak practices, especially when ministries are handling sacred gifts at scale.

Common receipting failures that deserve follow-up

Several patterns show up repeatedly when donors forward receipts to our team for review or ask how to interpret an acknowledgment. The concern is not that every imperfect receipt indicates fraud, but that repeated sloppiness often correlates with deeper weaknesses in internal control and transparency.

Examples of red flags include receipts that omit quid pro quo language when benefits were provided, inconsistent donor names and amounts, missing dates, or a refusal to provide written acknowledgments for larger gifts. Another concern is a receipt that implies deductibility for something that is not a charitable contribution, such as payments for personal services or goods.

What good looks like under The Most Trusted Standard

Ministries that operate with mature integrity tend to issue receipts promptly, correct errors quickly, and provide a clear pathway for donors to request documentation. They also align their public communications with their receipting reality. If a ministry says it values transparency, the donor should see it in the small things.

We also recommend that donors look for ministries that are clear about how restricted gifts are handled, that maintain accessible financial reporting, and that treat donor questions as part of stewardship rather than suspicion. Many of these expectations overlap with broader donor decision-making in Giving Strategies for Christian Relief and Development, where administrative maturity is often the difference between confidence and chronic uncertainty.

FAQs for What tax receipts Christian ministries should provide

Is an email confirmation enough for my donation receipt?

An email can qualify if it functions as a contemporaneous written acknowledgment and includes the required elements, especially the statement about whether goods or services were provided in exchange for the gift. For contributions of 250 dollars or more, donors should ensure the acknowledgment is clear, retained, and complete under IRS substantiation rules. When in doubt, donors should request a formal receipt or year-end statement that contains the required language.

Should a ministry put a dollar value on my donated clothing, vehicle, or stock?

For most noncash gifts, the ministry should describe what was received and the date, but it generally should not assign a dollar value. Valuation is ordinarily the donor’s responsibility and may require additional substantiation, including a qualified appraisal in some cases. Donors should use IRS guidance for noncash contributions and consult a qualified tax professional when the gift is significant or complex.

Giving with clarity honors the giver, the ministry, and the Lord

Tax receipts will never be the deepest measure of a ministry’s faithfulness, but they are a meaningful measure of its seriousness. Christian donors do not ask for meticulous documentation because they distrust the Church. We ask for it because love of neighbor includes love of truth, and because stewardship requires that gifts offered to God are handled with verifiable care.

A ministry that issues clear, compliant receipts is not merely meeting a bureaucratic expectation. It is bearing witness, in a small and concrete way, to the integrity the gospel requires.