Tax receipts and compliance for Christian medical ministry giving are not administrative details; they are part of faithful stewardship. When donors fund medical care for others, they are rightly attentive to whether a gift is acknowledged properly, whether the ministry handles restricted funds with integrity, and whether a year-end statement will stand up to ordinary IRS expectations. The goal is not suspicion. It is clarity, so that generosity can be offered with a clear conscience and well-kept records.

Across our verification work at Most Trusted, we see that ministries with strong financial integrity and transparent donor communications tend to reduce friction for donors at precisely these points: timely acknowledgments, accurate receipting language, consistent recordkeeping, and forthright explanations when a gift cannot be treated as a charitable contribution. These practices do not replace spiritual discernment, but they do reflect it.

What makes a medical ministry gift deductible and what does not

For U.S. donors, the deductibility question usually turns on two issues: whether the recipient is a qualified charitable organization and whether the donor receives a benefit in return. The IRS frames the first issue through organizational status (commonly, but not exclusively, a 501(c)(3) public charity). Donors can verify an organization’s status through the IRS Tax Exempt Organization Search at irs.gov. In practice, reputable Christian medical ministries anticipate this concern and make their status and legal name easy to confirm.

The second issue is more pastorally charged because it touches on motive and substance: is the gift truly a gift, or is it a payment for one’s own coverage? The IRS states plainly that a charitable contribution is deductible only to the extent it exceeds the value of goods or services received in return, with specific rules for quid pro quo contributions at irs.gov. This becomes especially relevant when a donor participates in a health-sharing arrangement or gives in a way that reduces personal obligations. Christians genuinely disagree about how to describe certain arrangements in everyday speech, but tax law requires precise distinctions.

Donations, fees, and personal benefit

Many donors support Christian medical ministries in two ways at once: they contribute to a general fund that assists others, and they may also participate in a program that resembles mutual aid. The tax treatment can differ. A gift to support charitable care for others may be deductible if it meets IRS requirements. A payment that functions as a personal membership fee, premium substitute, or direct exchange for personal medical benefit may not be deductible, even if the organization is explicitly Christian and motivated by mercy.

The practical discipline for donors is to ask a simple question before year-end: “Is this transfer best described as a charitable contribution, or as a personal payment tied to my own needs?” When ministries answer this question clearly in writing, donors are protected from later confusion.

Restricted gifts and designated giving

Medical ministries frequently invite donors to support specific categories of care: maternal health, emergency relief, medical debt assistance, or international clinics. In charitable law, restrictions are legitimate when the donor sets a purpose restriction and the ministry retains discretion over the specific beneficiaries and the administration of the program. When a gift is effectively earmarked for a particular individual, however, it can become a private benefit transaction rather than a charitable contribution.

This is not merely a compliance technicality. It also guards the ministry from partiality and protects donors from the subtle temptation to convert charitable giving into an informal pipeline of personal obligation. Ministries that handle this well usually explain how designations work, what discretion the ministry retains, and how exceptions are handled when needs change.

What your receipt should contain and why the wording matters

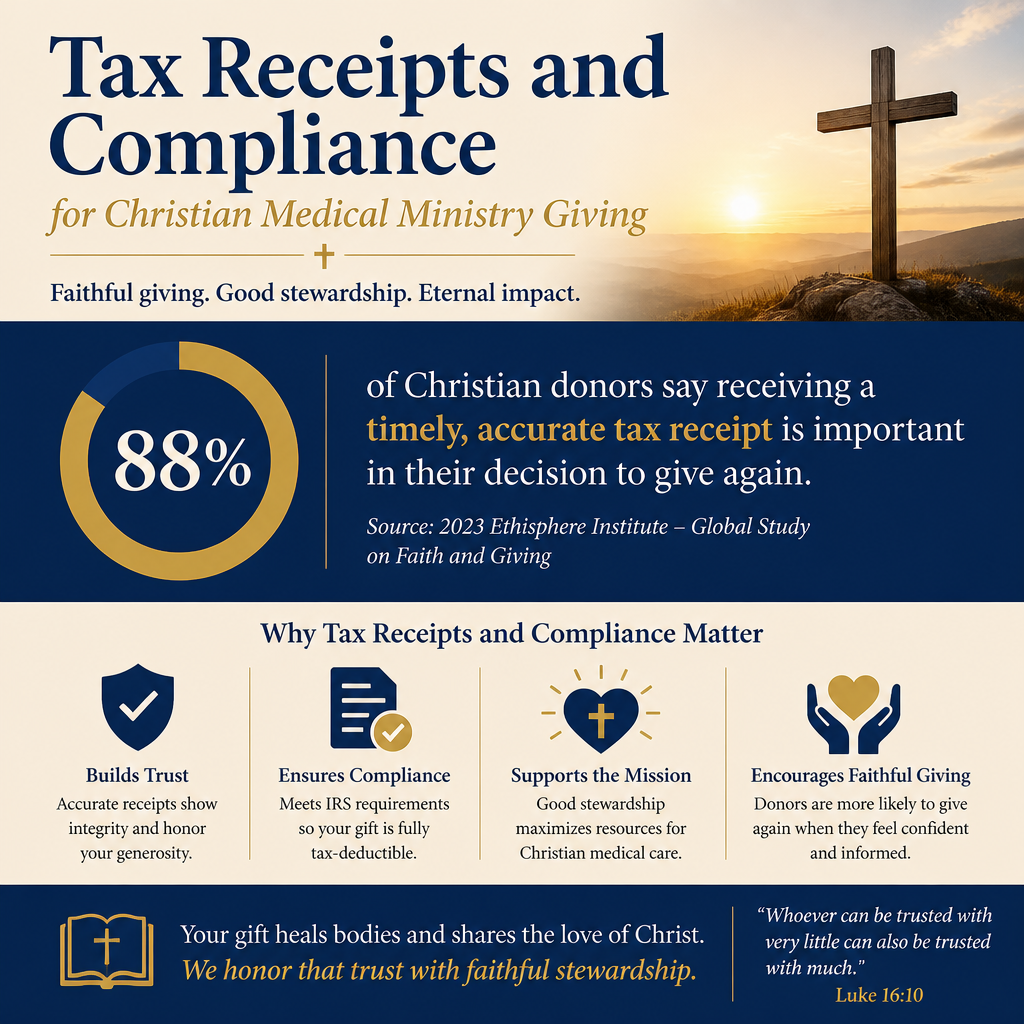

Donors often assume a receipt is a receipt. In tax practice, details matter. The IRS describes what a donor must obtain for contributions of $250 or more: a contemporaneous written acknowledgment that includes the amount contributed and a statement about whether the organization provided goods or services in exchange, with special rules for noncash gifts. The requirements are outlined at irs.gov. When donors face an audit, the existence and accuracy of these acknowledgments is commonly what the IRS will ask to see.

We encourage donors to treat receipting language as a ministry’s window into its governance and financial controls. Sloppy acknowledgments often correlate with deeper weaknesses: inconsistent donor records, unclear program accounting, and underdeveloped internal review.

Core elements for cash gifts

A strong acknowledgment for a cash donation typically includes the ministry’s legal name, the date and amount of the contribution, and a clear statement that no goods or services were provided in exchange for the contribution, or a description and good-faith estimate of the value if they were. The “no goods or services” sentence is not mere boilerplate; it is a compliance marker that the ministry understands quid pro quo rules and is willing to communicate them plainly.

When a ministry provides something of value—tickets to a banquet, a book, a membership benefit, or another tangible item—donors should expect a receipt that distinguishes the deductible and non-deductible portions. When that separation is missing, the donor bears the risk of claiming too much.

Noncash gifts and complex contributions

Gifts of stock, cryptocurrency, equipment, or in-kind medical supplies require greater care. Ministries generally acknowledge receipt of noncash property without assigning a value; valuation is typically the donor’s responsibility, with additional IRS documentation requirements at higher thresholds. If a ministry casually states a value on a noncash receipt, donors should pause and confirm that the language aligns with standard practice and current IRS expectations.

For donors making significant noncash gifts, it is prudent to coordinate early with the ministry and a qualified tax advisor, not because ministries are untrustworthy, but because the recordkeeping requirements can be exacting and deadlines can be unforgiving.

Year-end statements, matching gifts, and common failure points

Many Christian donors plan their giving in December, then rely on January statements to finalize tax records. The ministry’s timing and clarity here affects not only donor convenience, but donor confidence. When year-end statements arrive late, omit transactions, or use ambiguous descriptions, donors are left to reconstruct their own giving history under pressure.

Strong ministries treat year-end statements as a core part of donor care: accurate, complete, and delivered predictably. This is one area where competent operations quietly serve the Church.

When to expect statements and what to check

Ministries vary in their processing schedules, but donors should generally expect a year-end statement early enough to file taxes without guesswork. When it arrives, donors should check that each contribution date and amount matches bank or card records, that the ministry’s legal name is consistent, and that quid pro quo language is present where relevant. If a donor gives through a donor-advised fund, the receipt typically comes from the sponsoring organization, not the ministry itself, and the ministry’s acknowledgment should be treated as supplemental rather than primary documentation.

What this means in practice is that donors should keep both sides of the record: the ministry acknowledgment and the donor’s own payment confirmation. The IRS may accept bank records for smaller gifts, but the $250 threshold for a contemporaneous written acknowledgment is a hard line. Ministries that communicate this clearly are serving donors well.

Matching gifts and who issues which receipt

Matching gifts can create confusion because multiple parties are involved: the donor, the employer, and the ministry. In most cases, the donor’s personal gift is receipted to the donor, and the employer’s match is a separate contribution receipted to the employer. Donors should not expect to claim a deduction for the employer’s match, and they should not expect their own receipt to include the match as if it were their gift.

Some employers route matches through third-party platforms. That can introduce delays and naming variations that complicate statements. Clear ministries reconcile these gifts and communicate how they appear in donor records so that donors are not left to interpret ambiguous line items.

Common friction points that deserve direct questions

Across the sector, the most common receipting problems are not malicious. They are operational: outdated donor databases, batch processing errors, inconsistent treatment of event benefits, and confusion over whether certain payments are gifts or program fees. Mature donors should feel free to ask for clarification in writing, especially for larger contributions, noncash gifts, or any giving that is tied to participation benefits.

The harder question is whether a ministry’s systems are built for scale. A small ministry may serve faithfully for years, then grow quickly after a crisis or viral exposure. Growth tends to expose weak compliance and weak donor communication at the same time. Donors who pay attention to receipts are often the first to see those cracks.

Audits, accountability, and how Most Trusted evaluates compliance signals

Christian donors do not ask about audits because they distrust the Gospel. They ask because Scripture treats stewardship as a moral matter. Jesus’ repeated warnings about money are not reducible to personal piety; they also press on how institutions handle resources entrusted to them. “Moreover, it is required of stewards that they be found faithful” (1 Corinthians 4:2) is not a slogan. It is a standard that should be visible in policies, documentation, and candor.

In nonprofit practice, an “audit” can mean different things: an independent financial statement audit, a review, a compilation, or an agreed-upon procedures engagement. Donors should not assume every “audited” claim is equivalent. The type of engagement, the auditor’s independence, and whether the financial statements are made available all affect how meaningful the assurance really is.

What an audit can and cannot tell you

An independent audit, when properly conducted, can increase confidence that financial statements are presented fairly in accordance with an accounting framework. It does not guarantee that every program claim is accurate, that every internal control is strong, or that a ministry is effective in outcomes. It also does not replace spiritual discernment or board oversight. It is one signal among several, and it is most valuable when paired with transparency: audited statements, a clear Form 990 where applicable, and straightforward explanations of revenue sources and program spending.

For donors seeking to understand the IRS side, the IRS maintains an overview of Form 990 at irs.gov. Not every ministry files the same forms, and some religious organizations have different filing expectations, but defensiveness about basic financial transparency should raise questions for any donor tasked with stewardship.

Compliance as a component of trustworthiness

Most Trusted exists because donors deserve more than marketing assurances. Under The Most Trusted Standard, we evaluate ministries using a 15-criteria framework across Faith Foundation, Financial Integrity, Governance and Leadership, and Transparency and Effectiveness. Receipts and compliance sit within that broader landscape: they are not the whole story, but they are observable indicators of whether a ministry takes accountability seriously.

In our work, the most trustworthy ministries do not treat donor questions as nuisances. They answer them with documentation, align receipting with IRS requirements, and explain the boundaries of deductibility without resorting to ambiguity. That posture is both administratively sound and spiritually fitting.

Giving with clean records and a clear conscience

Tax receipts and compliance for Christian medical ministry giving are one of the places where mature generosity meets ordinary responsibility. Donors should expect timely acknowledgments, accurate quid pro quo language, and clear explanations when a payment is not a charitable contribution. Ministries should expect donors to ask for this clarity, not as adversaries, but as stewards.

For donors evaluating where to give and how to document it, it is wise to consider the ministry’s compliance signals alongside its theological convictions and practical care for the sick. This work sits within the wider world of Christian Medical Ministries, where compassion is urgent and accountability is a form of love.