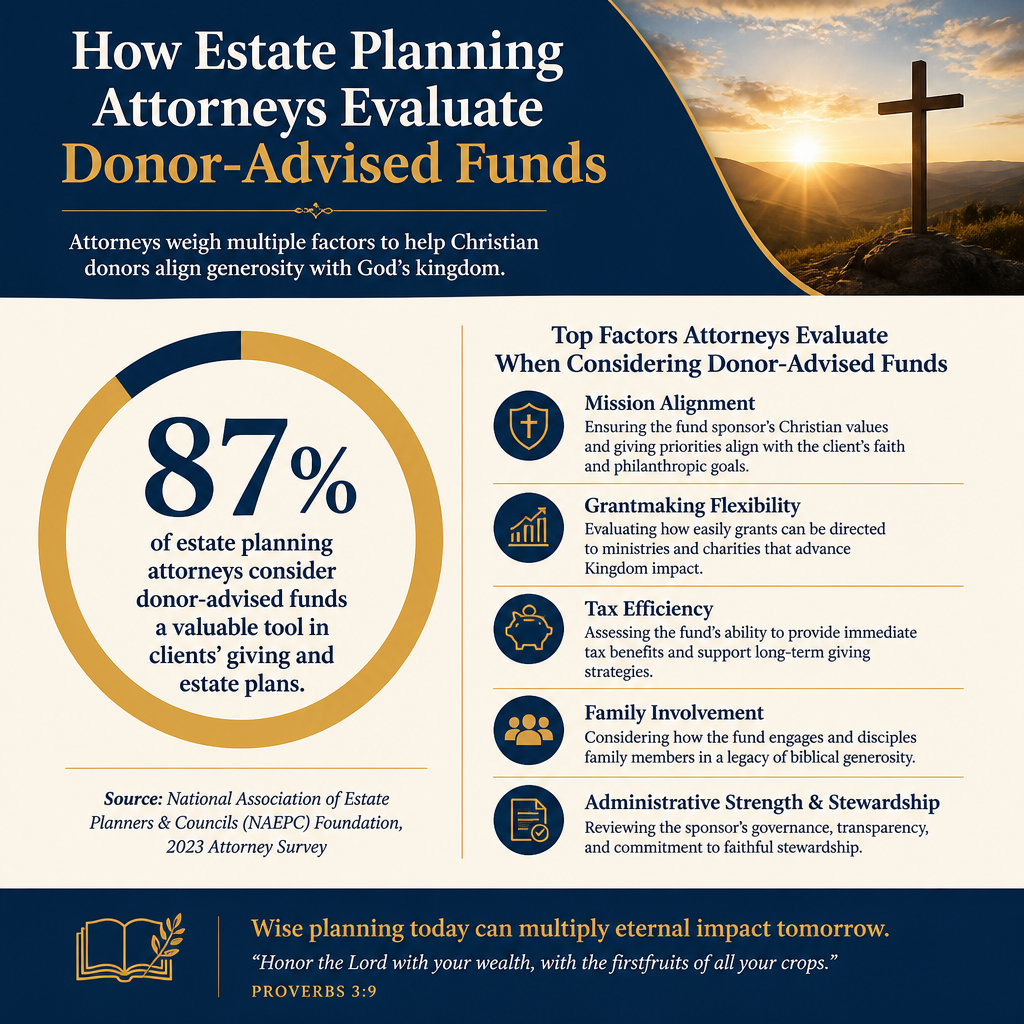

How estate planning attorneys evaluate donor-advised funds is rarely a question about convenience. It is a question about control, tax substantiation, family dynamics, and whether a client’s charitable intent will actually be carried out when they are no longer able to supervise it.

For Christian donors, the question carries additional moral weight. Scripture treats wealth as a trust, not an entitlement, and it warns against confusion between good intentions and faithful outcomes (Luke 12:48). Attorneys who work in this space often sound less like marketers and more like risk managers: they assess what a donor-advised fund can accomplish, what it cannot, and where it can unintentionally create conflict or ambiguity.

Attorneys begin with the legal identity and the limits of donor control

A donor-advised fund is legally owned by the sponsoring organization

The first step in an attorney’s evaluation is clarifying what a donor-advised fund actually is under U.S. law. When assets are contributed to a DAF, the assets become the property of the sponsoring organization, and the donor retains advisory privileges rather than enforceable control. That distinction is not a technicality; it is the defining feature that shapes both the benefits and the constraints.

DAFs are governed by rules set out in the Pension Protection Act of 2006, which formalized key definitions and restrictions, including what counts as a donor-advised fund and how certain benefits and distributions must be handled. Attorneys who want the primary source typically begin with the statute itself and related IRS guidance rather than sponsor marketing materials. See the U.S. Congress record of the Pension Protection Act at Congress.gov.

The harder question is enforceability after incapacity or death

Estate planning is about what happens when a person cannot speak for themselves. Attorneys examine whether a sponsor’s policies create a clear path for successor advisors, whether successor privileges can be split among children, and whether succession language can be drafted precisely enough to avoid disputes. They also look for what happens if the sponsor changes its policies later, merges, or closes the account class.

For Christian families, this often intersects with a real pastoral question: how to pursue unity without surrendering theological clarity. Donors may want to support evangelism and discipleship, while some heirs may prefer broadly “values-based” philanthropy. A DAF cannot eliminate those differences, but careful drafting can reduce the likelihood that conflict will derail the donor’s intent.

They test tax substantiation and distribution compliance under real-world scrutiny

Documentation and timing are evaluated as if an audit were possible

Attorneys tend to evaluate DAF administration with an auditor’s eye: how contributions are receipted, whether appraisals are required for complex gifts, and how grants are documented. This is especially true for non-cash assets—closely held business interests, restricted stock, real estate—where valuation and acceptance policies determine whether a donor’s plan will succeed on schedule.

For donors who want the most reliable baseline, IRS Publication 526 lays out the federal substantiation rules for charitable contributions, including the need for contemporaneous written acknowledgment in many cases. See IRS.gov.

Attorneys are attentive to prohibited benefits and private gain

DAFs can support a wide range of charitable work, but they cannot be used to confer more-than-incidental benefits back to the donor, the donor’s family, or related parties. Attorneys check whether the sponsor has clear procedures that prevent grants that would violate the rules—such as payments that satisfy a legally binding pledge, provide tickets or table benefits, or otherwise produce a personal benefit.

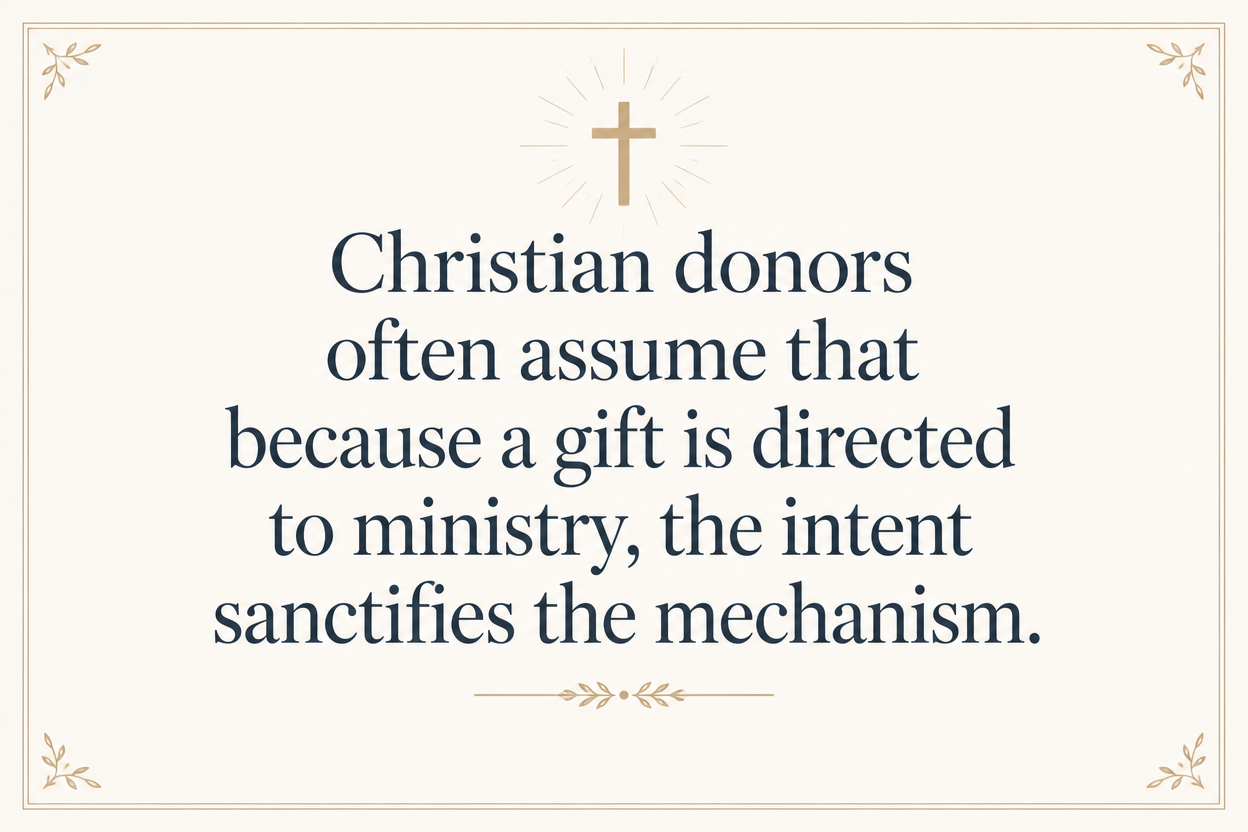

Christian donors often assume that because a gift is directed to ministry, the intent sanctifies the mechanism. The law does not work that way, and neither does Christian moral reasoning. Faithful stewardship includes careful attention to integrity and to the appearance of impropriety (2 Corinthians 8:20–21).

They compare DAFs to private foundations for legacy and family formation

DAFs reduce administrative burden but narrow formal governance

Attorneys typically frame DAFs and private foundations as different tools for different problems. A DAF usually reduces administrative complexity—no separate tax filings by the donor, fewer governance requirements, and often easier grantmaking. A private foundation can provide more formal family governance and greater control, but it comes with greater compliance burden and a higher likelihood that the structure becomes its own project.

For donors who want family involvement but do not want to create an institution that competes with the family’s vocational callings, DAFs can be an appropriate middle path. The question is whether the sponsor’s policies allow meaningful successor engagement and whether that engagement will strengthen spiritual formation rather than become an arena for rivalry.

Minimums, fees, and investment policy are evaluated as long-term stewardship issues

DAFs are not interchangeable. Attorneys review the sponsor’s fee schedule, investment options, minimum grant requirements, and policies for dormant accounts. A low fee does not automatically mean a better fit. Higher fees may accompany stronger compliance controls, better complex-asset capabilities, or more attentive grant review.

What this means in practice is that attorneys want to see whether the DAF can hold the assets a donor expects to contribute, whether it can execute the grantmaking pace the donor desires, and whether it provides enough reporting for executors and trustees to administer the estate cleanly.

They examine how the DAF interacts with the broader estate plan

Beneficiary designations and funding mechanics matter more than slogans

Attorneys tend to ask practical questions: Will the DAF be funded during life, at death, or both? Will it receive assets by beneficiary designation from an IRA or other retirement account? Will it receive a portion of the residuary estate? Each path has different implications for timing, liquidity, and family expectations.

When retirement accounts are involved, attorneys often evaluate charitable beneficiaries because of the ordinary income tax character of those assets. Many donors begin their analysis with IRS guidance on retirement account rules and distributions. See IRS.gov for foundational materials on IRAs and beneficiary considerations.

Successor advisors and statements of charitable intent are treated as risk controls

For Christian donors, the most common failure point is not the initial gift; it is the slow drift of intent across decades. Attorneys therefore look for mechanisms that can carry meaning across time: a well-drafted statement of charitable intent, guidance on theological commitments, and practical boundaries on what kinds of organizations should or should not receive grants.

Donors sometimes hesitate to write such guidance because it can feel overly directive. Yet Scripture treats legacy not as control for control’s sake, but as responsibility for what will shape future generations (Psalm 78:4–7). In estate planning, clarity is often a form of love.

They assess the quality of recipient ministries because grantmaking is the moral act

Due diligence is where Christian conscience meets verifiable evidence

Attorneys are not theologians, but they are trained to evaluate claims. Many will ask whether the donor has a repeatable due diligence process for selecting ministries. This is where Christian donors can unintentionally import weak standards: impressive stories, charismatic leaders, or emotionally compelling appeals without sufficient verification of governance, finances, and outcomes.

Across our verification work at Most Trusted, we see that mature donors increasingly want evidence that a ministry’s faith commitments are real, its finances are honest, its leadership is accountable, and its communications are transparent. That is why we evaluate organizations against The Most Trusted Standard, a 15-criteria framework that attends to faith foundation, financial integrity, governance and leadership, and transparency and effectiveness. The objective is not suspicion; it is faithful stewardship with eyes open.

Attorneys often want a simple, repeatable checklist

When a donor uses a DAF as a long-term giving platform, the diligence process has to be sustainable for successors as well. A common approach is to define a short set of questions that must be answered before recommending a grant:

- Is the organization a qualified public charity, and can the sponsor verify it?

- Does the ministry articulate a clear Christian confession, and does its work align with it?

- Are audited or reviewed financial statements available when appropriate to scale?

- Is there evidence of accountable governance, including an independent board?

- Is reporting truthful about results, costs, and limitations?

For donors who want a broader view of how donor-advised funds function in Christian giving, the category context matters. We maintain perspective on these questions within Family and Legacy Giving Through Christian Donor-Advised Funds, where the recurring issues are succession, clarity of intent, and disciplined grantmaking.

Attorneys also recognize that donors may support a range of work: local church ministry, global missions, poverty alleviation, crisis pregnancy support, prison ministry, and more. Each carries distinct due diligence questions. The DAF does not answer those questions; it simply provides the mechanism by which the questions become financially consequential.

Christian donors who want to situate these estate-planning questions within the broader practice of DAF stewardship can also engage Christian Donor-Advised Funds, where we address the interplay of generosity, accountability, and long-horizon planning.

FAQs for How estate planning attorneys evaluate donor-advised funds

Do donor-advised funds preserve our charitable intent after we die?

They can, but attorneys treat intent preservation as a drafting and policy question rather than a guarantee. The sponsor’s rules for successor advisors, the clarity of the donor’s written intent, and the family’s willingness to honor that intent all matter. A DAF typically offers less enforceable control than a private foundation, so donors who want strong guardrails should plan for clarity, succession structure, and a repeatable diligence process.

Can we use a donor-advised fund to support any Christian ministry we care about?

A DAF can recommend grants to many qualified charities, including many Christian ministries, but it cannot support non-charitable recipients, provide personal benefits, or satisfy certain obligations in ways that violate IRS rules. Attorneys evaluate the sponsor’s grant review practices, how it handles restricted gifts, and whether it has clear procedures for compliance. Christian donors also remain responsible for discerning whether the recipient ministry is trustworthy and aligned with their convictions.

Why this evaluation matters for Christian legacy giving

Estate planning attorneys evaluate donor-advised funds by asking whether the mechanism will actually serve the donor’s intent under pressure: audits, family conflict, incapacity, market volatility, and ministry controversy. That is a sobering set of tests, but it is also a gift. It forces Christian donors to treat giving as stewardship before God, not merely as preference.

A DAF can be a prudent instrument for generosity across decades, especially when paired with careful succession planning and rigorous ministry diligence. The goal is not to control the future from the grave. The goal is to order our resources toward what is true, accountable, and faithful, so that the fruit of giving does not depend on sentiment but on integrity.