Are Christian medical ministry donations tax-deductible? Often they are, but only when the gift is made to a qualifying organization and structured as a true charitable contribution rather than a payment for personal benefit. For donors who give as an act of worship and stewardship, the question is not merely technical. It is a question of integrity before God and neighbor, since Scripture treats honest dealing with money as a matter of righteousness, not administrative preference (Proverbs 11:1; 2 Corinthians 8:21).

In practice, medical missions, Christian hospitals, pregnancy centers, disability ministries, and global health efforts operate under a range of legal structures. Some are churches. Many are recognized by the IRS as 501(c)(3) public charities. Others are membership-based cost-sharing arrangements or ministry programs housed inside broader organizations. That complexity is manageable, but it requires donors to ask the right questions before expecting a tax deduction.

Tax-deductible usually means a gift to a qualified 501c3

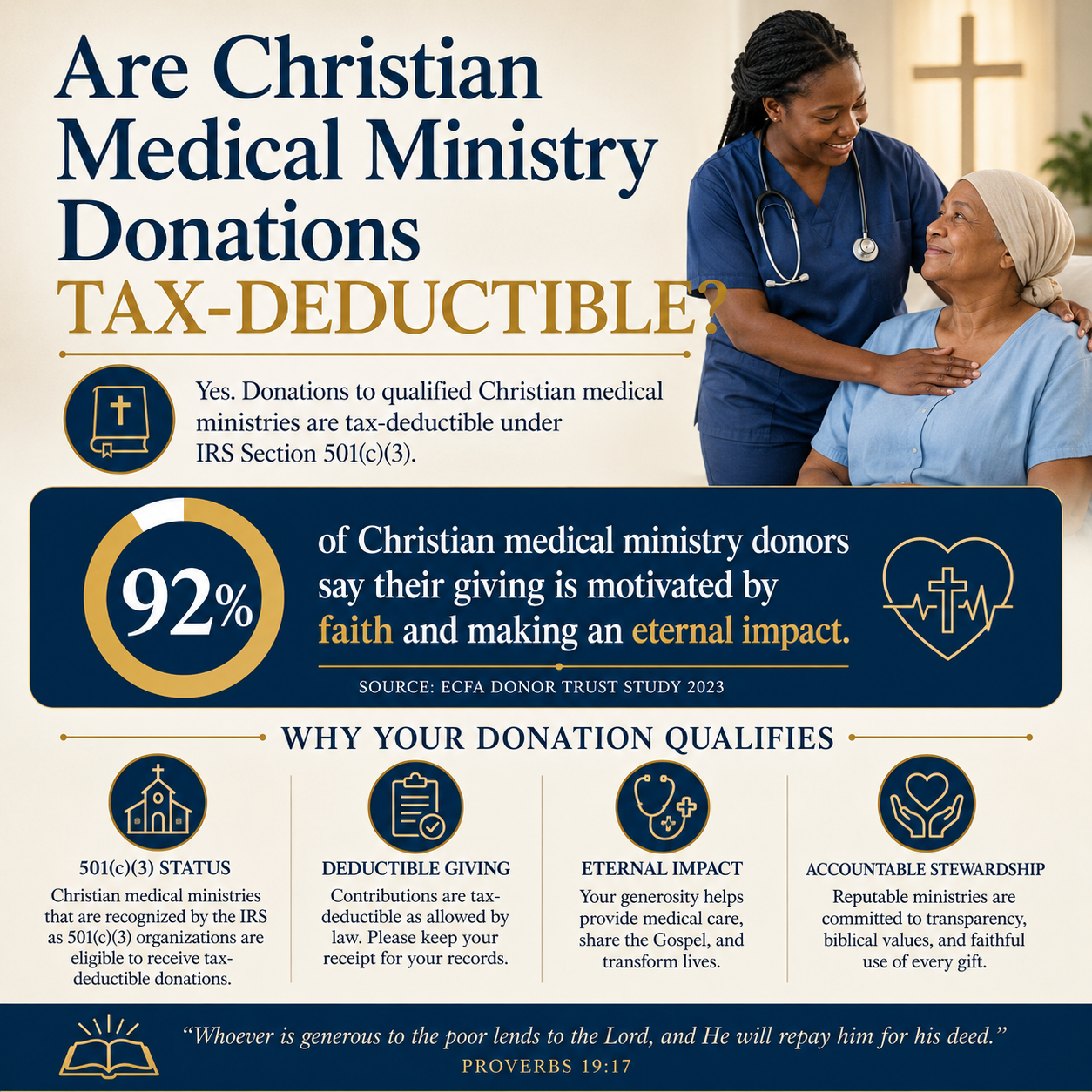

For U.S. federal income tax purposes, donations are generally deductible only when made to a “qualified organization,” most commonly a 501(c)(3) public charity. The IRS maintains the controlling definitions and rules; donors should begin with the IRS guidance on charitable contribution deductions and qualified organizations (IRS).

Many Christian medical ministries do qualify. A gospel-centered clinic serving uninsured patients, a mission hospital network, or a nonprofit funding cataract surgeries can all be valid charitable recipients. The deduction, however, attaches to the recipient organization and the nature of the transfer, not to the Christian intent of the donor. The tax code recognizes certain structures; it does not adjudicate spiritual sincerity.

How to confirm an organization’s status

A credible ministry should be able to state clearly whether contributions are tax-deductible and under what conditions. Donors can independently verify U.S. federal tax-exempt status using the IRS Tax Exempt Organization Search (IRS). If a ministry hesitates to provide its legal name, EIN, or documentation, that is not a minor inconvenience; it is a warning sign.

Churches and integrated auxiliaries

Some Christian medical initiatives operate under a church or denomination. Churches are generally treated as qualified organizations even without applying for formal 501(c)(3) determination, though donors still need substantiation for significant gifts. In these settings, clarity matters: donors should confirm whether the contribution is received by the church itself and whether the church is exercising genuine control and discretion over how the funds are used. Without that control, what looks like “giving through a church” can become a pass-through arrangement that undermines deductibility.

The harder question is quid pro quo and personal benefit

Most donor confusion arises when funds are connected to a benefit received by the donor or a designated individual. The IRS draws a bright line: a payment is not a charitable contribution if it is made in exchange for goods or services, or if it earmarks funds for a specific individual in a way that the charity does not control. The doctrine is often discussed as “quid pro quo” contributions and the “no earmarking” principle; the IRS explains the basic framework in its guidance on charitable contributions (IRS Publication 526).

This is especially relevant in Christian medical ministry because so much giving is compassionate and personal. Donors want to cover a surgery, pay for medicines, or support a family in crisis. Those desires are honorable. Yet the tax question turns on whether the nonprofit receives the gift as its own and allocates it according to an established charitable program, rather than functioning as a conduit for a donor’s private decision.

Designated giving versus earmarked giving

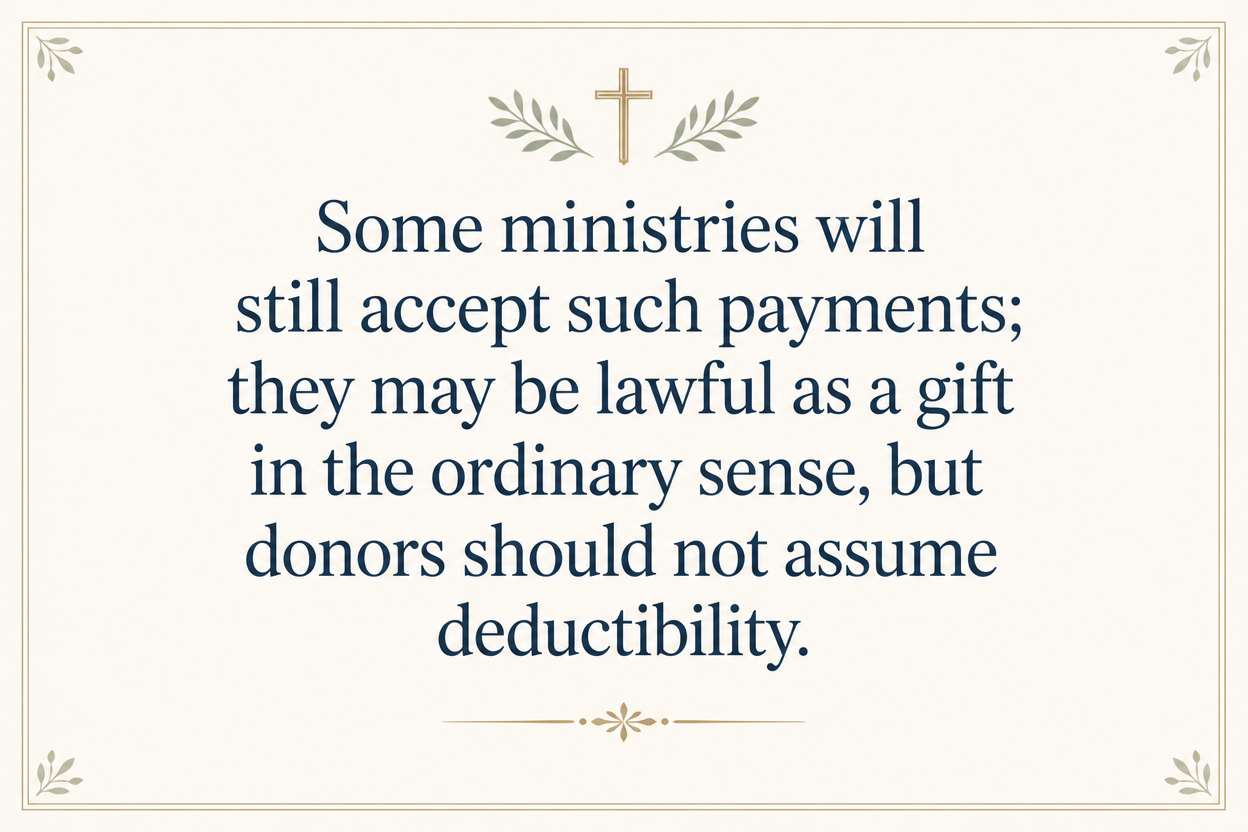

Many ministries allow donors to express a preference: “support maternal health,” “fund HIV care,” or “equip a rural clinic.” That kind of designation can remain deductible if the charity retains final control and discretion. By contrast, “this gift must pay for John Smith’s hospital bill” is generally not a charitable contribution, because it provides a direct private benefit and removes the charity’s discretion. Some ministries will still accept such payments; they may be lawful as a gift in the ordinary sense, but donors should not assume deductibility.

Membership models and cost sharing require special care

Several faith-based healthcare arrangements describe themselves as “ministries” yet function as membership contributions toward participants’ medical expenses. These can be spiritually serious communities of mutual aid, but the tax treatment can differ sharply from standard charitable gifts. When payments are made with the expectation of personal coverage, they may be treated more like insurance premiums or personal expenses than charitable contributions. Donors should ask directly: is this a donation to a 501(c)(3) public charity, or a member payment connected to one’s own medical needs?

Receipts, substantiation, and the discipline of good records

Christian donors often approach tax matters with reluctance, as though recordkeeping were at odds with generosity. Scripture does not treat careful administration as spiritual compromise. Paul insisted on transparent handling of gifts “so that no one should blame us” (2 Corinthians 8:20–21). The modern analogue is substantiation: donors should keep records that match IRS requirements and should expect the charity to issue a proper acknowledgment when needed.

What a compliant receipt should include

For a cash contribution, donors generally need a bank record or a written communication from the charity. For larger gifts, donors need a contemporaneous written acknowledgment from the charity stating whether any goods or services were provided in exchange for the gift. Those requirements are summarized by the IRS in its charitable contribution guidance (IRS).

We recommend confirming these receipt practices before year-end, especially for donors who give through donor-advised funds, make non-cash gifts, or support international medical work through U.S. intermediaries. Receipts should reflect legal reality, not donor preference.

When the receipt itself can be misleading

Some ministries issue acknowledgments that imply deductibility even when payments are connected to a personal benefit or are directed to an individual. A receipt is not an IRS ruling. Donors remain responsible for taking only lawful deductions. Ministries that take compliance seriously will communicate limits clearly and will avoid language that pressures donors toward improper deductions.

How ministry structure affects deductibility in Christian medical work

Christian medical ministry spans domestic care, international missions, and disaster response. The same act of generosity can be deductible or not depending on the structure. Donors who want to give with confidence should understand three common patterns.

Direct gifts to a U.S. public charity

This is the simplest case: a donation to a recognized 501(c)(3) that operates clinics, trains health workers, or funds care for the poor. Deductibility is typically straightforward when the donor receives no significant goods or services in return and the charity controls the funds.

International work through a U.S. intermediary

Many Christian donors support hospitals and mission clinics outside the United States. A gift can still be deductible when it is made to a qualified U.S. charity that exercises real oversight and discretion over the use of funds, even if the charity ultimately grants to a foreign partner. Donors should not assume that “international” is the problem; the real issue is whether the U.S. charity is more than a pass-through.

Pass-through and agency concerns

Some arrangements are effectively personal fundraising: a donor gives “to the ministry” but directs the funds to a particular missionary, clinician, or family. Ministries sometimes facilitate this for practical reasons. Yet the closer a contribution looks like a directed payment for a specific person’s benefit, the more fragile deductibility becomes. Mature ministries separate personal support from charitable relief and maintain documented policies that reflect that separation.

Across our verification work at Most Trusted, we observe that ministries that meet The Most Trusted Standard tend to treat compliance not as a nuisance but as part of public faithfulness. That includes clear donor communications, documented gift acceptance policies, conflict-of-interest safeguards, and financial controls that prevent donors or staff from informally steering restricted funds. Donors who want a broader view of how medical ministries operate can see the range of work and structures under Christian Medical Ministries.

What we recommend donors ask before claiming a deduction

Tax rules cannot substitute for spiritual discernment, but they can clarify what is being claimed. We recommend asking questions that test both legal status and operational integrity. For donors, this is not suspicion; it is due diligence consistent with loving the neighbor who depends on the ministry’s credibility.

- Is the recipient a qualified organization, and can it be verified in the IRS database?

- Is the payment a voluntary gift, or is it connected to a personal benefit or expected coverage?

- Does the ministry retain control and discretion over designated gifts, with written policies to prove it?

- Will the ministry provide a compliant written acknowledgment stating whether goods or services were provided?

- If funds support an individual, is the aid distributed through an established charitable program rather than donor direction?

- If the work is overseas, does the U.S. charity provide oversight and documentation rather than acting as a conduit?

Questions like these belong within a broader posture of careful stewardship. Many donors also need practical guidance on receipts, acknowledgments, and restricted gifts across different ministry contexts; Tax Receipts and Compliance for Christian Medical Ministry Giving addresses those recurring issues in more detail.

FAQs for Are Christian medical ministry donations tax-deductible

If a Christian medical ministry says gifts are tax-deductible, can we rely on that?

We can treat the ministry’s statement as a starting point, not a final determination. Donors should independently verify tax-exempt status using the IRS database and should evaluate whether the payment is a true charitable contribution rather than a payment tied to personal benefit. A receipt or website statement does not override IRS rules or the substance of the transaction.

Can we deduct a gift that is intended to pay for a specific patient’s surgery?

Usually not if the gift is earmarked for a named individual or if the donor controls the outcome. A donation can be deductible when it supports a charity’s patient care program broadly and the charity retains full discretion in selecting recipients and applying funds. Donors who want to help a particular person may still give, but they should be prepared for the gift to be treated as non-deductible.

Giving with integrity in both charity and compliance

Christian medical ministry sits close to human vulnerability, where donors feel urgency and compassion. That is precisely where clarity matters. When gifts are made to qualified charities, structured without personal benefit, and documented with proper substantiation, tax deductibility can align with faithful stewardship. When those conditions are not met, the right course is not to force a deduction, but to give honestly, ask better questions, and support ministries whose governance and financial practices can bear public scrutiny.