Planned giving options for Christian retirees are not primarily tax tactics. They are a disciplined way to convert a lifetime of accumulation into a final season of witness, ordered love, and durable support for the Church’s work. Retirement concentrates the question. Income is often fixed, health costs are less predictable, and heirs may be entering adulthood with their own needs and assumptions about money.

Scripture does not romanticize wealth, but it does treat stewardship as morally serious. Jesus’ warning that “where your treasure is, there your heart will be also” (Matthew 6:21) presses directly on estate plans and beneficiary designations. Planned giving becomes one of the last places a believer can make choices that are both practical and explicitly theological.

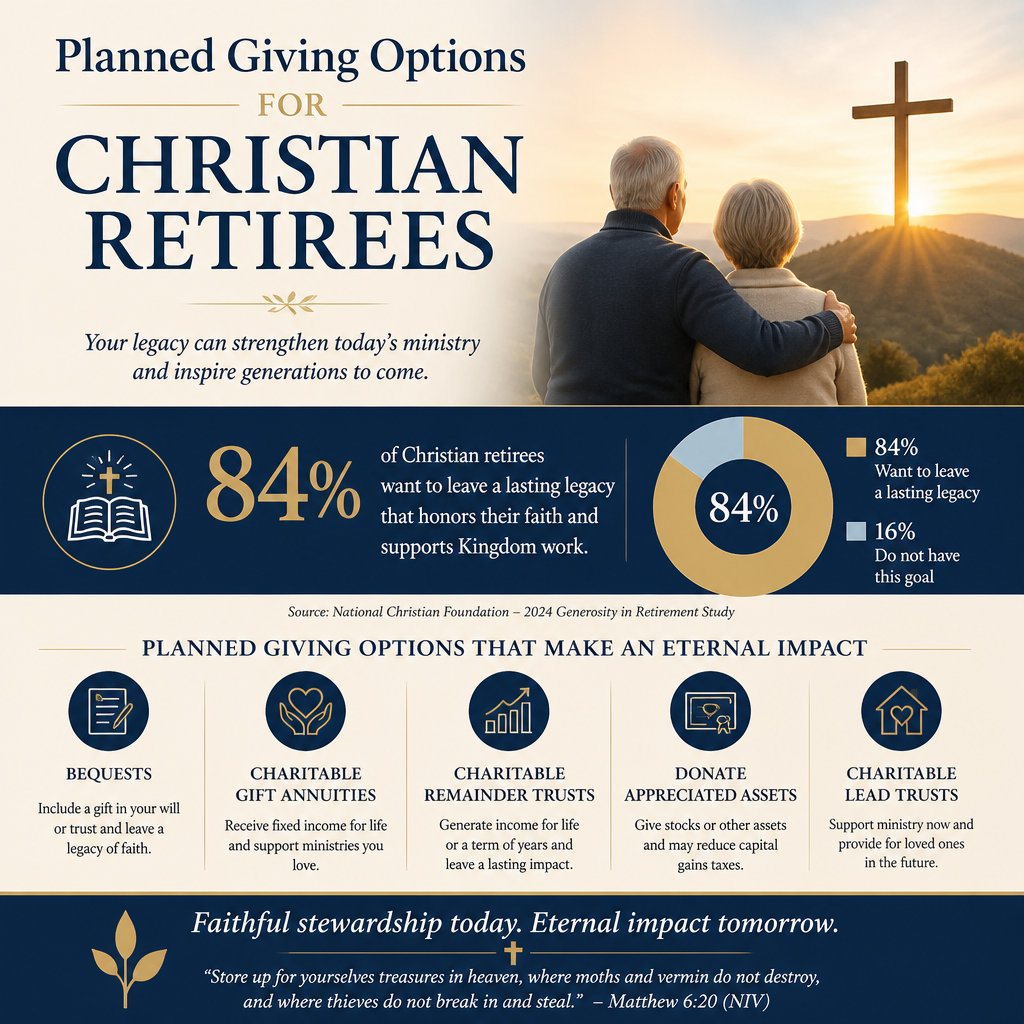

Retirement changes the stewardship equation

Income risk and longevity risk are real

Retirees commonly face a set of trade-offs that are not present in peak earning years: inflation risk, sequence-of-returns risk, and the possibility of long-term care needs. Planned gifts can honor generosity while preserving appropriate resilience for a spouse, dependent family members, or personal medical obligations. Christians genuinely disagree about where “enough” becomes “excess,” but most agree that prudence is not unbelief. Joseph stored grain; he did not hoard it for private glory.

What this means in practice is that planned giving works best when it is integrated with a clear cash-flow picture and an honest view of what heirs will realistically need. Many families discover that the conflict is not between “family or ministry,” but between an unexamined default and a prayerfully reasoned plan.

Most giving is already planned, whether or not we admit it

Beneficiary designations, required minimum distributions, and the structure of one’s portfolio already determine who receives value and when. The question is whether those defaults align with Christian conviction. Planned giving is often less about adding complexity and more about correcting drift: ensuring generosity is not crowded out by inertia, market habits, or a lack of conversation.

The simplest options are often the most faithful

Bequests in a will or trust

A charitable bequest directs assets to a ministry at death through a will or living trust. It is frequently the most straightforward planned gift because it does not reduce current income and is easy to adjust as circumstances change. A bequest can be a fixed dollar amount, a percentage of the estate, or a “residuary” bequest that gives what remains after other commitments are met.

For Christian retirees who want to care well for a surviving spouse and still leave a meaningful witness, percentage-based bequests often balance clarity and flexibility. They also reduce the likelihood that the charitable gift is unintentionally diminished by later life expenses.

Beneficiary designations on retirement accounts

Retirement accounts can be especially effective for charitable giving because the gift typically avoids income tax that would otherwise be owed when heirs withdraw funds. Many donors choose to name a qualified ministry as a beneficiary of some portion of an IRA or 401(k), while leaving other assets to children.

This is also an area where errors are common. Beneficiary forms override a will. A carefully written estate plan can be undone by an outdated designation that still lists a former employer plan, an ex-spouse, or an estate rather than specific individuals or ministries. A disciplined annual review is a form of stewardship.

Gifts that support ministry and preserve lifetime income

Charitable gift annuities

A charitable gift annuity is a contract with a charity: the donor makes an irrevocable gift, and the charity pays a fixed income stream for life (sometimes for two lives). These arrangements can support a ministry while providing predictable income, which appeals to retirees who value stability. The trade-off is permanence. Once established, the gift generally cannot be undone, and the donor is relying on the charity’s financial strength and reserve practices.

Because of that reliance, donors should ask whether the issuing organization has audited financials, clear board oversight, and transparent reserve policies. Across our verification work at Most Trusted, the ministries that meet The Most Trusted Standard tend to treat long-term obligations with documented seriousness: clear governance, appropriate financial controls, and public transparency that allows a donor to evaluate risk rather than assume it away.

Charitable remainder trusts

A charitable remainder trust (CRT) provides income to the donor or other beneficiaries for a term of years or for life, with the remainder passing to charity. CRTs can be funded with appreciated assets, which may allow a donor to diversify without immediate capital gains tax, while still reserving income. These trusts can be powerful tools, but they introduce administrative cost and legal complexity. They are rarely appropriate for modest estates.

For Christian families, the deeper question is not merely efficiency but intent: does the structure serve a clear stewardship purpose, or does it become a way to avoid decisive generosity? A CRT can be a faithful instrument, but it should be anchored in a coherent plan rather than treated as a spiritual substitute for clarity.

Tax-aware giving without letting taxes become the master

Qualified charitable distributions from IRAs

Qualified charitable distributions (QCDs) allow eligible taxpayers to give directly from an IRA to a qualified charity, potentially satisfying required minimum distributions while keeping the distribution out of taxable income. For many retirees, this is one of the cleanest ways to fund regular generosity when itemized deductions are limited. The IRS describes the basic rules and limits in its retirement plan guidance (IRS retirement plans).

QCDs also reinforce a formative habit: generosity as a first claim, not merely what remains. Christians genuinely disagree about whether the tithe applies directly to modern income streams, but few dispute that disciplined, prioritized giving is a means of spiritual formation.

Donor-advised funds for structured generosity

Donor-advised funds (DAFs) can help retirees make a larger gift in a high-income year, receive an immediate charitable deduction, and then grant to ministries over time. They can also help families involve children in grant recommendations, turning generosity into shared formation rather than a private financial decision.

The tension is real: DAFs can become warehouses for delayed obedience if grants are not made consistently. Donors should set an internal policy for grant timing and communicate it to family. Where the heart intends generosity, the calendar should confirm it.

- Review beneficiary designations annually and after any major life change.

- Decide which assets are best suited for heirs and which for ministry support.

- Establish a giving policy for any donor-advised fund, including a minimum annual grant rate.

- Ask ministries for audited financials and clear governance disclosures before making complex commitments.

- Coordinate your plan with a qualified attorney and tax professional, then document it clearly for executors.

Choosing ministries worthy of a legacy gift

Why verification matters more as gifts get larger

Legacy gifts are often among the largest single gifts a ministry will ever receive from a household. They also arrive when the donor can no longer correct course. That reality raises the bar. Good intentions do not substitute for evidence of integrity, doctrinal seriousness, and operational competence.

Most Trusted exists because donors deserve more than marketing claims. We evaluate Christian nonprofits against The Most Trusted Standard, a 15-criteria framework that examines faith foundations, financial integrity, governance and leadership, and transparency and effectiveness. Donors can explore the broader landscape of Christian Stewardship Services as they assess where their giving decisions fit within their full stewardship life.

Common red flags in planned giving outreach

Many ministries handle planned giving responsibly. Some do not. A sophisticated donor will watch for patterns that signal future risk: reluctance to provide audited financial statements, unclear board oversight, aggressive pressure to make irrevocable gifts, or vague promises about impact without verifiable reporting. The “Overhead Myth” letter—signed by major charity evaluators—helped correct simplistic assumptions about overhead ratios, but it also underscored the need for meaningful transparency and outcomes rather than cosmetic efficiency (Candid/GuideStar on the Overhead Myth).

Good legacy giving is patient. It asks more questions, not fewer. It honors ministry leaders by expecting the kind of governance that withstands scrutiny.

Integrating planned giving with family, church, and conscience

Heirs need clarity more than they need secrecy

Estate decisions can strain families when surprises appear after death. A legacy gift can be a profound testimony, but it can also be perceived as rejection if it is unexplained. Many Christian retirees choose to write an ethical will or legacy letter that explains their decisions in explicitly theological terms: gratitude for God’s provision, love for family, and confidence that the gospel outlasts any household.

This is also where church life matters. Planned giving should not replace ordinary, local faithfulness. Scripture’s steady emphasis on the local church’s shared life makes it difficult to justify a legacy plan that bypasses congregational responsibility entirely. Christians disagree on the right balance between local and external giving, but most mature plans have both.

Guarding against spiritual distortion

Planned giving can serve pride as easily as it serves love. Naming opportunities after donors, cultivating influence through gifts, or treating philanthropy as reputation management can quietly hollow out generosity. Jesus’ warning in Matthew 6 about practicing righteousness “to be seen by others” applies to large gifts as much as to small ones. Wise donors structure giving in ways that reduce the temptation to control outcomes beyond their proper role.

For donors who want additional context on how planned giving intersects with stewardship practice and ministry evaluation, resources in Christian Stewardship Services and Planned Giving can help frame next steps without reducing the decision to financial technique.

FAQs for Planned giving options for Christian retirees

Should a Christian retiree prioritize heirs or ministry in an estate plan?

Scripture affirms obligations to family and calls Christians to durable generosity. The question is rarely either-or. Many faithful plans provide well for a spouse, set clear expectations for children, and still direct meaningful resources to ministries that will remain at work beyond the donor’s lifetime. The most helpful discipline is to decide intentionally rather than defaulting to cultural norms or avoiding the conversation.

How can we evaluate whether a ministry is safe to include in a planned gift?

Start with verifiable disclosures: audited financial statements, clear board governance, transparent leadership practices, and credible reporting on outcomes. Ask whether the ministry’s public communication matches what its documents show. Because planned gifts are difficult to reverse, independent evaluation becomes more valuable, not less. Most Trusted’s verification work, grounded in The Most Trusted Standard, is designed to help donors assess ministries with evidence rather than assumption.

A legacy that is coherent, not merely generous

Planned giving options for Christian retirees work best when they express a coherent theological vision: provision without fear, generosity without manipulation, and trust that God’s Kingdom advances through faithful stewardship. The practical tools matter, but the order of love matters more. A well-made plan blesses family, strengthens the Church’s work, and leaves heirs not only assets, but a pattern worth imitating.