What to check in Christian financial ministry statements is not a narrow accounting question. For donors, it is part of spiritual stewardship: whether the ministry’s public promises about handling God’s money can be verified with ordinary evidence. Ministries that manage money on behalf of others carry an added moral burden, because financial opacity does not only risk inefficiency; it risks the trust that makes generosity possible.

Christian financial service ministries sit in a complex space. Some are regulated financial institutions; others are nonprofit ministries providing counseling, benevolence, or training; still others function as intermediaries between donors and downstream programs. Christians genuinely disagree about how much “proof” a donor should require before giving. Yet Scripture’s insistence on integrity in weights and measures (Proverbs 11:1) presses us toward clarity rather than sentiment, and toward verifiable practices rather than reassuring language.

Begin with the statement itself, not the ministry story

Confirm the document type and reporting basis

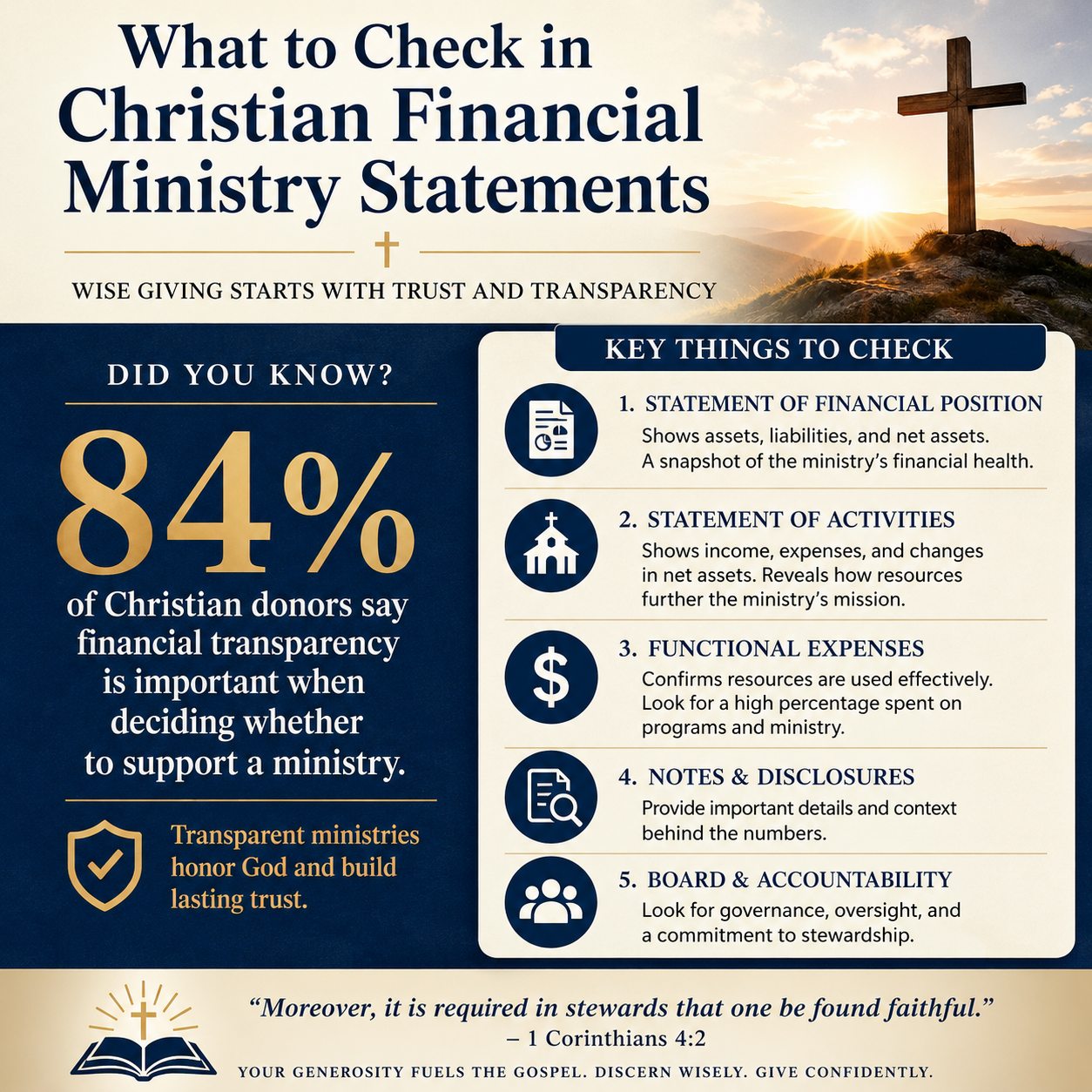

Many donor questions are resolved by identifying what the ministry has actually published. A full set of financial statements generally means a balance sheet, a statement of activities, and a statement of cash flows, accompanied by notes. Ministries sometimes post internal summaries that resemble financial statements but omit cash flow, omit notes, or blend categories in ways that prevent meaningful review.

Next, look for the reporting basis and standards. For U.S. nonprofits, generally accepted accounting principles are the norm, and audited statements should clearly indicate an independent audit opinion. If the ministry uses a different basis of accounting, the statement should say so plainly and explain limitations. A faithful ministry is not threatened by precision; it is strengthened by it.

Check time period, comparatives, and restatements

Financial statements should specify the fiscal year, present comparative prior-year figures, and disclose material restatements. Comparatives allow donors to see trend lines: whether growth is accompanied by strain, whether reserves are declining, or whether liabilities are rising. Restatements are not automatically disqualifying, but they demand explanation because they indicate prior reporting was materially wrong or incomplete.

When donors want to understand how to evaluate ministries in this field at a higher level, we situate this work within Christian Financial Service Ministries, where the central question is consistent: can claims about stewardship be supported by documents that withstand scrutiny?

Follow the money through revenue quality and restrictions

Identify the dominant revenue stream and its fragility

Two ministries can have identical total revenue and radically different risk profiles. A ministry funded primarily by broad individual giving typically faces different volatility than one dependent on a small number of major donors, a single church network, a government contract, or fee-for-service income. The statement of activities should show whether support is concentrated or diversified, and the notes often disclose concentrations that a top-line number conceals.

Revenue quality also includes whether funds are recurring, restricted, or one-time. A large gift can create the appearance of strength while masking a deficit in ongoing operations. Donors should read for sustainability rather than sentiment: what portion of the work is supported by predictable inflows, and what portion is dependent on episodic fundraising wins?

Read net assets for donor intent and flexibility

For nonprofits, net assets with donor restrictions matter because they reflect promises made to donors. A healthy ministry typically shows that restricted funds are tracked faithfully and released according to the satisfaction of restrictions. Chronic growth in restricted net assets alongside operational shortfalls can signal a mismatch between what donors want to fund and what the ministry needs to operate.

Conversely, a ministry with almost no restricted funds is not automatically healthier. Some ministries simply do not solicit restricted gifts, and some donors do not require restrictions. The question is whether the ministry communicates clearly about the difference between donor-restricted resources and funds available for general operations, and whether it avoids implying that restricted funds can cover unrelated needs.

Test financial integrity through liquidity, debt, and cash flow

Liquidity is not an optional metric for ministries handling financial needs

Donors often focus on ratios that are easy to repeat, but ministries fail more often from cash constraints than from “bad overhead.” The statement of cash flows is the place where hard reality shows up: whether operations generate cash, whether receivables are ballooning, and whether the organization is relying on financing to stay afloat.

Liquidity questions can be framed in plain terms: if revenue slowed for a season, could the ministry keep paying staff, honoring obligations, and serving people without immediate crisis? The notes may also disclose lines of credit and covenant requirements. If a ministry is close to covenant breach, donors should expect sober disclosure and a clear plan.

Debt and leases should match mission, not ambition

Debt is not inherently unspiritual, and Scripture does not forbid borrowing as a category. Yet taking on long-term obligations creates structural pressure that can reshape a ministry’s priorities, messaging, and fundraising posture. Ministries should disclose debt terms, maturity schedules, collateral, and interest rates. An expansion financed by heavy leverage can become a silent driver of program decisions.

Leases also matter, especially with modern accounting standards requiring many leases to be recognized on the balance sheet. A ministry that appears asset-light may in fact have significant long-term lease commitments. Donors are not “nitpicking” when they ask how fixed obligations compare to dependable revenue.

Evaluate spending with an eye for honesty, not simplistic ratios

Program, administration, and fundraising categories are useful but incomplete

The nonprofit sector has had to reckon with the damage caused by oversimplified overhead narratives. Charity Navigator, GuideStar, and the BBB Wise Giving Alliance publicly warned against using overhead ratios as the primary measure of nonprofit performance in their joint “overhead myth” letter (often cited across the sector) https://www.charitynavigator.org/. Mature donors should still review functional expenses, but as part of a broader credibility assessment rather than as a single scorecard.

What this means in practice is that donors should look for internal consistency. Does the ministry’s description of its work plausibly align with the level and kind of staffing it reports? Do fundraising expenses rise sharply without a clear explanation? Is there evidence of cost allocation practices that appear designed to “push” expenses into programs in a way that flatters public perception?

Compensation and related-party transactions require clarity

Executive compensation is a frequent flashpoint because it touches both justice and prudence. The financial statements and Form 990 together typically provide the most complete public window for U.S. nonprofits. Donors should expect the ministry to disclose compensation governance: whether salaries are set by an independent board, whether comparable data is used, and whether conflicts are managed.

Related-party transactions matter as well. If a ministry rents property from an officer, contracts with a board member’s company, or conducts business with an affiliated entity, the notes should disclose it. Such arrangements can be legitimate, but secrecy is rarely benign. Donors should be able to see the terms and evaluate whether they are fair.

- Are functional expense allocations explained in the notes, including the basis for shared costs?

- Is executive compensation governed by independent review rather than founder discretion?

- Are related-party transactions disclosed with clear terms and amounts?

- Do fundraising costs track with outcomes without suggesting desperation or manipulation?

- Is there evidence of mission drift driven by the need to cover fixed costs?

Use the statements to test transparency and effectiveness claims

Reconcile the financial statements with other public documents

A credible ministry’s story should match its documents. Donors should compare audited financial statements, annual reports, board lists, and (when applicable) Form 990 disclosures. Misalignments are often revealing: an annual report that describes extensive field operations while the statements show modest program expense; a ministry that emphasizes “no fundraising costs” while reporting significant fundraising staff; or a ministry that claims rapid growth while cash flow from operations remains negative.

In our verification work at Most Trusted, ministries that meet The Most Trusted Standard tend to treat reconciliation as a discipline rather than an inconvenience. They assume sophisticated donors will read across documents, and they publish in a way that rewards careful review.

Ask what the numbers cannot prove, and how the ministry compensates

Financial statements are necessary, but they are not sufficient. They do not directly measure spiritual fruit, pastoral faithfulness, or the quality of counseling and care. Christians genuinely disagree about how to quantify outcomes in ministries where the work is relational and long-term. Yet the absence of perfect metrics does not excuse the absence of any metrics.

The harder question is whether the ministry has a coherent view of effectiveness that is honest about limits. A financial counseling ministry, for example, may track participant completion, behavior change indicators, and follow-up outcomes while acknowledging selection bias and attrition. A benevolence ministry may track the proportion of aid delivered through churches, the timeliness of assistance, and safeguarding measures against fraud. The goal is not to reduce ministry to numbers, but to ensure that “good intentions” are tethered to accountable practice.

Donors who want a broader framework for these questions will find them addressed across Accountability and Transparency in Christian Financial Service Ministries, where the recurring standard is whether a ministry’s public-facing claims are matched by verifiable evidence and mature governance.

FAQs for What to check in Christian financial ministry statements

Is an audit required for a Christian ministry to be trustworthy?

An audit is not the only marker of trustworthiness, but it is one of the clearest forms of third-party verification available. Smaller ministries may not be able to sustain the cost of an audit, and some may use a review or compilation instead. What donors should require in every case is proportional transparency: clear statements, clear governance, clear disclosures of major risks, and a willingness to answer concrete questions without defensiveness.

What if a ministry says it cannot share financial statements because of security or privacy?

Security and privacy concerns can be real, especially for ministries working in sensitive contexts or with vulnerable clients. Yet those concerns rarely justify refusing to publish basic financial statements and notes. Mature ministries typically protect sensitive details while still providing meaningful public disclosure: aggregated figures, redacted names where appropriate, and a clear explanation of what is withheld and why. Donors should expect the ministry to offer an alternative form of verification rather than asking for trust without evidence.

A faithful donor standard is clarity proportionate to responsibility

Christian donors are not seeking perfection; we are seeking truthfulness, competence, and accountability. What to check in Christian financial ministry statements ultimately comes down to whether the ministry has made itself knowable: whether revenue is understandable, restrictions are honored, cash realities are disclosed, conflicts are managed, and public claims can be reconciled with documents. When ministries handle money on behalf of others, clarity is not a marketing choice. It is part of integrity before God and neighbor.