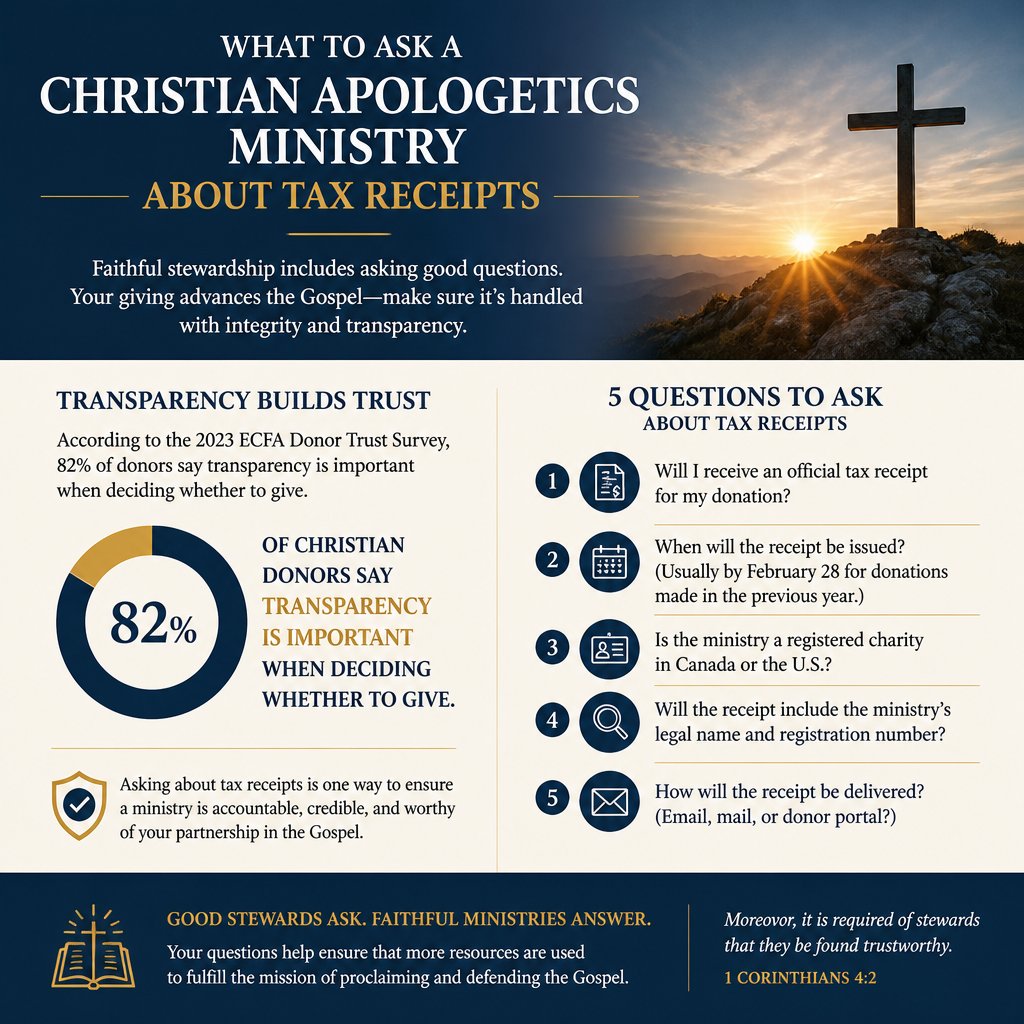

What to ask a Christian apologetics ministry about tax receipts is not a bureaucratic detour from generosity. It is one way donors test whether a ministry’s handling of money is consistent with its handling of truth—careful, verifiable, and worthy of trust.

Apologetics work often sits at the intersection of evangelism, education, publishing, events, and digital media. That mix can create legitimate complexity in what counts as a charitable contribution, what counts as a purchase, and what must be disclosed on the acknowledgment a donor receives. A responsible ministry will not treat those distinctions as nuisances. It will treat them as part of neighbor-love and honest dealing.

1. Confirm the ministry can lawfully issue receipts and acknowledgments

Ask for the organization’s legal identity and IRS status

The first question is simple: “What legal entity am we giving to, and is it eligible to receive tax-deductible charitable contributions?” In the United States, most donors are looking for a 501(c)(3) public charity. A credible ministry should be able to provide its exact legal name, EIN, and a clear statement of its status without defensiveness.

Many ministries operate affiliated entities: a church, a 501(c)(3), and sometimes a related 501(c)(4) advocacy arm. That structure can be legitimate, but it changes what kind of receipt is appropriate and whether the gift is deductible. If staff members speak as though “it’s all the same,” donors should slow down and insist on clarity.

Ask how restricted gifts are handled on the receipt and in accounting

Apologetics donors often give toward specific projects: a documentary, a campus tour, a translation, a debate series, a student scholarship for an institute, or a new curriculum. The ministry should be able to explain how it records and honors donor restrictions and what it will do if a project becomes infeasible. Mature ministries will have written gift acceptance policies that address this directly.

What this means in practice is that the receipt is only part of the question. The deeper issue is whether the ministry’s systems can actually track restricted funds, prevent internal reclassification without authorization, and report on how restricted gifts were used. Those concerns sit close to what Most Trusted evaluates under The Most Trusted Standard, because accountability is not only doctrinal; it is operational.

2. Verify the receipt contains the elements the IRS expects

Ask what the ministry provides for noncash and larger gifts

In the U.S., donors need a “contemporaneous written acknowledgment” for gifts of $250 or more. A sound ministry will not improvise here. It should issue acknowledgments promptly and ensure they include the donor’s name, the date, the amount (or a description for noncash gifts), and the required language about goods and services.

The IRS summarizes these rules in Publication 1771 and related guidance on charitable contribution substantiation; donors and ministries alike should be conversant with the basics (IRS). A ministry does not need to provide tax advice, but it does need to provide a compliant acknowledgment so a donor is not left with preventable exposure at filing time.

Ask how they handle donor-advised funds and qualified charitable distributions

Serious donors increasingly give through donor-advised funds (DAFs) and, for those age 70½ and older, through qualified charitable distributions (QCDs) from IRAs. Those channels are straightforward when staff understand them, and frustrating when they do not.

Ask: “Do you have a process for DAF grants and QCDs, and how do you document them?” A ministry should understand that a DAF receipt is generally issued by the sponsoring organization, not the ministry, and that QCDs have specific documentation expectations. When a ministry’s development staff cannot articulate the basics, it often signals broader weaknesses in financial administration.

3. Ask direct questions about quid pro quo and fair market value

When a gift is tied to something received, clarity matters

Apologetics ministries often offer books, online course access, conference registrations, membership programs, or premium media in connection with giving. Some of these arrangements are spiritually and ethically appropriate; they also raise receipt questions. The issue is quid pro quo: when a donor receives goods or services in return for a payment, the deductible portion is generally the amount that exceeds the fair market value of what was received.

Ask: “If I attend an event, receive resources, or access paid content as part of my giving, how do you calculate and disclose the deductible amount?” The right answer is not “don’t worry about it.” The right answer is a specific, consistent policy that honors both tax law and ordinary honesty.

Ask how they treat books, study materials, and digital subscriptions

Many apologetics ministries are also publishers. Others operate subscription platforms that resemble continuing education. These are fruitful tools, but they are not always charitable gifts. A donor should ask whether a transaction is a purchase, a donation, or a blended transaction with a disclosed benefit.

If a ministry distributes resources widely at no charge and a donor gives voluntarily, the receipt is simpler. If a donor must pay to receive a product, the ministry should be prepared to describe the portion that is a purchase and the portion that is a charitable contribution, if any.

- “Does this payment provide goods or services to the donor?”

- “If yes, what is the fair market value of what is provided?”

- “Is the deductible portion clearly stated on the acknowledgment?”

- “Is the same policy applied consistently across donors?”

- “Where is this policy documented in writing?”

4. Ask how the ministry handles noncash, complex, and planned gifts

Noncash gifts require precision, not improvisation

Noncash gifts are common among mature donors: publicly traded securities, closely held business interests, real estate, cryptocurrency, and collections. These gifts can be powerful for apologetics work because they free cash for mission while allowing donors to give from appreciated assets. They also require disciplined boundaries.

Ask: “If we give stock or another noncash asset, what will the receipt say?” In general, the ministry should acknowledge receipt of the asset and describe it, but not assign a value. The donor is typically responsible for valuation and may need an appraisal for certain gifts. A ministry that casually states dollar values on receipts for noncash gifts is creating risk for donors and for itself.

Planned giving calls for coordination and documentation

For donors considering bequests, beneficiary designations, or charitable remainder trusts, a ministry’s competence is tested by its documentation: clear legal name, EIN, and willingness to coordinate with advisors. The receipt question becomes: “What will you provide to substantiate gifts that occur later, through an estate or trust?”

These donors are often working within Planned Giving for Christian Apologetics Ministries commitments that involve heirs, fiduciary duty, and spiritual responsibility. A trustworthy ministry will not pressure for secrecy or speed. It will encourage independent counsel, provide written instructions, and keep lines clean between pastoral encouragement and technical claims.

5. Use receipt practices as a window into deeper governance and transparency

Ask who oversees compliance and what controls exist

Receipts are generated by systems, and systems reflect governance. Ask: “Who is responsible for ensuring receipts are accurate and timely, and what controls prevent errors?” Strong ministries typically have separation of duties, documented procedures, and periodic review—especially during year-end giving when mistakes are most common.

Also ask how promptly the ministry corrects errors. A delayed or inaccurate acknowledgment can be fixed, but a ministry’s posture matters. Defensiveness is rarely isolated to one administrative area.

Ask whether their public reporting matches their receipting practices

The donor’s question is not only “Will I get a receipt?” It is “Does the ministry tell the truth consistently—on receipts, on financial statements, and in public communications?” Responsible ministries will make it easy to access basic information: audited financials if they are large enough to warrant them, annual reports, board oversight, and clear descriptions of how funds are used.

Across our verification work at Most Trusted, ministries that meet The Most Trusted Standard tend to treat donor documentation as a spiritual discipline of transparency, not as a compliance burden. That posture aligns with a Christian account of stewardship: “Moreover, it is required of stewards that they be found faithful” (1 Corinthians 4:2).

Donors evaluating apologetics work in particular often care about intellectual integrity and public credibility. Those same values should be visible in administrative integrity. For related due diligence beyond receipting, many donors also consult Christian Apologetics Ministries as they weigh mission fit, financial practices, and governance signals.

FAQs for What to ask a Christian apologetics ministry about tax receipts

Should a Christian apologetics ministry put a dollar value on a noncash gift receipt?

Generally, no. For many noncash gifts, a ministry should acknowledge receipt and describe the property, but not state its value. Donors typically determine value for tax reporting and may need qualified appraisal documentation depending on the gift type and amount. When in doubt, donors should consult a qualified tax advisor and confirm the ministry follows IRS substantiation norms (IRS).

If I receive books or event access because I gave, is my whole gift deductible?

Not necessarily. If goods or services are provided in exchange for a payment, the deductible portion is generally limited to the amount that exceeds the fair market value of what the donor received. A trustworthy ministry will disclose that value clearly and consistently on the acknowledgment rather than leaving the donor to infer it.

Receipts are a small document with a large moral weight

A donor’s receipt is not the sum of Christian accountability, but it is an unusually clear test. Ministries that proclaim truth publicly should welcome verifiability privately: clear legal identity, compliant acknowledgments, consistent treatment of donor benefits, and disciplined handling of complex gifts. When a ministry treats receipts with seriousness, it often signals a deeper readiness to steward resources in a way that honors both the Gospel and the donor’s trust.