How charitable gift annuities work for Christian legal ministries is a practical question with spiritual weight. It asks how to fund truth-telling, advocacy, and the quiet, costly work of serving people in legal vulnerability without turning ministry into a sales pitch or a speculative bet.

Christian legal ministries often sit at the intersection of pastoral care and public responsibility: defending religious freedom, providing immigration and asylum counsel, helping survivors obtain protective orders, supporting prisoners and returning citizens, or equipping churches to respond faithfully to legal pressures. Donors who care about this work are frequently also thinking about retirement income, tax stewardship, and the long arc of faithfulness. A charitable gift annuity can be one of the few tools that addresses all three.

What a charitable gift annuity is and what it is not

A contract with a ministry, not a market product

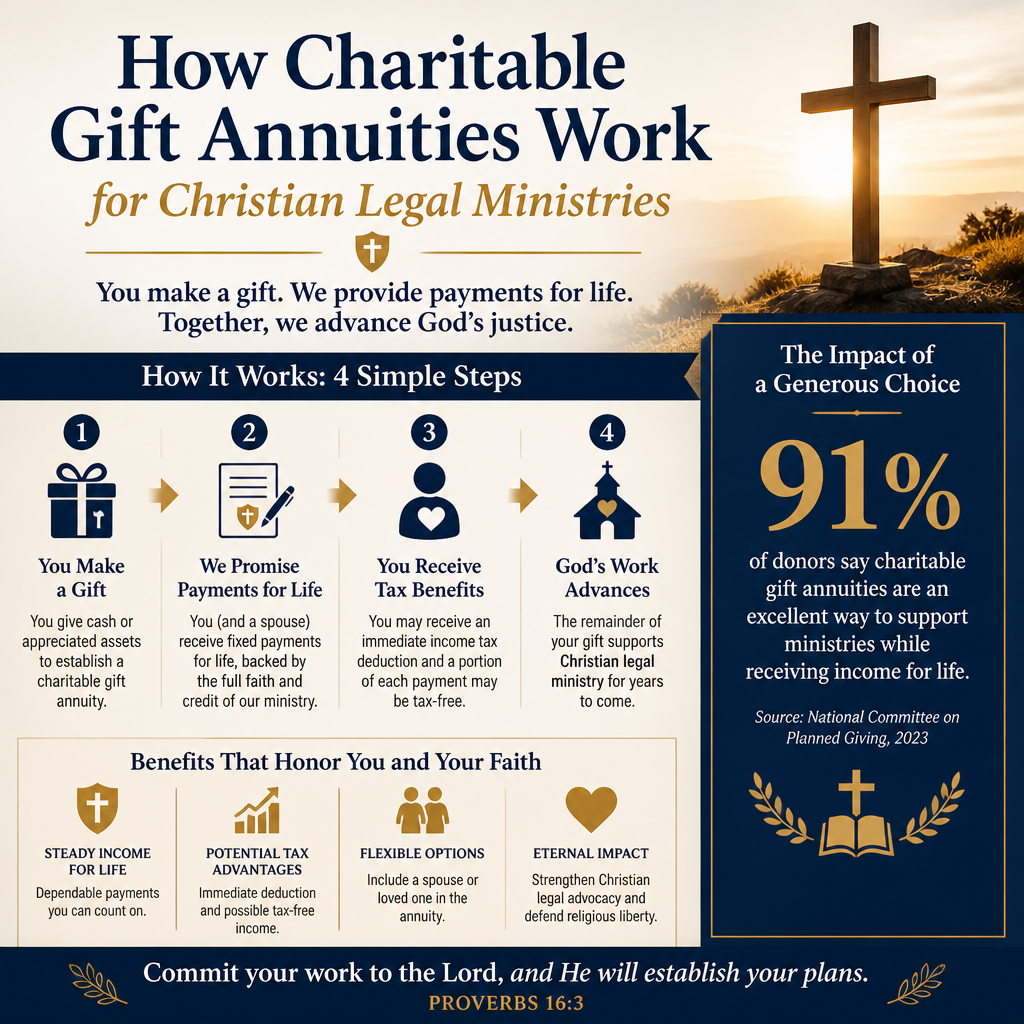

A charitable gift annuity, often shortened to CGA, is a simple contract: a donor makes an irrevocable gift to a qualified charity, and in return the charity promises to pay a fixed income stream to one or two annuitants for life. When the annuitant dies, the remaining value stays with the charity for its mission.

This is not a donor-advised fund, not a private foundation, and not an investment account. It does not rise and fall with markets, and it is not insured by the FDIC. The charity’s ability to pay rests on the charity’s financial strength and its legal obligation under state gift annuity rules. That is why sophisticated donors treat the issuing ministry’s financial integrity and governance as part of the gift decision, not as an afterthought.

Why ministries offer them at all

For the ministry, a CGA is a way to receive an immediate gift while honoring a donor’s desire for predictable lifetime income. For the donor, it can convert appreciated assets into a steady stream without selling the asset first and bearing the full tax impact up front.

For Christian donors, there is also a theological dimension. Jesus’ teaching consistently ties money to discipleship, not because money is ultimate, but because it is revealing (Matthew 6:21). A CGA can be a disciplined way to loosen the grip of wealth, provide for a spouse, and place capital under kingdom purposes rather than leaving it entirely to consumption or uncertainty.

How the economics and tax features usually work

Fixed payments, set at the start

The defining feature of a CGA is the fixed payout rate. Once established, the payment amount typically does not change. Many charities reference the recommended payout rates published by the American Council on Gift Annuities, which were designed to balance donor value with charitable remainder and financial prudence. The rates themselves are not law, but they function as an established norm in the field. Donors can review the council’s framework directly at American Council on Gift Annuities.

Because the payment is fixed, CGAs can be attractive in a planning context where predictability matters more than maximum upside. That is a trade-off, and it should be named plainly. A CGA is not the right instrument for every donor, especially for those who prioritize liquidity or want to retain control of principal.

Three common tax elements donors should understand

Tax treatment depends on the asset given, the donor’s age, the payout rate, and applicable IRS rules. Ministries and gift planning officers should not be treated as the donor’s tax counsel. Still, donors benefit from understanding the typical contours:

- Charitable income tax deduction: A portion of the gift is usually deductible in the year of the gift, subject to IRS limitations and substantiation rules.

- Partly tax-free income: A portion of each annuity payment is often treated as a tax-free return of principal for a period of years, based on an IRS calculation.

- Capital gain recognition may be spread out: When funding a CGA with appreciated assets, some of the capital gain is often recognized over time rather than entirely in the year of the gift.

These features are governed by IRS rules around charitable contributions and annuities. The IRS materials are technical but authoritative, and donors and advisors can begin with the agency’s guidance on charitable contributions at IRS.

What this means in practice is that a CGA can be a means of tax-wise generosity without turning giving into tax avoidance. Christians genuinely disagree about how much tax planning is spiritually healthy, but Scripture does not condemn prudence. It condemns greed, false security, and neglect of neighbor. A well-ordered plan can serve love.

Why charitable gift annuities fit Christian legal ministries in particular

Legal work is durable and often underfunded

Many Christian legal ministries carry costs that do not map neatly to donor expectations: professional staff, case management systems, security and confidentiality measures, and sometimes court-related expenses. At the same time, the fruit is often slow and difficult to measure in a single reporting cycle. The point is not that outcomes are unknowable; the point is that legal ministry often requires persistence more than spectacle.

A CGA aligns well with that reality because it is long-duration funding. It gives the ministry resources now and leaves a remainder later, creating two moments of support. For a ministry engaged in precedent-setting litigation, long-term client advocacy, or policy work that protects vulnerable communities, patient capital matters.

They can strengthen a ministry’s balance sheet but require discipline

A well-managed gift annuity program can provide stable funding and encourage a culture of planned giving. But the harder question is whether the issuing ministry has the governance, reserves, and transparency to carry a lifetime payment obligation responsibly.

Across our verification work at Most Trusted, we observe that donors are often attentive to theological alignment but less attentive to balance-sheet strength, board oversight, and the clarity of audited financial reporting. Yet a CGA intensifies those concerns. The ministries that meet The Most Trusted Standard tend to treat planned giving as a fiduciary responsibility: clear policies, careful reserve practices, and forthright disclosure rather than promotional pressure.

Donors who want a broader view of the field, including how ministries typically structure legal services and accountability, often begin with Christian Legal Services Ministries.

Due diligence for donors considering a gift annuity

Four questions that protect both donor and ministry

A charitable gift annuity is a gift, but it is also a contract. Christian donors should not confuse trust in the Lord with naivete about institutions. Due diligence is not cynicism; it is stewardship.

Before funding a CGA with a Christian legal ministry, we recommend asking:

- Is the ministry financially positioned to carry long-term obligations? Review audited financials, liquidity, and trends in unrestricted revenue.

- How is the annuity obligation reserved and reported? Responsible ministries disclose annuity liabilities and follow state requirements.

- Who governs the program? Look for board oversight, documented policies, and segregation of duties.

- Is the ministry clear about donor intent and use of funds? Legal ministry often has restricted program needs; clarity prevents misunderstanding later.

- Does the ministry communicate outcomes with sobriety and evidence? Avoid ministries that trade in inflated claims, especially in contentious legal arenas.

Why verification matters more with planned gifts

Because the payout obligation may last decades, the issuing organization’s integrity and stability are not secondary. This is where independent verification can serve donors. Most Trusted exists to help donors give with confidence by evaluating Christian nonprofits against The Most Trusted Standard, a 15-criteria framework that tests faith foundation, financial integrity, governance and leadership, and transparency and effectiveness.

The purpose of a framework is not to replace prayer or pastoral counsel. It is to supply evidence where evidence is appropriate, and to honor the biblical expectation that leaders be above reproach and that stewardship be faithful (1 Corinthians 4:2).

Common tensions and wise alternatives

Irrevocability and changing life circumstances

Once established, a CGA is generally irrevocable. That is not merely a technical detail. It is the heart of the instrument. For donors facing uncertain healthcare costs, supporting adult children, or anticipating long-term care, a large irreversible gift can be unwise even when generosity is strong.

Some donors address this by funding a CGA at a modest level relative to net worth, or by using a deferred gift annuity that begins payments later. Others decide that a bequest, beneficiary designation, or donor-advised fund better fits their circumstances. Each option carries different trade-offs in control, timing, and ministry benefit.

When a CGA may not be the best tool

A CGA may be a poor fit when the donor needs liquidity, when the asset is better used through a charitable remainder trust, or when the ministry does not have the administrative maturity to run an annuity program responsibly. It can also be a poor fit when the donor is primarily motivated by maximizing payout rather than making a gift. A gift annuity is designed to include a charitable component; when that intent is absent, the instrument is being asked to carry weight it was not built to bear.

Donors weighing these choices within a broader strategy of tax stewardship often consult Tax-Smart Giving to Christian Legal Services to understand how different tools align with both conviction and circumstance.

FAQs for How charitable gift annuities work for Christian legal ministries

Are charitable gift annuities safe if a ministry faces financial trouble?

A charitable gift annuity is a general obligation of the issuing charity, so payment security depends on the charity’s overall financial health and compliance with state gift annuity requirements. It is not FDIC-insured, and it is not the same as a commercial annuity issued by an insurance company. Donors should review audited financial statements, governance practices, and the ministry’s track record of transparency before entering a long-term payment contract.

Can a charitable gift annuity be funded with stock or other appreciated assets?

Many gift annuities are funded with appreciated securities, and doing so can be attractive because the donor may receive a charitable deduction and may recognize capital gain over time rather than entirely in the year of the gift, depending on the specific circumstances and IRS rules. The exact tax result depends on the asset, the donor’s age, the payout rate, and other factors, so donors should involve qualified tax counsel and confirm the ministry’s acceptance policies for non-cash gifts.

A faithful instrument when it is used faithfully

Charitable gift annuities work best for Christian legal ministries when donors and ministries both approach them as a covenantal responsibility rather than a financial product. The donor gives irrevocably with clear charitable intent and sober attention to personal obligations. The ministry accepts long-term liability with governance discipline, transparent reporting, and a mission worthy of durable support. When those conditions are met, a CGA can fund legal work that protects the vulnerable, strengthens the church’s public witness, and endures beyond a single season of attention.