How Christian donor-advised funds handle grants is not merely an administrative question. For Christian donors, grantmaking is where stewardship becomes concrete: where prayerful intent meets legal structure, ministry risk, and the lived consequences of funding decisions.

Donor-advised funds can serve Christian generosity well because they pair charitable efficiency with deliberation. Yet they also introduce distance. A donor writes one check to a sponsoring organization and then recommends grants over time, often to ministries the donor has not personally observed. That distance can either protect wisdom or erode it, depending on how grants are reviewed, documented, and followed through.

Grantmaking is the moment stewardship becomes accountable

Theological weight meets institutional responsibility

Scripture presents giving as worship and as moral formation, not as a private expression of preference. Jesus commends costly faithfulness, warns against performative righteousness, and ties money to where the heart rests. For donors, that means grant recommendations are not value-neutral transactions. They are acts that can strengthen faithful work or inadvertently subsidize confusion, mismanagement, or harm.

A Christian DAF does not replace discernment; it formalizes it. The sponsoring organization is the legal donor, responsible for ensuring that grants are made for charitable purposes and consistent with applicable law. Donors retain advisory privileges, but they do not own the assets once contributed. That distinction matters when a donor feels certain about an organization that the sponsor cannot approve.

What a DAF sponsor must do before sending funds

Most DAF sponsors follow a common baseline: they verify that the recipient is eligible, that the grant is not providing more than incidental benefit to the donor, and that funds are not earmarked to individuals. Those requirements are often described in “anti-abuse” terms, but for Christian donors they also function as guardrails against a subtle temptation: using charitable structures to accomplish private ends.

Because Christian donors frequently support churches, missionaries, and crisis needs, the practical questions become specific. A DAF can often grant to a church, but cannot pay a donor’s pledge in a way that creates a personal benefit. A DAF can support missions work through a qualified charity, but cannot route a grant to an individual missionary as personal support. When these lines feel technical, they are often protecting something spiritual: integrity in giving.

How grants typically move from recommendation to disbursement

Recommendation, review, and approval

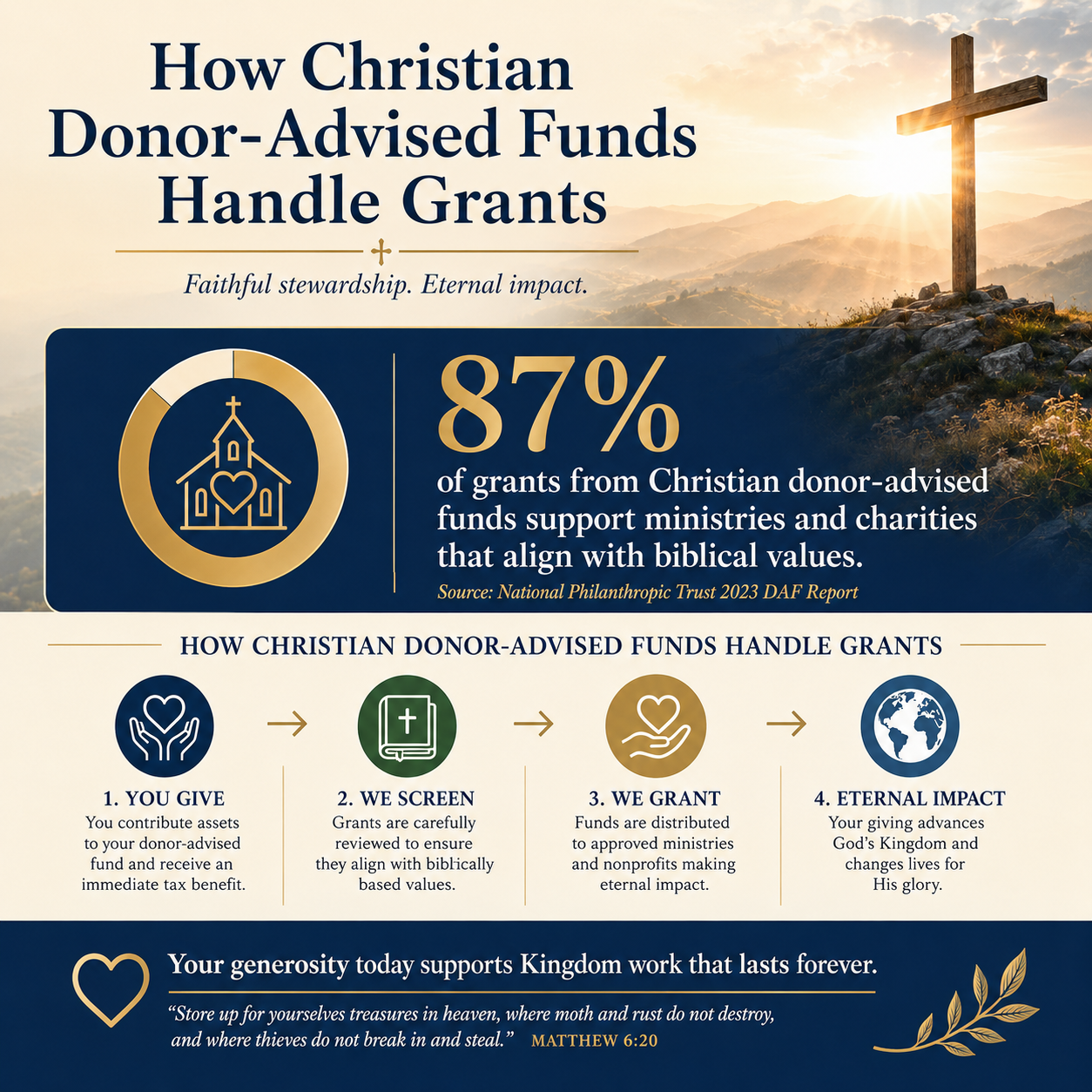

In most Christian donor-advised funds, the grant workflow has three distinct steps. First, the donor recommends a grant: recipient name, amount, and any purpose notes. Second, the sponsor reviews the recommendation for eligibility and compliance. Third, the sponsor approves and sends the grant, typically by check or electronic transfer, along with a grant letter.

Many donors assume a DAF functions like a pass-through account. It does not. The sponsor can decline a recommendation, request clarification, or require a different form of grant description. This is not hostility to donors; it is a core part of what makes the contribution to the DAF irrevocably charitable.

Timing, processing, and practical frictions

Grant timing varies widely by sponsor and by recipient readiness. Churches and smaller ministries may not have current mailing addresses on file, may not have banking information set up for electronic receipt, or may not understand how to acknowledge a DAF grant correctly. Donors who are trying to respond quickly to a disaster, a capital campaign deadline, or a year-end matching opportunity can find that the DAF introduces delay.

The trade-off is real. DAFs create order, recordkeeping, and legal clarity. They can also slow down urgent generosity. The mature approach is to plan for both: keep a posture of readiness while recognizing that certain kinds of grants require lead time.

What Christian donors should evaluate before recommending a grant

Eligibility is not the same as trustworthiness

A ministry can be legally eligible to receive charitable funds and still be unworthy of Christian confidence. Eligibility tends to focus on tax status and basic compliance. Trustworthiness includes doctrine, governance, financial integrity, and honesty about results. This is where donors must resist the assumption that a sponsor’s approval equals substantive endorsement.

Across our verification work at Most Trusted, we observe that donors often rely on familiar signals—charismatic leadership, moving stories, impressive growth—when what they actually need is verifiable evidence. The ministries that meet The Most Trusted Standard tend to have clear faith commitments, accountable leadership, transparent financial reporting, and restrained claims about impact. Those are not cosmetic virtues; they are moral ones.

Questions that protect both generosity and witness

Before recommending a grant, donors can ask questions that are both practical and spiritually serious. A short list is often enough to surface whether a ministry is operating with integrity:

- Is the recipient clearly eligible to receive charitable funds, and can the DAF sponsor verify that status?

- Does the ministry publish current financial statements or a Form 990 where applicable, and are they coherent?

- Is governance real, with a functioning board and documented oversight, rather than honorary names?

- Does leadership communicate impact with evidence and humility, not with inflated certainty?

- Are restrictions on the grant purpose clear, lawful, and aligned with the ministry’s stated mission?

This kind of due diligence is not cynicism. It is neighbor-love applied to systems. When donors fund weak governance or opaque finances, they can unintentionally burden the very people a ministry claims to serve.

Restrictions, designations, and the hard lines DAFs must hold

Purpose restrictions can be faithful and still require care

Christian donors often want to designate a grant: “for discipleship,” “for Bibles,” “for pastoral training,” “for a specific campus,” or “for a missions trip.” Many of these restrictions are appropriate and can improve accountability. Others can accidentally become earmarking—attempting to direct funds to a specific individual or to satisfy a personal obligation.

DAF sponsors are right to treat earmarking cautiously. The donor’s advisory privilege cannot become a mechanism to control charitable funds as if they remained personal assets. The sponsor must retain discretion and ensure the charity can use the funds consistently with its exempt purposes.

Why some common Christian grant ideas are declined

Some declined recommendations surprise donors because they feel morally compelling. But the DAF sponsor is operating under rules that cannot be softened by good intentions. Common examples include grants that would pay tuition for a specific student, cover the donor’s event ticket, purchase goods that will be returned to the donor, or provide direct support to a named individual. The IRS has been explicit that DAF grants cannot provide more than incidental benefit to the donor or related persons; IRS guidance on donor-advised funds and prohibited benefits explains the boundaries with clarity on how private benefit concerns arise for DAF grants. https://www.irs.gov/charities-non-profits/donor-advised-funds

The Christian instinct to meet a specific need is good. The prudent adjustment is to give through eligible structures that can meet the need without creating private benefit. For instance, many donors support scholarship funds administered by a qualified charity with an independent selection process, rather than attempting to fund a specific student. The point is not to dampen compassion; it is to preserve integrity.

Follow-through after the grant is sent

Acknowledgments, receipts, and what they do and do not mean

After a DAF grant is disbursed, the receiving ministry will typically send an acknowledgment letter. Donors should understand what that letter represents. The tax deduction generally occurs when the donor contributes to the DAF, not when the DAF makes a grant, so the donor does not need a charitable receipt for the grant itself. Still, acknowledgment matters as a practice of transparency and respect.

DAF sponsors also maintain grant records and statements that become part of a donor’s long-term giving history. For donors supporting multiple ministries over many years, this record can be a form of stewardship clarity—helpful not only for planning, but also for family communication and legacy giving.

Measuring faithfulness without reducing ministry to metrics

Christians genuinely disagree about the role of measurement in ministry. Some work is inherently difficult to quantify: pastoral care, church planting, and discipleship formation rarely fit cleanly into dashboards. Yet the absence of perfect metrics is not a license for unaccountable storytelling.

The strongest ministries tend to hold two commitments together: theological faithfulness and operational honesty. They report what they can, name what they cannot, and avoid manipulating donors with certainty they have not earned. This posture aligns with the broader charitable sector’s push for responsible transparency, including the widely cited “Overhead Myth” letter urging donors to assess nonprofits by outcomes and governance rather than overhead ratios alone. https://www.philanthropy.com/article/the-overhead-myth/

For donors who want to go deeper into the broader mechanics and trade-offs of these accounts, we maintain editorial coverage on Christian Donor-Advised Funds and on How Christian Donor-Advised Funds Work in a way that keeps legal realities and Christian stewardship concerns in view.

FAQs for How Christian donor-advised funds handle grants

Can a Christian donor-advised fund grant to a church?

In many cases, yes. Churches are often eligible charitable recipients even when they are not required to file Form 990. The DAF sponsor will typically verify the church’s status through internal processes or denominational documentation. Donors should expect the sponsor to retain discretion and to decline grants that would provide private benefit or that function as a payment of a personal obligation.

Can a Christian donor-advised fund support missionaries or individuals in need?

A DAF generally cannot make a grant to an individual. Support typically must go to a qualified charity that has full control and discretion over the use of funds and administers any aid according to an independent process. For missionary support, donors commonly give to a sending organization, church missions fund, or mission agency that can receive charitable grants and then deploy funds according to its governance and policies.

Grantmaking that strengthens the church and protects the donor

Christian donor-advised funds handle grants well when they treat grantmaking as a disciplined stewardship practice rather than a mechanical payout. The sponsor’s review is not a substitute for Christian discernment, but it can serve it—by holding legal lines, documenting decisions, and requiring clarity about recipients and purposes.

The calling for donors is to unite conviction with evidence. When grants are made to ministries that are faithful in doctrine, accountable in governance, and honest in reporting, the donor’s generosity becomes not only a gift, but a witness of integrity.