Tax-wise giving to Christian financial service ministries is not primarily about getting the largest deduction. It is about ordering resources faithfully while honoring the legal and moral boundaries that govern charitable giving. Mature donors are right to ask how to give in ways that strengthen a ministry’s long-term capacity without confusing charity, commerce, and personal benefit.

Financial service ministries sit at a complicated intersection: they often provide counseling, training, lending, or technical services, and they sometimes charge fees. Christians genuinely disagree about where the line falls between ministry activity and market activity. What is not disputed is that donors should give with clarity about what qualifies as a charitable gift, what counts as a purchase, and how to verify that a ministry’s practices reflect the standards it proclaims.

Begin with the tax distinction that governs everything

A deductible gift is not the same as a ministry transaction

The Internal Revenue Service draws a bright line between a charitable contribution and an exchange. If a donor receives goods or services in return, the deductible portion is generally limited to the amount that exceeds the value received. The IRS describes this as the “quid pro quo” rule, and it applies whether the organization is explicitly Christian or not. The governing framework is summarized in IRS Publication 526 on charitable contributions: IRS Publication 526.

For financial service ministries, this distinction surfaces in common situations: paying for a budgeting class, purchasing a book or curriculum, paying loan origination fees, buying event tickets, or receiving one-on-one coaching. A donor may support the same ministry through both deductible giving and non-deductible purchases, but the two should not be blurred. Clear, separate transactions protect the donor, the ministry, and the credibility of Christian witness.

Some “generous” payments are simply fees

Many donors assume that if the provider is a ministry, a payment is a donation. That assumption can produce incorrect receipts and, more importantly, a distorted sense of what one has actually given. A tax receipt should state only what is true: the amount contributed, the date, and whether any goods or services were provided. Ministries that handle these matters with precision tend to be the ones that treat governance and financial integrity as discipleship issues rather than administrative burdens.

Use the giving instruments that fit serious stewardship

Donor-advised funds and bunching when it serves long-term generosity

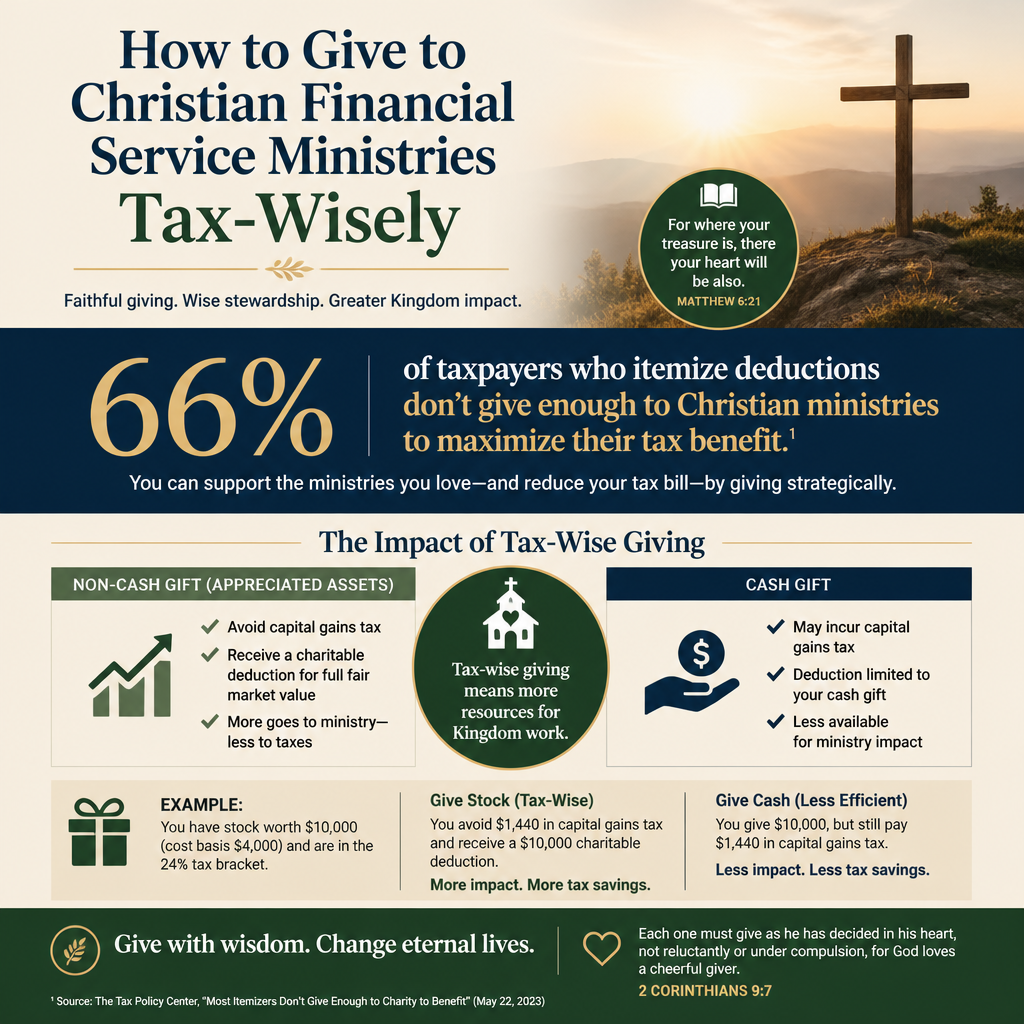

Tax-law changes have made itemizing less common for many households, which means some donors no longer receive a marginal tax benefit for charitable gifts in a given year. One lawful response is “bunching” several years of charitable giving into one year to exceed the standard deduction, often using a donor-advised fund to distribute grants over time. The IRS outlines the standard deduction and filing thresholds annually: IRS Topic 551.

This approach is not a spiritual good in itself. It is a tool. For donors with stable giving intentions, it can preserve the discipline of regular support for ministries while improving tax efficiency. For donors prone to treat giving as discretionary, it can become an excuse to turn generosity into an annual accounting project. Stewardship requires knowing which risk is more likely in one’s own household.

Appreciated assets and qualified charitable distributions

Giving appreciated securities directly to a qualified charity is often more tax-efficient than selling and giving cash, because it can avoid capital gains tax while still allowing a charitable deduction if the donor itemizes. This is especially relevant for donors whose generosity is constrained by the tax friction created by selling assets.

For donors age 70½ and older, qualified charitable distributions from an IRA can also be significant. These distributions can satisfy required minimum distributions while excluding the amount from taxable income in many cases. Because the rules are precise and penalties are real, counsel from a qualified tax professional is prudent before implementing. The IRS provides an overview of IRA charitable distributions: IRS IRA charitable distributions.

What this means in practice is that sophisticated donors can often increase net giving without increasing out-of-pocket cost. That outcome is not manipulation; it is lawful stewardship. The moral question is whether the structure serves a stable commitment to the work of the gospel or merely the satisfaction of tax minimization.

Give without subsidizing private benefit or conflicted lending

Be cautious with gifts that reduce your own costs

Financial service ministries may offer discounted services, preferential access, or member benefits. Those can be legitimate program features. They can also create private benefit concerns if donors effectively pay for their own services through “donations.” The stronger practice is separation: pay for services as a client, and give charitably as a donor, with receipts that reflect reality.

Christians often feel a pastoral impulse to “help a ministry out” by paying more than the stated fee. That can be appropriate, but only if the ministry can properly document the value of what was received and receipt the difference as the charitable portion. If a ministry cannot explain how it handles this, caution is warranted. Confusion here is not merely technical; it is an integrity issue.

Understand how loan funds and revolving capital affect deductibility

Some Christian financial service ministries operate loan funds, microenterprise programs, or revolving capital pools. Donors sometimes assume that contributing to a loan fund is always deductible. In reality, the deductibility can depend on the structure and the recipient organization’s tax status, and on whether the donor retains any rights to repayment or financial return. If the arrangement resembles an investment or includes repayment to the donor, it is typically not a charitable contribution.

Even when a gift is deductible, donors should ask how the ministry accounts for loan losses, reserves, and program outcomes. Revolving funds can be powerful, but they can also mask underperformance if leadership uses recycled principal to imply a level of impact that is not borne out by repayment rates, graduation outcomes, or client stability. Clarity about reporting is part of Christian truth-telling.

Verify the ministry, not only the tax receipt

Why tax compliance is necessary but not sufficient

A correct receipt does not guarantee a faithful ministry. Donors can do everything legally right and still fund fragile governance, unaccountable leadership, or financial practices that quietly erode trust. Across our verification work at Most Trusted, we observe that the ministries that sustain integrity over decades tend to treat financial controls, board oversight, and transparent reporting as part of their Christian formation.

That is the rationale behind The Most Trusted Standard, our 15-criteria evaluation framework covering faith commitments, financial integrity, governance and leadership, and transparency and effectiveness. We do not replace a donor’s prayerful discernment. We do insist that discernment should be informed by verifiable evidence, especially when ministries handle money, counsel families under stress, or steward capital intended for the vulnerable.

Practical due diligence questions for Christian financial service ministries

- Does the ministry clearly distinguish donations from fees, and does it issue receipts consistent with IRS rules?

- Are audited financial statements, annual reports, and board governance disclosures readily available?

- Is executive compensation disclosed and explained in context, rather than defended with vague comparisons?

- Are outcomes reported in a way that names limits and trade-offs, not only success stories?

- Does the ministry’s theology of money resist both prosperity assumptions and shame-based scarcity?

For donors comparing ministries across the space, the broader landscape of Christian Financial Service Ministries can clarify which organizations are structured as churches, charities, or hybrid entities, and which models tend to create recurring receipt and governance confusion.

Plan tax-wise giving without shrinking the moral horizon

Let the tax code serve generosity, not define it

Scripture does not treat giving as an optimization problem. Jesus’ warnings about wealth and self-justification are severe because money is morally formative. Tax planning is legitimate, but it can become a subtle discipline of self-protection if the donor’s imagination is limited to what is deductible. Christian generosity includes hospitality, direct relief, and church-based care that may not always fit the categories donors prefer.

The harder question is how a donor’s giving plan shapes the heart over time. A disciplined approach—budgeted, reviewed annually, and tied to long-term commitments—often produces more stability for ministries than sporadic gifts driven by emotion or tax deadlines. The most mature donors treat multi-year commitments as a form of truthfulness: if we say a work matters, we fund it in a way that reflects that claim.

Coordinate with counsel and keep records that withstand scrutiny

Complex giving requires competent counsel. A CPA or attorney familiar with charitable contributions can prevent unforced errors, especially around noncash gifts, IRA distributions, and gifts connected to services received. Recordkeeping also matters. The IRS requires written acknowledgments for certain contributions, and donors should retain receipts, contemporaneous acknowledgments, and valuation documentation where applicable. The IRS summarizes substantiation expectations for charitable contributions: IRS substantiation requirements.

Christian donors should not fear scrutiny; ministries should welcome it. Transparency is not a concession to secular regulators. It is an application of the biblical concern for honest weights and measures, expressed in contemporary institutional form.

FAQs for How to give to Christian financial service ministries tax-wisely

If a ministry charges for financial counseling, can we still give a deductible donation?

Yes. A donor can pay a counseling fee as a client and also make a separate charitable contribution. The key is that the donation must not function as payment for services received. If the donor receives goods or services in connection with a payment, only the amount exceeding the fair value of what was received is generally deductible under IRS quid pro quo rules described in IRS Publication 526.

Are gifts to a ministry loan fund tax-deductible?

Sometimes, but the answer depends on how the fund is structured and whether the donor receives any repayment rights or other return. If the arrangement resembles an investment or includes repayment to the donor, it is typically not a charitable contribution. Because these structures vary, donors should ask the ministry for written clarification and consult qualified tax counsel before claiming a deduction. For broader context on evaluating ministries in this field, see How to Give to Christian Financial Service Ministries.

Giving that is both lawful and faithful

Tax-wise giving to Christian financial service ministries requires more than selecting a technique. It requires honesty about what is a gift, clarity about what is a purchase, and vigilance against arrangements that quietly convert charity into private benefit. When donors pair competent tax planning with rigorous verification and a theologically grounded vision of stewardship, their giving strengthens ministries in ways that endure beyond a single tax year.