How Christian aviation ministries prevent fraud and financial misuse is not a secondary concern for serious donors; it is part of Christian stewardship itself. Aviation work combines high-value assets, remote operations, cross-border spending, and intense donor trust—all conditions that can either strengthen accountability or expose a ministry to predictable forms of abuse.

Scripture is not silent on the moral stakes. Paul’s instructions about administering the Jerusalem relief gift centered on visible financial integrity: “We take pains to do what is right, not only in the eyes of the Lord but also in the eyes of man” (2 Corinthians 8:21). In an aviation context, that principle has operational consequences: controls must be designed for life in hangars, on runways, and in field offices, not only for a headquarters finance desk.

Why aviation ministries face distinctive fraud pressures

High-value movable assets and decentralized decision-making

Aircraft, avionics, fuel, spare parts, and maintenance contracts create a concentration of value that is unusually portable and unusually technical. Many decisions are made far from the boardroom: a mechanic orders parts to meet an airworthiness deadline; a pilot authorizes fuel at a remote airstrip; a field leader approves a cash expense to keep a medical evacuation moving. These realities do not excuse weak controls, but they do mean controls must be engineered for speed, safety, and distance.

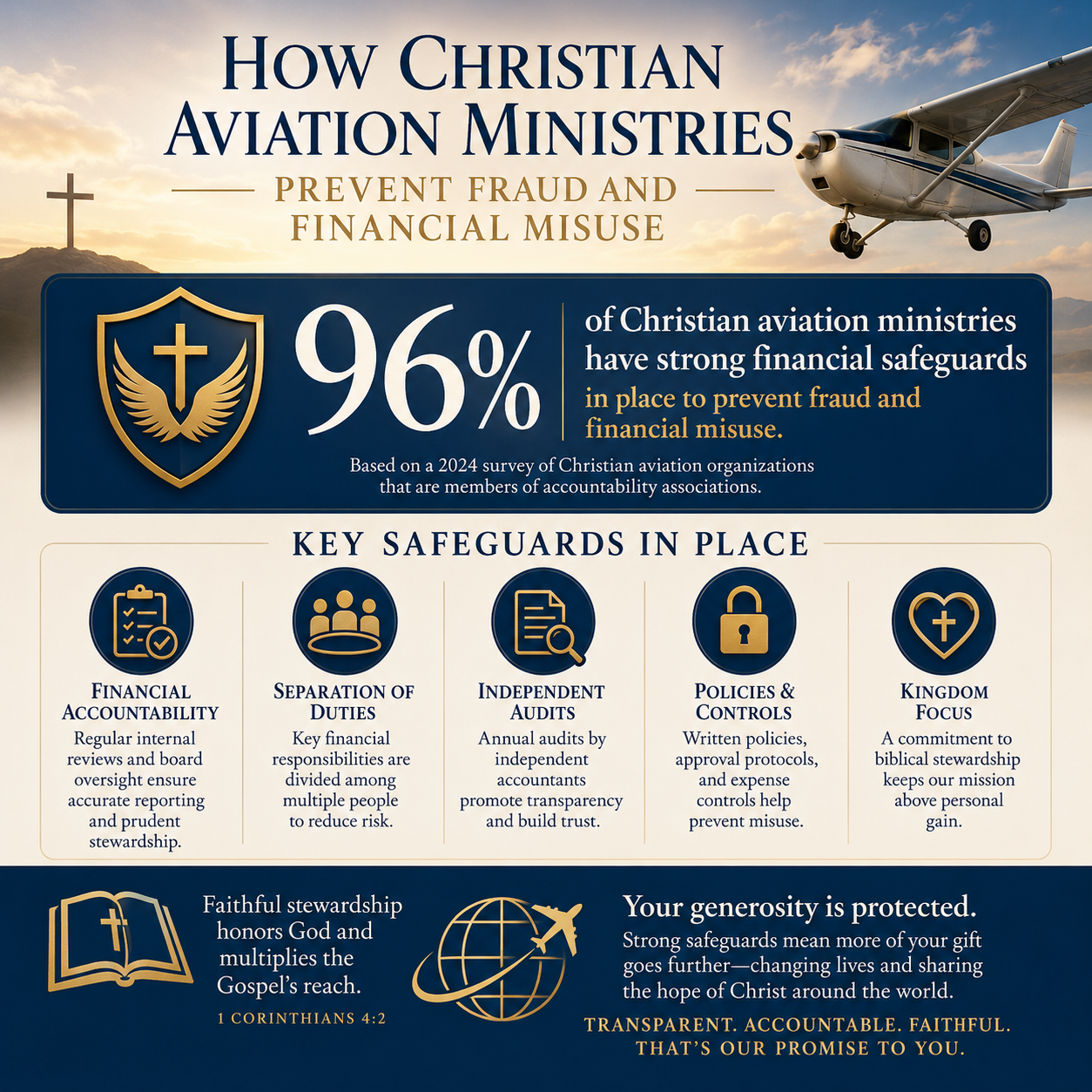

The Association of Certified Fraud Examiners consistently finds that organizations with limited segregation of duties and informal approval practices are more vulnerable to asset misappropriation and expense reimbursement fraud, especially when oversight is thin across locations. ACFE’s Occupational Fraud 2024: A Report to the Nations notes that asset misappropriation is the most common category of occupational fraud across cases studied, even when median losses are lower than other schemes; frequency matters for ministries with many small transactions across the field. Association of Certified Fraud Examiners

Cross-border giving and compliance complexity

Many Christian aviation ministries operate across jurisdictions with uneven banking infrastructure and inconsistent enforcement of anti-corruption norms. That raises legitimate operational friction: a ministry may have to pay landing fees, temporary permits, local labor, and emergency services under time pressure. The harder question is how to keep that reality from becoming a blank check for “field discretion.”

Donors should expect ministries to treat compliance as a discipleship issue rather than a nuisance: anti-bribery training, written policies for facilitation payments, vendor vetting, and documentation standards that remain non-negotiable even when the field is difficult. A mature ministry will also know that “everyone does it” is not a Christian argument.

Controls that separate trust from access to funds

Segregation of duties that works in real operations

Fraud prevention rarely begins with suspicion; it begins with design. The most resilient aviation ministries separate the authority to request, approve, pay, and reconcile. Where staffing is lean, they compensate with compensating controls: dual approvals, centralized payment release, independent review of supporting documentation, and periodic rotation of responsibilities.

Segregation of duties is particularly critical for fuel and maintenance spending because it is both high-frequency and hard for non-specialists to evaluate. A donor should not assume that “technical” spending is automatically honest; technical complexity can also become a hiding place.

Procurement discipline for parts, maintenance, and contractors

Procurement is where many ministries either demonstrate seriousness or drift into avoidable risk. Ministries that prevent misuse typically implement clear thresholds for competitive bids, documented sole-source justifications, and vendor onboarding that verifies ownership, banking details, and potential conflicts of interest. Aircraft maintenance and refurbishment projects are especially vulnerable to inflated invoices, duplicate billing, and undisclosed related-party arrangements when controls are informal.

Across our verification work at Most Trusted, the ministries that meet The Most Trusted Standard tend to treat procurement files as a form of accountability ministry, not bureaucratic overhead. They keep complete documentation, and they can explain why they chose a vendor, not only what the invoice amount was.

How strong governance shows up before a crisis

Boards that understand aviation risk and financial risk

In aviation, safety culture is not optional. Financial integrity requires a similar culture at the board level: informed oversight, not passive affirmation. A board that prevents fraud is one that receives meaningful financial reporting, asks hard questions, and has the competence to interpret answers. Some boards need aviation expertise to understand capital replacement cycles and maintenance reserves; all boards need financial competence to understand internal control risk.

Christians genuinely disagree about how “hands-on” a board should be in ministry operations. The line between governance and management is real. Yet boards cannot outsource fiduciary responsibility to a charismatic founder, a respected chief pilot, or a long-tenured CFO. In 1 Timothy 3 and Titus 1, the moral qualifications for leaders assume observable character and accountability, not private virtue alone.

Conflict-of-interest enforcement, not merely a policy

Many ministries can produce a conflict-of-interest policy; fewer can show consistent enforcement. Aviation ministries are especially exposed to related-party risks because specialized services are often provided by a small ecosystem of vendors and contractors. A conflict is not automatically corruption. It becomes corruption when it is hidden, unmanaged, or rewarded.

Donors should look for annual written disclosures from board and key staff, recusal documentation in board minutes, and procurement decisions that show independence. Ministries that treat conflicts seriously protect both the donor and the honest leader from suspicion.

Transparency that goes beyond a clean audit opinion

Audits, but also internal control maturity

An independent audit is a meaningful accountability instrument, but it is not a comprehensive fraud detector. Audits are designed to provide reasonable assurance that financial statements are free of material misstatement, not to examine every transaction or catch every abuse. Mature ministries explain this clearly rather than using an audit as a shield against legitimate donor questions.

When assessing transparency, we look for a ministry to publish financial statements or an annual report with sufficient clarity for a donor to understand revenue sources, major expense categories, and program commitments. For U.S. nonprofits, the IRS Form 990 remains one of the most standardized windows into financial governance, including board composition and related-party disclosures. Internal Revenue Service

Outcome reporting that does not incentivize exaggeration

Financial misuse is not the only integrity risk. Ministries can also misuse donor trust by overstating impact, underreporting setbacks, or presenting aviation capacity as a proxy for spiritual fruit. Aviation work lends itself to impressive numbers—hours flown, miles covered, cargo delivered. Those measures matter, but they can become a substitute for mission clarity if donors are not careful.

Responsible ministries report outcomes with appropriate restraint: what was delivered, to whom, through what partnerships, and with what limitations. They also avoid turning safety-critical decisions into fundraising stories. Transparency that is shaped by truth-telling, rather than marketing pressure, is an integrity marker.

What donors should ask for, and why it is spiritually appropriate

Practical questions that reveal the control environment

Donors sometimes hesitate to ask detailed questions because they fear appearing cynical. That instinct can be sincere, but it is incomplete. The New Testament assumes that financial administration in the church requires visible safeguards (2 Corinthians 8:20–21). Asking for clarity is not distrust; it is participation in stewardship.

The questions below do not require a donor to be an accountant or an aviation mechanic. They are designed to surface whether a ministry’s systems match the realities of aviation operations:

- Who can approve spending in the field, and what dollar thresholds require a second approval?

- How are fuel purchases authorized and reconciled against flight logs and mission schedules?

- What controls exist over aircraft parts purchasing, including competitive bids and receipt verification?

- Does the ministry have an independent audit, and does it address any material weaknesses or significant deficiencies?

- How are conflicts of interest disclosed, documented, and enforced at board and staff levels?

Using independent verification without outsourcing discernment

Independent evaluation helps donors avoid making high-stakes decisions with partial information. Most Trusted exists to serve that need by assessing ministries against The Most Trusted Standard, a 15-criteria framework that examines faith foundation, financial integrity, governance and leadership, and transparency and effectiveness. Verification is not a replacement for pastoral wisdom or personal conviction; it is a disciplined way to test whether a ministry’s claims can be corroborated.

Donors interested in the broader landscape of aviation missions can situate this question within Christian Aviation Ministries, especially where operational complexity intersects with donor responsibility. For donors comparing accountability practices across organizations, Accountability and Transparency in Christian Aviation Ministries provides the context that often determines whether a ministry’s assurances are supported by evidence.

FAQs for How Christian aviation ministries prevent fraud and financial misuse

Is a clean audit enough to assure a ministry is free from fraud?

No. A clean audit is meaningful, but it is not designed to detect every fraud scheme, particularly smaller recurring misuses spread across many transactions. Donors should also look for internal control maturity: segregation of duties, documented approvals, conflict-of-interest enforcement, and reconciliation practices tied to operational records like flight logs and fuel receipts.

What fraud risks are most common in aviation ministry operations?

Common risk areas include expense reimbursements and per diem abuse, fuel purchasing irregularities, inflated or duplicate maintenance invoices, procurement conflicts of interest, and cash handling in field locations with limited banking infrastructure. The prevention question is less about assuming bad intent and more about whether controls fit the operational realities of remote and time-sensitive work.

Stewardship that withstands scrutiny

Christian aviation ministries exist to serve the Church’s mission, often in places where access is limited and needs are acute. That urgency does not justify financial shortcuts; it increases the moral obligation to administer resources transparently and carefully. The ministries most worthy of donor confidence are those that can demonstrate, in plain documentation and disciplined governance, that their trustworthiness is not assumed but proven.