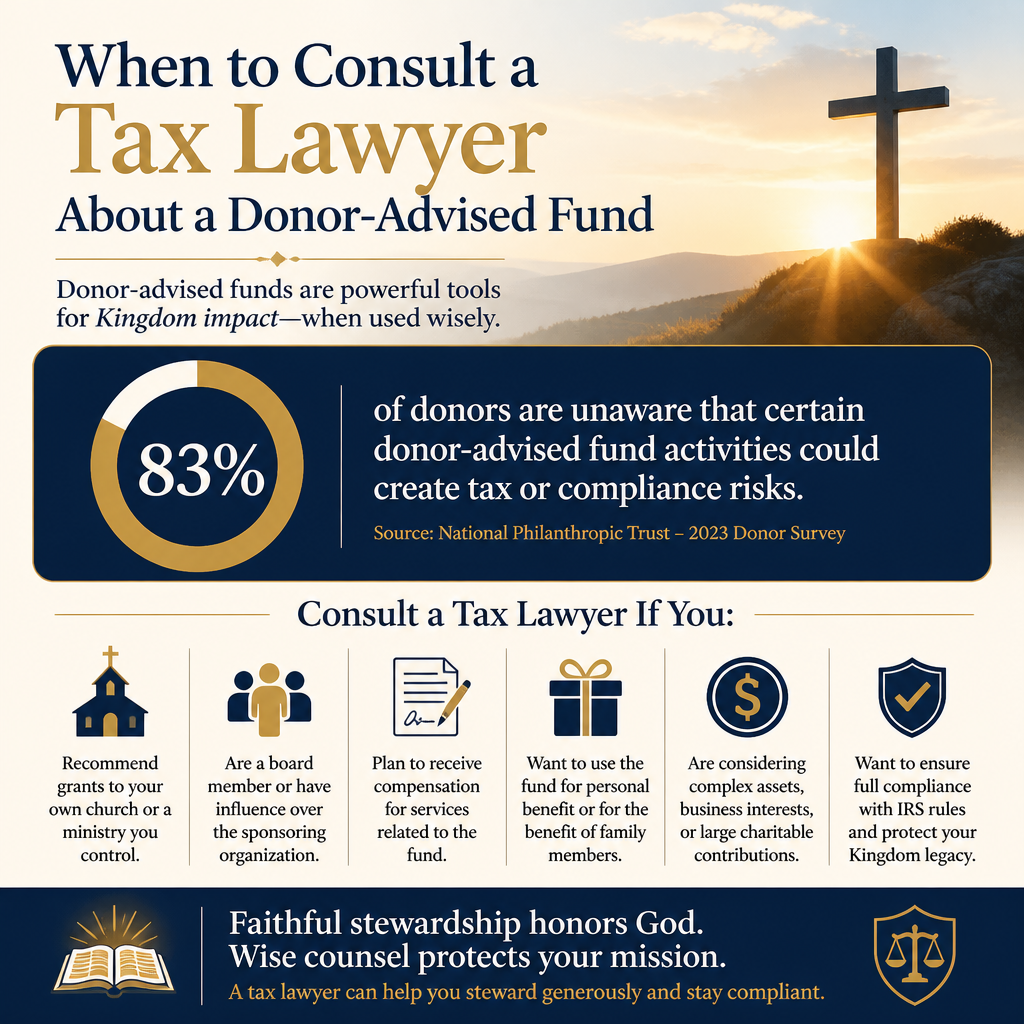

Knowing when to consult a tax lawyer about a donor-advised fund is less about anxiety and more about stewardship. A DAF can be a clean, effective instrument for generous Christian giving, but it sits at the intersection of tax law, charitable rules, and family decision-making—areas where small errors can become costly, and where serious donors often have legitimate complexity.

Most DAF activity never requires bespoke legal counsel. A reputable sponsoring organization handles administration, issues receipts, and keeps the account within standard charitable parameters. Yet certain patterns reliably signal that a qualified tax attorney should review the plan before gifts are made, grants are recommended, or family members are added to advisory roles.

Know what a DAF can do and what it cannot do

A donor-advised fund is not a private foundation and not a personal account. Legally, contributions are irrevocable gifts to a public charity that sponsors the fund, and the donor retains an advisory privilege regarding grants. Most legal trouble begins when donors treat advisory privileges as control, or when they assume a DAF can accomplish objectives that belong in other vehicles.

DAFs are charitable vehicles, not multipurpose planning tools

DAFs are designed for charitable giving, not personal benefit, not business transactions, and not family compensation. The sponsoring charity must maintain legal control over assets and grantmaking decisions, even if, in practice, it generally follows donor recommendations. When a DAF is pressured toward outcomes that look like quid pro quo, self-dealing, or private benefit, a tax lawyer’s counsel becomes prudent.

We also recommend clarity about what “qualified charity” means in practice. Many Christian ministries operate with integrity but still have uneven governance, limited disclosure, or weak financial controls. That is not a legal disqualification, but it can create reputational and stewardship risk. Most Trusted’s work focuses on helping donors evaluate ministries against The Most Trusted Standard so that generosity is paired with verifiable credibility.

DAF rules shift at the edges

The hard cases are rarely about routine grants to a church or established ministry. They appear when donors give non-cash assets, coordinate giving with a sale or liquidity event, involve family members across state lines, or attempt to solve a complicated need through a grant that looks charitable but functions like private support. Those are the places where a tax lawyer earns their fee.

Consult a tax lawyer when the gift itself is complex

Many legal issues arise before the DAF receives anything—at the point of contribution. If the asset is unusual, encumbered, or connected to a transaction, a tax attorney can help ensure the donor’s intent is carried out without creating avoidable tax exposure.

Non-cash gifts require careful documentation and timing

Publicly traded securities are straightforward. But closely held business interests, private equity, cryptocurrency, real estate, or collectibles introduce valuation questions, transfer restrictions, and compliance obligations. In some cases, the DAF sponsor may refuse the asset or require significant review. A tax lawyer can coordinate with the sponsor so the contribution is structured and documented correctly.

If a donor claims a deduction for a non-cash charitable contribution above certain thresholds, the IRS requires a qualified appraisal and specific reporting. The rules are technical, and mistakes can jeopardize the deduction. The governing IRS guidance is the starting point for the compliance framework: IRS Charitable contributions substantiation and disclosure requirements.

Gifts tied to a sale or liquidity event merit legal review

DAFs are often used to give appreciated assets before a sale, aligning generosity with tax efficiency. This can be legitimate, but it is also an area where the “assignment of income” doctrine can be implicated if the sale is already effectively locked in. If a donor is contributing business interests or property in proximity to a signed letter of intent, a binding purchase agreement, or other evidence that a sale is inevitable, counsel should review the timeline and documents.

Tax law here is fact-specific. The question is not whether a donor had a hope or expectation of sale, but whether the donor had already earned the income or effectively transferred the right to it. A tax lawyer can help a donor avoid arrangements that invite scrutiny, and can document the donor’s charitable intent in a way that holds under examination.

Consult a tax lawyer when grants could create private benefit or quid pro quo

Most DAF grants are routine and compliant. Legal risk increases when a grant recommendation is connected to the donor’s personal benefit, a family member’s benefit, or an exchange of value. This is also where Christian donors can feel tension: the desire to meet a real need can collide with rules designed to prevent charitable dollars from becoming a substitute for personal spending.

Common risk areas where counsel is often warranted

We recommend speaking with a tax lawyer before recommending DAF grants connected to any of the following:

- Payments that satisfy a legally binding pledge or other enforceable obligation of the donor

- Event tickets, gala tables, or any arrangement where the donor receives goods or services in return

- School tuition, scholarships earmarked for a specific person, or aid directed to a named individual or family

- Mission trips where the grant would cover the donor’s travel costs or a family member’s participation

- Payments to for-profit entities, including “charitable” programs run through a business

Some of these are clearly prohibited in many cases; others depend on how the charity structures the program and whether the donor receives more than incidental benefits. The practical point is that donors should not have to guess. A tax attorney can interpret the facts, and the DAF sponsor can confirm its policies.

Regulatory attention has increased around DAFs

DAFs are widely used, and regulators continue to examine how they function. Even when donors are acting in good faith, the public-policy scrutiny is real. The IRS has noted DAFs and related compliance issues in its exempt organizations priorities and published guidance in recent years: IRS Exempt Organizations annual report and work plan. The lesson for donors is not fear; it is prudence. Complex grants should be structured so they remain unambiguously charitable.

Consult a tax lawyer when family and estate planning intersects with DAFs

Christian donors often want to shape family generosity across generations. DAFs can support that goal, but they are not a full estate plan. When a DAF becomes part of legacy intent—especially with multiple heirs, blended families, or significant assets—legal coordination becomes a form of care for both the donor’s witness and the family’s peace.

Successor advisors and governance within the family

Many sponsors allow successor advisors, enabling children or other designees to recommend grants after the donor’s death. The legal questions arise when donors attempt to exert control beyond what the sponsor permits, or when family governance is unclear. A tax lawyer can help a donor coordinate beneficiary designations, successor advisor arrangements, and estate documents so they do not conflict.

This is also where pastoral wisdom and legal precision belong together. Scripture commends ordered provision and the avoidance of unnecessary contention. “If possible, so far as it depends on you, live peaceably with all” (Romans 12:18). A coherent plan reduces confusion and protects relationships when decisions become weighty.

Coordinating DAFs with private foundations and trusts

Some donors use both a DAF and a private foundation: the DAF for simpler grants and anonymity when appropriate, the foundation for staffing, direct charitable activities, or tightly governed family philanthropy. This can be appropriate, but it can also create self-dealing pitfalls and payout confusion if not structured well. When trusts, donor intent provisions, or international giving are involved, counsel is typically necessary.

For donors building a broader approach, our Christian Donor-Advised Funds resource is a useful orientation to what DAFs are best suited to accomplish and where adjacent tools may serve better.

Consult a tax lawyer when the ministry relationship or grant purpose is contested

Not every reason to consult a tax lawyer is purely technical. Some situations involve disputes, unclear facts, or heightened reputational stakes. For Christian donors, these moments can carry an additional moral weight: the desire to support faithful work without enabling poor governance or creating a public stumbling block.

When a ministry is new, opaque, or structurally unusual

A DAF can recommend grants to many legitimate Christian ministries, but donors should not assume that a compelling story equals a compliant structure. Some organizations operate through fiscal sponsors, affiliated entities, or complex networks of related parties. Others are led by founders who have not built mature governance. Those patterns do not automatically mean wrongdoing, but they merit due diligence—legal, financial, and practical.

Across our verification work at Most Trusted, we observe that ministries that meet The Most Trusted Standard tend to document decision-making, disclose related-party transactions, and publish clear financial information. Those practices do not replace legal review, but they reduce the likelihood that a donor’s generosity becomes entangled with preventable controversy.

When a grant is tied to a restricted purpose or sensitive outcome

Restricted giving can be faithful stewardship: funding a specific program, a capital campaign, or a targeted initiative. It can also create disputes if expectations are not documented or if the recipient’s circumstances change. A tax lawyer can help donors understand how restrictions interact with the DAF sponsor’s control and the recipient’s discretion.

For donors discerning these questions in greater depth, Tax and Legal Basics of Christian Donor-Advised Funds addresses the recurring legal and compliance themes that surface in higher-stakes giving.

FAQs for When to consult a tax lawyer about a donor-advised fund

Do we need a tax lawyer to open or use a donor-advised fund?

Most donors do not. For routine contributions of cash or publicly traded securities and ordinary grants to established 501(c)(3) charities, the DAF sponsor’s process and a competent CPA are often sufficient. Legal counsel becomes advisable when the contribution involves complex assets, the timing intersects with a sale, the grant could create private benefit, or the DAF is integrated into estate and family governance decisions.

Can a donor-advised fund pay for our mission trip, tuition, or a ticketed fundraiser?

Generally, no when the payment would confer a more-than-incidental personal benefit to the donor or family members, or when it functions as a purchase. The facts and the sponsor’s policies matter, and there are limited scenarios where a charity structures a program so that a donor receives no impermissible benefit. A tax lawyer can assess the specific arrangement before a recommendation is made.

Stewardship that is legally careful is spiritually serious

Christian donors do not consult tax lawyers because generosity is merely a transaction. We do so because generosity is accountable: to God, to the public trust, and to the ministries we aim to strengthen. When DAF giving becomes complex—through assets, timing, grants, or family legacy—qualified legal counsel is often the simplest path to preserving both compliance and conscience.