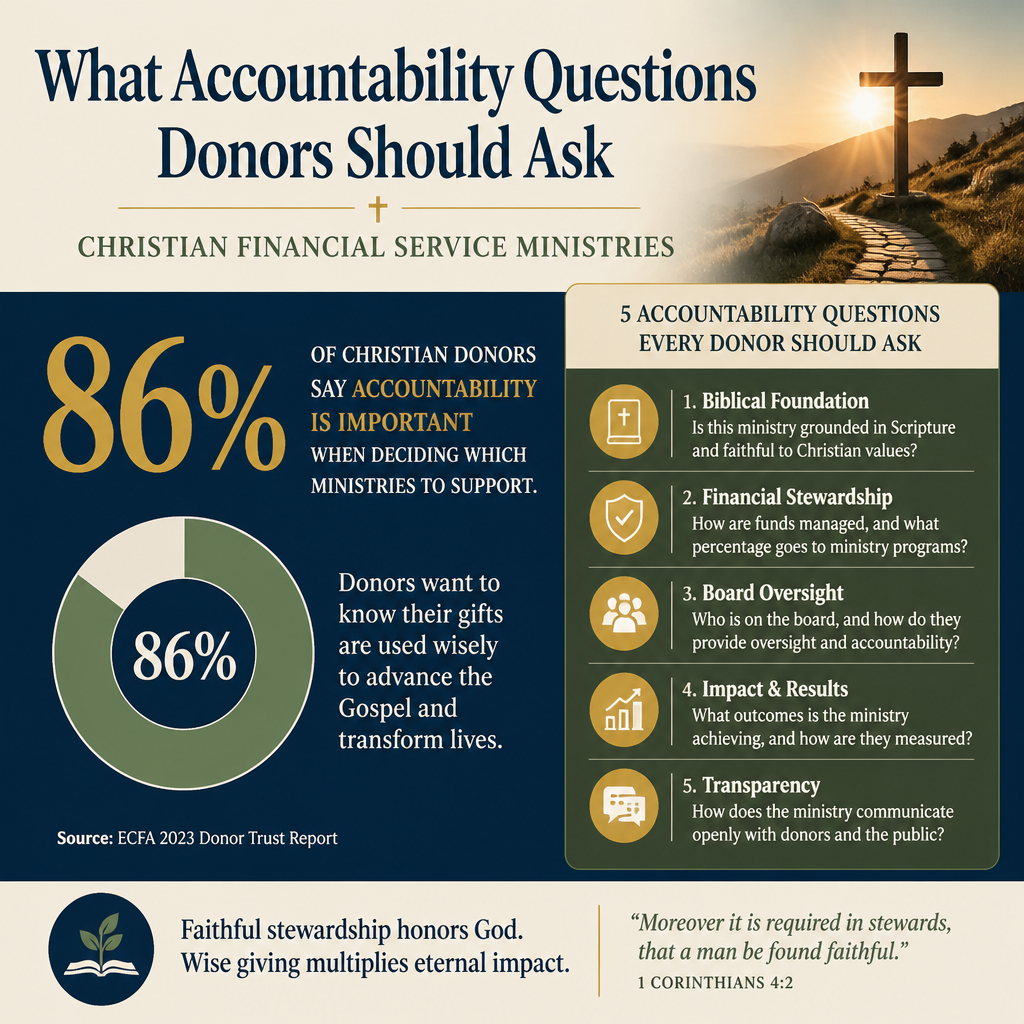

What accountability questions donors should ask Christian financial service ministries are not peripheral; they are stewardship questions with spiritual weight. When a ministry touches debt relief, lending, budgeting, or donor-advised giving, it shapes habits of the heart as well as household balance sheets.

Scripture does not treat money as neutral. Jesus warned that mammon competes for worship, and the apostles treated integrity with funds as a credibility issue for the gospel itself. Donors who want to give with a clear conscience should not settle for marketing assurances or warm testimonies. The work requires verifiable answers, documented controls, and leaders who welcome scrutiny.

1. Begin with theology and moral clarity, not product features

Ask what the ministry believes money is for

Christian financial service ministries often sound similar at the surface: “helping believers steward resources,” “breaking the cycle of debt,” “funding kingdom work.” Accountability begins by asking for a coherent Christian account of money, prosperity, and obligation. Is the ministry’s teaching anchored in a biblical theology of stewardship, generosity, contentment, and justice—or does it drift into a baptised version of consumer finance?

Christians genuinely disagree about details: whether certain debt instruments can be used responsibly, how to weigh entrepreneurship against simplicity, or how strongly to emphasize tithing language in the New Covenant. But theological seriousness is measurable. Does the ministry have a published doctrinal statement and a clearly articulated approach to wealth, interest, and mercy? Is there evidence that board and senior leadership submit to that doctrine when revenue pressures rise?

Ask how it protects the vulnerable from spiritualized financial pressure

Financial ministries serve people in stress: families behind on bills, pastors facing burnout, donors trying to be faithful amid conflicting counsel. That vulnerability can be exploited through manipulation, shame, or promises that Scripture does not make. Donors should ask whether the ministry has written standards for fundraising and counseling that forbid coercive tactics, guarantee voluntary participation, and avoid implying that giving to the ministry is a condition of God’s favor.

Across our verification work at Most Trusted, ministries that meet The Most Trusted Standard tend to show their work here: they publish what they teach, they train staff on ethical boundaries, and they maintain complaint pathways that do not route every concern back to the person who caused it.

2. Demand transparent economics and honest incentives

Ask who pays, who profits, and what is subsidized

Many Christian financial service ministries combine charitable activity with fee-based services. Some function as nonprofits offering counseling and education. Others operate programs that resemble financial products: debt management plans, lending circles, investment platforms, insurance-like member models, or DAF administration. None of those structures is automatically unfaithful. But each creates incentives that can conflict with pastoral rhetoric.

Donors should ask for a plain-language map of the ministry’s revenue streams: donations, fees, interest income, affiliate commissions, corporate sponsorships, and program reimbursements. Ask how pricing is set and whether lower-income clients pay more (directly or indirectly) than higher-income clients. Ask what portion of donations subsidizes services, what portion funds expansion, and what portion supports executive overhead.

Ask whether the ministry’s messaging aligns with its business model

A ministry may describe itself as “free help,” while funding operations through referral fees from financial products. Another may emphasize “debt freedom,” while sustaining itself through multi-year repayment plans that create retention incentives. Donors should ask whether the ministry discloses conflicts of interest, affiliate relationships, and compensation arrangements in a manner that an average donor can understand.

This is not a demand for “no overhead” or “no revenue.” The nonprofit sector has rightly pushed back on simplistic overhead ratios, as articulated in the Overhead Myth letter endorsed by GuideStar, BBB Wise Giving Alliance, and Charity Navigator https://www.guidestar.org/. The accountability question is whether the ministry’s economics are explained honestly and governed with discipline.

3. Verify financial integrity with documents, not assurances

Ask for audited financials and specific internal controls

Donors should ask whether the ministry publishes independently audited financial statements, not only an annual report summary. If an audit is not available, ask why: size, cost, or governance maturity. For ministries with significant revenue, the absence of audited statements is a substantive risk factor. When financial work includes client funds, escrow-like arrangements, or restricted gifts, internal controls are not optional.

Specific questions are appropriate: Who can initiate payments, who can approve them, and who reconciles accounts? Are dual controls used for disbursements? Are restricted gifts tracked and reported with clarity? Does the board finance committee review variance reports, cash reserves, and related-party transactions?

Ask how the ministry handles reserves and downturn risk

Christian donors have learned in recent years that reputational crises and economic volatility can disrupt funding quickly. If a ministry is promising ongoing services—especially anything that resembles a long-term financial commitment to clients—donors should ask about liquidity and risk management. What is the reserve policy? What triggers spending restraint? What is the contingency plan if donations fall sharply?

Even healthy ministries can be destabilized when revenue becomes correlated with market swings or donor sentiment. The donor’s task is not to guarantee outcomes but to ensure the ministry is not operating as if providence exempts it from prudence.

4. Evaluate governance, independence, and the real distribution of power

Ask whether the board can discipline leadership

Many ministry failures are not fundamentally financial; they are governance failures that later show up as financial or moral scandal. Donors should ask who holds authority, how decisions are reviewed, and whether the board has independent capacity to correct senior leadership.

Ask whether the board is majority independent, whether it meets without staff present at times, and whether it documents executive compensation decisions with comparability data. If the founder remains central, ask what succession planning exists and whether any “irreplaceable leader” narrative has quietly formed.

Ask about related-party transactions and family employment

Christian organizations are often relational by design, and family involvement is not automatically problematic. But related-party arrangements can create conflicts that undermine trust. Donors should ask whether the ministry has a written conflict-of-interest policy, whether disclosures are collected annually, and whether the board minutes reflect recusal and independent review when conflicts arise.

For donors wanting a deeper view of how ministries handle these questions across the field, we maintain a continuing editorial focus on Accountability and Transparency in Christian Financial Service Ministries.

5. Insist on truthfulness about outcomes and real-world harm

Ask what success looks like and how it is measured

Financial discipleship is hard to measure, and simplistic metrics can distort ministry practice. A “debt paid” number may ignore whether families built emergency savings, whether financial stress in the home decreased, or whether clients were pushed toward unwise decisions to meet program targets. Donors should ask what the ministry measures, how it defines terms, and whether it distinguishes outputs from outcomes.

Where claims are made, ask for the underlying methodology. If surveys are used, ask about response rates, sample bias, and whether results are independently reviewed. When a ministry makes public claims about the financial condition of Americans or Christians, donors should expect responsible citation. For example, the Federal Reserve’s annual Survey of Household Economics and Decisionmaking is a widely used benchmark for household financial stress https://www.federalreserve.gov/.

Ask how the ministry identifies and reduces unintended harm

Christian financial help can unintentionally reinforce shame, create dependency, or substitute technique for discipleship. The most responsible ministries acknowledge that risk. They train staff to avoid manipulating counselees, they maintain escalation paths for mental health crises, and they partner wisely with local churches rather than replacing pastoral care with a hotline.

Donors can ask a short set of questions that often reveals whether a ministry has done the difficult work:

- What complaints do you receive most often, and what did you change because of them?

- How do you protect clients from being marketed financial products they do not understand?

- What safeguards prevent spiritual pressure in counseling or fundraising?

- How do you handle data privacy, especially for sensitive financial information?

- What do you do when a client’s situation is beyond financial coaching and requires deeper care?

In the broader nonprofit field, the “starvation cycle” described by Gregory and Howard explains how pressure to appear low-cost can reduce organizational effectiveness and ultimately harm those served https://ssir.org/. Christian donors can learn from that analysis while still insisting that ministries tell the truth about what their services cost and why.

For readers who want to situate these questions within the wider ecosystem of organizations offering Christian financial products and services, we track the category at Christian Financial Service Ministries.

FAQs for What accountability questions donors should ask Christian financial service ministries

Should donors avoid Christian financial service ministries that charge fees?

Fees are not automatically disqualifying. The accountability question is whether fees are disclosed clearly, set fairly, governed responsibly, and aligned with the ministry’s stated mission. Donors should be especially attentive when the ministry’s revenue grows primarily through client retention or product referrals, because incentives can quietly shape counsel.

What is the single most revealing document to request?

Independently audited financial statements are often the most revealing starting point because they disclose revenue sources, functional expenses, cash position, restrictions, and related-party notes with more discipline than promotional materials. If a ministry cannot provide an audit, donors should ask what financial review exists, who performed it, and what timeline and governance steps are in place to mature toward independent audit oversight.

A stewardship posture that honors truth

Accountability is not suspicion; it is a disciplined commitment to truth in a domain where temptation is predictable and damage can be quiet. Donors who ask careful questions are not undermining ministry. They are insisting that Christian work involving money be as light-filled as the gospel it claims to serve, with practices sturdy enough to withstand scrutiny and seasons of pressure.