What donation receipt details matter for tax purposes is not a mere administrative question. For Christian donors, it is part of honest stewardship: rendering to Caesar what is Caesar’s without allowing paperwork to become a substitute for prayerful discernment about the ministry itself.

Across our verification work at Most Trusted, we see a consistent pattern: many giving decisions are made carefully, but the supporting documentation is treated casually. That mismatch can create avoidable risk at tax time and, more importantly, can obscure whether a donor’s generosity is being handled with clarity and integrity.

Tax compliance is a stewardship issue, not a technicality

Receipts protect both donor and ministry

Christian giving is spiritual, but it is not private in the sense of being detached from public responsibilities. The New Testament commends financial integrity that is visible and accountable: “We take this course so that no one should blame us about this generous gift that is being administered by us, for we aim at what is honorable not only in the Lord’s sight but also in the sight of man” (2 Corinthians 8:20–21). A sound receipt is one small way a ministry “aims at what is honorable” in the sight of others.

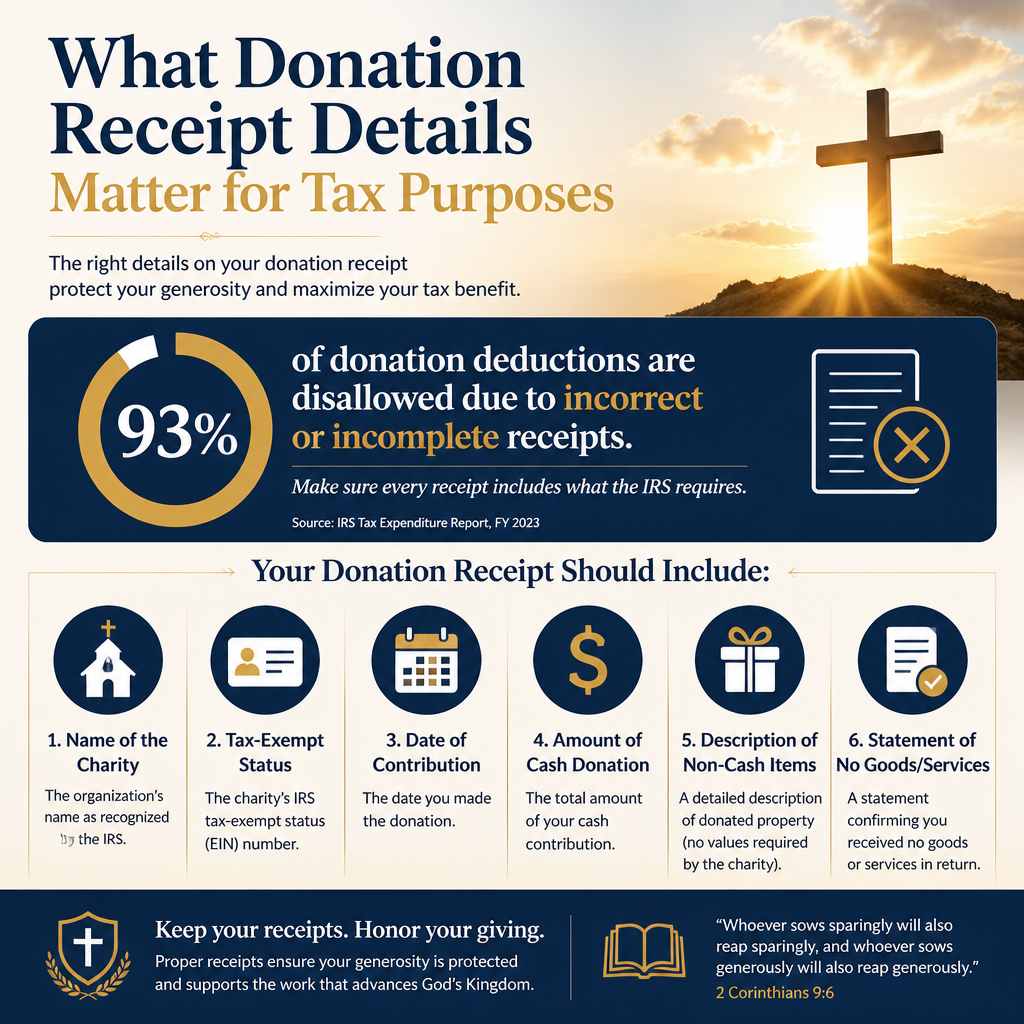

The Internal Revenue Service is explicit about what constitutes adequate substantiation, and it is not flexible in the way many donors assume. For gifts of $250 or more, a donor must have a contemporaneous written acknowledgment from the charity to claim the deduction. That requirement is not a preference; it is a condition of deductibility. See IRS guidance on “Charitable Contributions” and “Contemporaneous written acknowledgement” at IRS.gov.

Contested terrain: gratitude language versus legal language

Many ministries want receipts to sound pastoral: warm, grateful, and personal. That instinct is understandable, especially in Christian aviation ministries where donors often feel personally invested in the mission. Yet tax substantiation requires specific phrases and omissions. A receipt can be spiritually grateful and legally precise, but it must not drift into ambiguous language that suggests the donor received a benefit or that the ministry is promising a particular outcome.

The nonnegotiable receipt details the IRS expects

Core elements for cash and noncash gifts

For gifts of $250 or more, an acknowledgment should include the donor’s name, the amount of cash contributed or a description of noncash property, the date of the contribution, and one of two clear statements: either that no goods or services were provided in exchange for the contribution, or a good-faith estimate of the value of goods or services provided. The IRS describes these requirements in its charitable giving substantiation rules at IRS Publication 1771.

Two points routinely cause trouble. First, if a ministry provides anything of material value in exchange for a donation, the acknowledgment needs to address quid pro quo. Second, “contemporaneous” means the donor must receive the acknowledgment by the earlier of the date the donor files the return or the due date for filing, including extensions. The timing definition is spelled out in IRS Publication 1771 at IRS Publication 1771.

What churches and ministries sometimes misunderstand

Christian donors sometimes hear, “The donor is responsible, not the ministry.” That is only partially true. The donor bears the burden of proof, but the ministry’s acknowledgment is often the linchpin of that proof. When a ministry’s receipting is inconsistent, vague, or late, donors are left exposed.

In our view, strong receipting is a meaningful proxy for organizational maturity. It does not prove a ministry is effective, but weak receipts often correlate with weak internal controls elsewhere, especially in smaller organizations that are growing rapidly.

Quid pro quo and benefits: where donors most often lose deductions

When a gift is not purely a gift

A donation is deductible only to the extent it exceeds the fair market value of goods or services the donor receives. This applies to banquets, fundraising flights, premium items, membership benefits, or event tickets. The receipt must state the value of the benefit, or at least provide a good-faith estimate, and clearly indicate the deductible portion. The IRS summarizes this “quid pro quo” rule and the required disclosure at IRS.gov.

This matters in aviation-related fundraising because experiential events can be compelling. A donor might give at an airshow fundraiser, a hangar banquet, or a “flight experience” fundraiser connected to a ministry’s story. Those are legitimate tools, but they create a mixed transaction that must be documented accurately.

Intangible religious benefits and careful wording

Some benefits are intangible religious benefits, which do not require valuation the way tangible benefits do. Even so, ministries must use careful wording. Sloppy acknowledgments can create confusion about whether a benefit was received, and ambiguity tends to disadvantage the donor in an audit.

- Acceptable clarity: “No goods or services were provided in exchange for this contribution.”

- Quid pro quo clarity: “You received dinner with an estimated fair market value of $35. The deductible portion is $165.”

- Avoid: “Thank you for your generous gift for your flight,” if the donor actually received a flight experience.

- Avoid: Promising that a particular gift “will” fund a specific flight, unless the ministry truly treats it as a restricted gift and can honor that restriction.

Noncash gifts and stock: aviation donors should be especially attentive

Property receipts should describe, not value

Many mature donors give appreciated stock, equipment, or other noncash property. In those cases, the acknowledgment generally should describe the donated property but should not assign a value. Valuation is typically the donor’s responsibility and, for larger noncash contributions, the donor may need a qualified appraisal and IRS Form 8283. The IRS outlines these rules and thresholds in its noncash contribution guidance at IRS Topic No. 506.

In Christian aviation contexts, donors sometimes consider gifts of aircraft-related items, tools, avionics, or even parts inventories. The tax treatment can become complex quickly, especially if the donor has used the property in a trade or business, or if there are questions about fair market value and related use. A ministry should not attempt to provide valuation; it should document receipt and description with precision.

Stocks and donor-advised funds require the right records

For publicly traded stock, donors should keep brokerage confirmations and the ministry’s acknowledgment describing the shares transferred and the date received. For donor-advised fund grants, the donor is not the one making the charitable contribution for tax purposes; the sponsoring organization is. Donors can still track these gifts for personal stewardship, but they should not expect a charitable deduction from the grant itself if they already received the deduction when funding the donor-advised fund. IRS charitable substantiation guidance remains the baseline reference point at IRS.gov.

When donors are comparing ministries, the documentation burden can become one more variable in an already complex decision. This is one reason we encourage donors to evaluate Christian aviation ministries within the broader ecosystem of Christian Aviation Ministries, where questions of mission, doctrine, governance, and financial integrity intersect.

What strong receipting signals about a ministry’s trustworthiness

Receipts are a window into controls and transparency

A receipt cannot tell you whether a flight carried the right cargo, whether indigenous partnerships are healthy, or whether aviation assets are deployed strategically. Yet it can reveal whether a ministry treats donor communication as accountable recordkeeping rather than marketing. Ministries that meet The Most Trusted Standard tend to treat receipting as part of their overall transparency posture: timely, consistent, and aligned with their audited financial practices.

The harder question is how donors should respond when receipts are weak. Some donors assume it is merely a small-team limitation and compensate by lowering expectations. Others treat it as a warning sign and disengage. The right response depends on the ministry’s overall governance and financial maturity, but donors should not ignore the issue. If a ministry cannot reliably acknowledge gifts, it is fair to ask what else is not being tracked reliably.

Practical steps donors can take without becoming adversarial

Donors do not serve ministries by being cynical, but neither do they serve ministries by refusing to ask for what is basic. When giving to aviation ministries, we recommend a posture of calm clarity:

- Request the receipt promptly for any gift you expect to deduct, especially gifts of $250 or more.

- Confirm the receipt includes the required “no goods or services” statement, or a benefit valuation if applicable.

- For noncash gifts, confirm the receipt describes the property without assigning a value.

- Keep supporting records beyond the receipt: bank records for cash gifts, brokerage statements for stock.

- If you receive an event benefit, ensure the receipt specifies the fair market value and deductible portion.

These steps belong to wise giving, not suspicious giving. They align with the Christian conviction that integrity is not only inward sincerity but outward truthfulness.

Donors who want to develop a broader discipline of discernment will find that receipting questions naturally connect to bigger questions about financial accountability and transparency. That is why we situate this topic within How to Give Wisely to Christian Aviation Ministries, where documentation, governance, and ministry effectiveness belong in the same conversation.

FAQs for What donation receipt details matter for tax purposes

What if a ministry emails my receipt instead of mailing it?

An emailed receipt can qualify as a contemporaneous written acknowledgment if it contains the required elements and you receive it by the IRS timing rule. Keep the email in a durable format and retain it with your tax records. The governing requirements are described in IRS Publication 1771 at IRS Publication 1771.

Do I need a receipt for every donation, even small ones?

For cash gifts under $250, the IRS generally allows a bank record or other reliable written record, but rules vary by gift type and circumstances. For gifts of $250 or more, a contemporaneous written acknowledgment from the charity is required to claim a deduction. The IRS explains these substantiation thresholds at IRS.gov.

Receipts serve clear conscience giving

Donation receipts are not the heart of Christian generosity, but they are part of the honesty that should surround it. When receipt details are precise, donors can give with a clearer conscience, ministries can operate with fewer administrative wounds, and both can focus on the work itself: faithful witness and mercy carried out in public view with integrity.