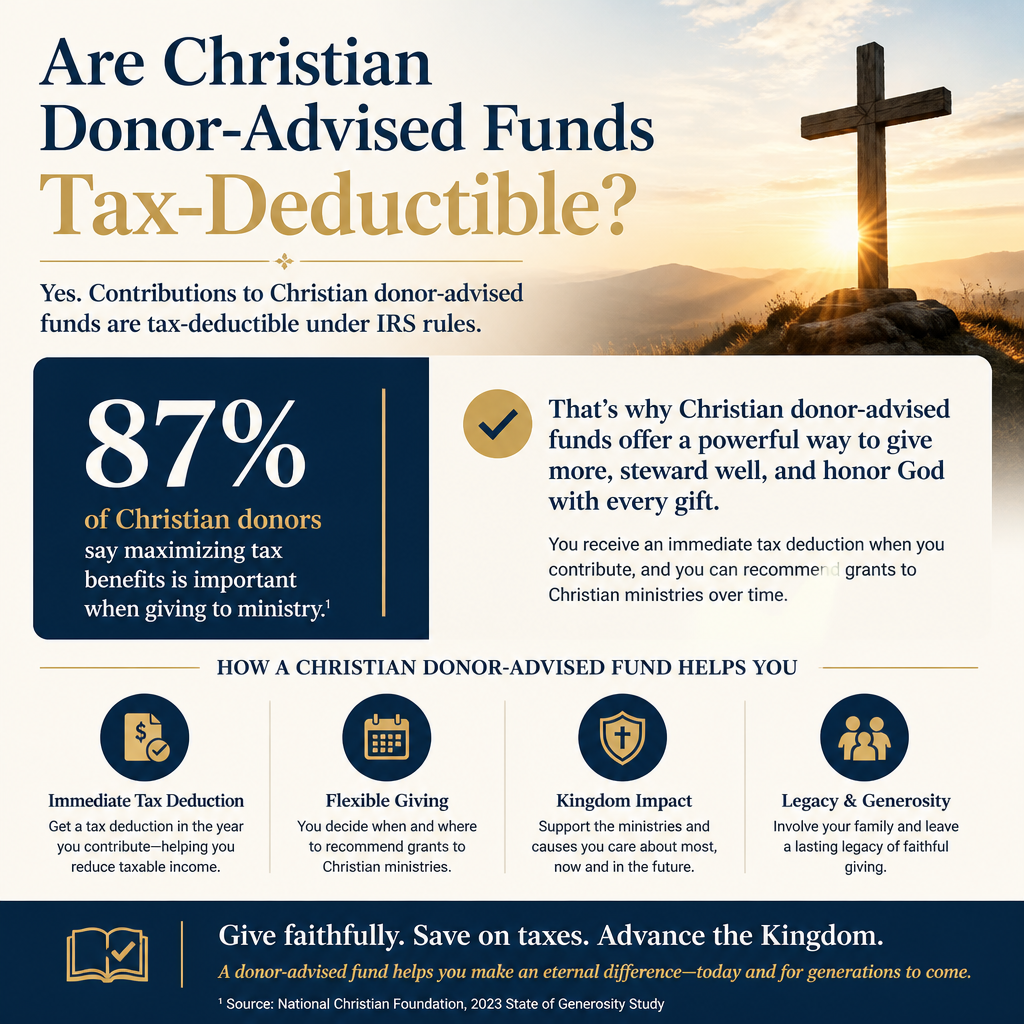

Are Christian donor-advised funds tax-deductible? In most cases, yes: contributions to a properly structured donor-advised fund are generally deductible in the year the gift is made, because the gift is made to a public charity that sponsors the fund. But faithful stewardship requires more than a tax answer. The harder questions are what, exactly, you are donating, what limits apply, how much control you retain, and whether the ministries you ultimately recommend are worthy of confidence.

Scripture never treats giving as a mere financial transaction. Jesus’ teaching assumes that money reveals allegiance and that generosity is an act of worship, not a mechanism for self-justification (Matthew 6:19–21). Tax law may encourage giving, but it cannot sanctify it. Christian donors should understand the rules clearly, then apply them with integrity.

When a Christian donor-advised fund gift is tax-deductible

The basic rule in U.S. tax law

A donor-advised fund is not a separate legal entity in the way a private foundation is. It is a charitable account maintained and operated by a sponsoring organization, typically a public charity. When you contribute to the sponsoring organization and it accepts the gift, the contribution is generally treated as a completed charitable donation for federal income tax purposes, even though you may later recommend grants from the account.

The Internal Revenue Code defines donor-advised funds and describes core restrictions, including the requirement that the sponsoring organization have legal control over the contributed assets. For the statutory definition, see Internal Revenue Service.

What makes the deduction legitimate

The deduction rests on the same principle that governs any charitable contribution: the donor must relinquish dominion and control. In a donor-advised fund, you may advise, but you do not own the assets after the gift is accepted. The sponsor may consider your recommendation, but it must retain final discretion. If a structure is marketed as a “donor-advised fund” while allowing the donor to direct distributions as a matter of right, that should raise immediate concern.

Because many Christian donors want strong faith alignment, it is common to choose a Christian sponsoring organization. That can be a prudent choice, but it does not change the legal question: the sponsor’s governance and policies must ensure that gifts are irrevocably charitable and that grants are made consistent with law and the sponsor’s charitable purposes.

Deduction limits and substantiation rules donors must treat seriously

Percentage limits depend on what you give

Even when a donor-advised fund contribution is deductible, the amount you can deduct in a given year is limited. Limits vary based on the type of property and the classification of the recipient organization. Many donor-advised fund sponsors are public charities, which often allows higher percentage limits than gifts to private foundations, but the details depend on your circumstances.

The IRS sets these limits and explains substantiation requirements for charitable contributions. For current guidance, see Internal Revenue Service.

Receipts and valuation are not administrative details

Christian donors sometimes treat recordkeeping as a bureaucratic distraction from spiritual obedience. Yet integrity is not optional when the public is subsidizing charitable giving through the tax code. Cash gifts require contemporaneous written acknowledgment at certain thresholds. Noncash gifts can trigger additional documentation and valuation requirements, and complex assets frequently require qualified appraisals.

In practice, the sharpest problems arise when donors contribute noncash assets—closely held business interests, complex real estate, or collectibles—without a clear plan for valuation, liquidation, and compliance. A reputable sponsor will be candid about what it will and will not accept and will not promise outcomes that depend on aggressive interpretations.

What you can and cannot do with a donor-advised fund as a Christian donor

You can recommend grants, but you cannot direct them

Many Christian families choose a donor-advised fund because it supports long-term, prayerful giving—especially when a family wants to involve children in decisions over time. This is often healthy. But it must be paired with humility about authority. The sponsor must retain final decision-making power, and donors should expect policies designed to protect the sponsor’s legal obligations.

For donors seeking a broader understanding of how these accounts function in Christian practice, our coverage of Christian Donor-Advised Funds addresses both the stewardship opportunity and the accountability questions that follow.

Benefits to individuals are prohibited

A donor-advised fund cannot be used to provide prohibited benefits to a donor or related parties. The most common point of confusion involves “self-satisfaction giving”—arrangements that feel generous but function as personal benefit. Paying for a gala table where the value is more than incidental, using DAF funds to buy items that you take home, or recommending grants that satisfy a personal pledge can raise serious compliance issues.

There are also restrictions and excise taxes tied to certain distributions and benefits involving donor-advised funds. The IRS is the appropriate primary reference point for the governing framework. Start with Internal Revenue Service.

Timing and intent matter for faithful tax stewardship

The deduction happens when the gift is made to the sponsor

One reason donor-advised funds are attractive is that they separate the timing of the tax deduction from the timing of grants. You can contribute in a high-income year, claim the deduction (subject to limits), and then recommend grants over subsequent months or years. That flexibility can serve thoughtful giving, but it can also tempt donors to treat the charitable account as a parking place rather than a channel of active mercy.

Many sophisticated donors ask whether a donor-advised fund is consistent with Jesus’ warnings against storing up treasure. The New Testament does not forbid prudent planning; it forbids hoarding and self-trust. Donors should examine whether the account is a tool for disciplined generosity or an excuse for delay. The moral question is not simply whether assets remain “charitable” on paper, but whether love of neighbor is being postponed without necessity.

A few practical guardrails that tend to prevent drift

- Set a grantmaking cadence that matches your household’s discernment and the urgency of need.

- Write a giving purpose statement anchored in biblical priorities, then revisit it annually.

- Keep clear separation between personal commitments and charitable recommendations.

- Use the sponsor’s due diligence tools, and add your own when grants are large or complex.

- Document your rationale for major grants, especially when funding restricted projects or overseas work.

These are not merely efficiency tips. They are disciplines of stewardship. Christian donors are accountable not only to regulators, but to the Lord who sees what is done in secret (Matthew 6:1–4).

Verification still matters after the deduction

A donor-advised fund does not evaluate ministries for you

The tax deduction answers one question: whether your contribution to the sponsoring organization is charitable under federal law. It does not answer whether the ministries you will support are doctrinally faithful, financially sound, well-governed, or candid with the public. Some donor-advised fund sponsors perform meaningful vetting. Others primarily ensure that a grantee is a recognized charity and that the grant is legally permissible. Mature Christian giving requires more.

At Most Trusted, we exist because donors routinely face a credibility gap. Marketing narratives and sincere testimonies are not the same as verifiable evidence. Our team evaluates ministries against The Most Trusted Standard, a 15-criteria framework that addresses faith commitments, financial integrity, governance and leadership, and transparency and effectiveness. The goal is not suspicion; it is confidence grounded in facts that can be tested.

Legal compliance is not the same as Christian trustworthiness

Many organizations are properly registered charities and still operate with weak internal controls, conflicted boards, opaque related-party transactions, or inflated impact claims. These failures are not merely administrative. They are moral failures because they misrepresent the use of resources entrusted for God’s purposes. Donors should treat governance and transparency as forms of truth-telling.

For donors who want a deeper orientation to the recurring legal and compliance issues around these accounts, our work on Tax and Legal Basics of Christian Donor-Advised Funds addresses where misunderstandings most often arise and what prudent donors should ask before they give.

FAQs for Are Christian donor-advised funds tax-deductible

If we open a Christian donor-advised fund, can we deduct the contribution even if we do not make grants right away?

Generally, yes. If you make a completed charitable contribution to the donor-advised fund’s sponsoring organization and it accepts the gift, the deduction is typically available for that tax year (subject to applicable limits), even if you recommend grants later. The sponsor must have legal control over the assets, and you should keep the required acknowledgments and documentation. For the IRS framework governing donor-advised funds, see Internal Revenue Service.

Are donor-advised fund contributions deductible for state income tax too?

Sometimes, but not always, and the rules vary by state. Many states generally follow federal definitions of charitable contributions, but state-specific limitations and conformity rules can change the result. Christian donors should confirm with a qualified tax professional who understands their state and the nature of the assets being contributed.

Giving with a clean conscience and clean paperwork

Christian donor-advised funds are often tax-deductible because the gift is made to a charitable sponsor and is legally irrevocable. That is a significant benefit, and it can serve long-term, wise generosity. The same structure can also obscure responsibility if donors confuse “advised” with “directed” or treat tax timing as the primary purpose.

Our counsel is straightforward: treat the tax deduction as a means, not an end. Give in a way that is compliant, transparent, and spiritually honest. Then apply equal seriousness to the ministries you fund, because the moral weight of Christian stewardship does not stop once a receipt is issued.