What happens to a Christian donor-advised fund at death is less a technical footnote than a final stewardship decision. A donor-advised fund is designed to outlive a season of income, a market cycle, or even a lifetime; the harder question is whether it will outlive us with clarity, faithfulness, and accountability.

Many Christian donors assume their donor-advised fund will “just continue” after they are gone. In practice, what happens depends on the sponsor’s policies, the legal instructions on file, and the spiritual seriousness with which successors approach the work. When those pieces are aligned, a donor-advised fund can become a stable channel of long obedience in the same direction. When they are not, it can drift into indecision, delay, or giving patterns no longer consistent with the donor’s convictions.

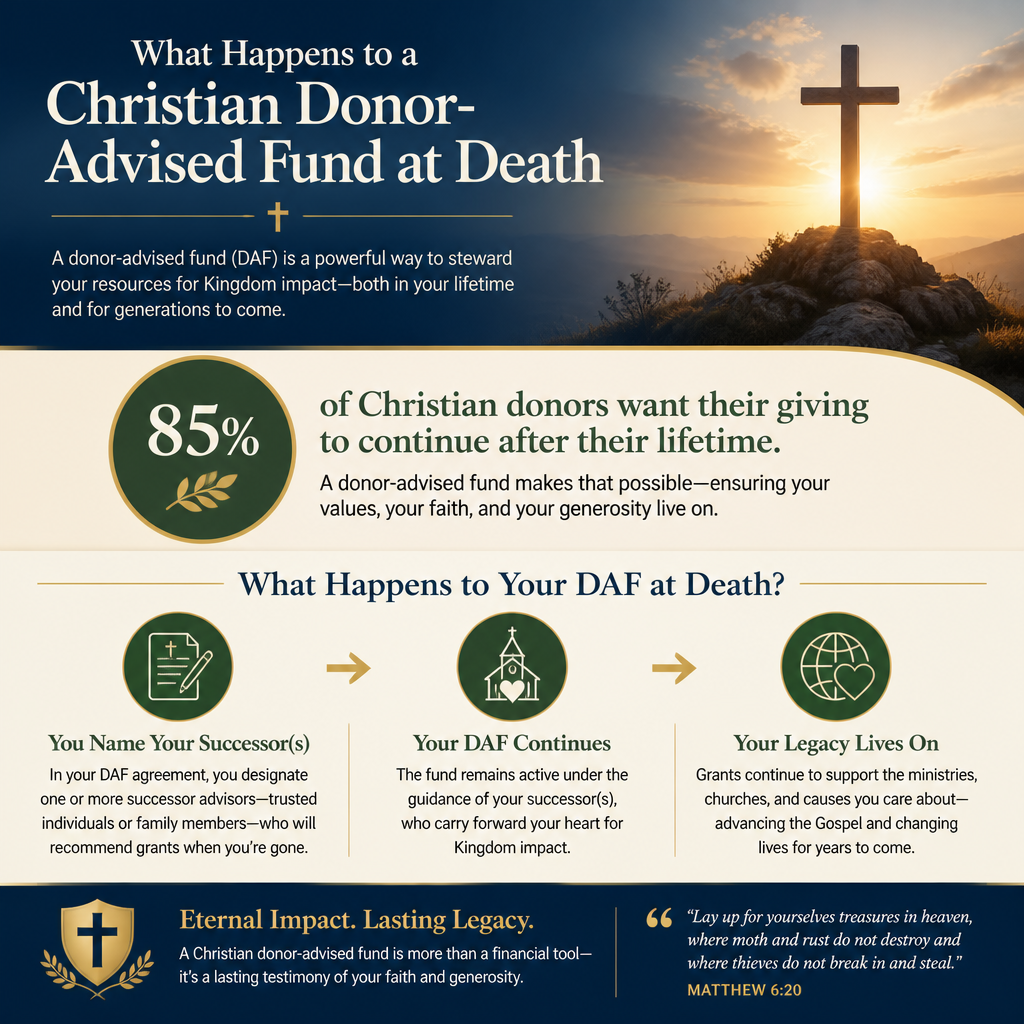

Death does not change ownership, but it does change who advises

A donor-advised fund is not owned by the donor in the same way a brokerage account is owned. Legally, the assets are held by the sponsoring organization, and the donor holds advisory privileges. That distinction matters at death: the fund does not typically pass through probate as a personal asset, and it is not distributed under a will as though it were private property. Instead, the sponsor looks to the successor plan the donor established, or to default policies if the donor left no clear instructions.

Advisory privileges usually transfer by designation, not by inheritance

Most sponsors allow donors to name successor advisors or successor account holders. These successor advisors may be spouses, adult children, trusted friends, or a committee. The donor’s death triggers the sponsor to confirm documentation, verify the successor’s identity, and then grant those individuals the ability to recommend grants within the sponsor’s guidelines.

What this means in practice is that “who should decide” is not a question to leave to family dynamics in a moment of grief. For many Christian households, generational discipleship is a sincere hope. Yet families also carry real differences in theology, politics, and institutional trust. Naming successors is as much a spiritual and relational discernment as it is an administrative task.

Some sponsors set limits on successor generations

Not every donor-advised fund is designed for indefinite family succession. Some sponsors allow one successor generation; others permit multiple generations; others require the fund to terminate after a set period. These policies vary by sponsor and by state context. Christian donors should ask directly: How long can this account continue? What happens after the last successor dies or resigns? What default recipients will the sponsor choose if the fund becomes inactive?

Planned giving is where many donors begin to consider Family and Legacy Giving Through Christian Donor-Advised Funds in a more disciplined way. The goal is not merely continuity, but continuity with integrity.

If you named no successors, the sponsor will follow its default policy

When a donor dies without a successor plan, the sponsor must still administer the fund responsibly. Sponsors typically treat an account with no successor as an account that should be distributed according to a default policy: perhaps to the sponsor’s own charitable programs, perhaps to a list of designated charities the donor previously supported, or perhaps to a general purpose charitable fund. Those outcomes can be legitimate, but they may not reflect the donor’s theological priorities or ministry relationships.

Default outcomes are rarely the donor’s best-case scenario

A default distribution policy is built for administrative necessity, not for personal discernment. It cannot account for the donor’s intent with the precision a thoughtful successor plan can. A Christian donor who spent decades supporting Bible translation, church planting, crisis pregnancy care, or theological education may not want their legacy to be decided by a generic policy designed for thousands of accounts.

Christians genuinely disagree about how tightly a donor should define “Christian” for charitable giving. Some donors want a doctrinal statement; others prioritize fruit and faithfulness in mission. Default policies tend to blur those distinctions. If theological intent matters, succession planning is not optional.

Inactive accounts can become delayed stewardship

Even when a sponsor does not immediately distribute a successor-less account, inactivity can create years of stalled giving. That can be a quiet failure of stewardship. Scripture treats stewardship as accountable action, not merely good intention. Jesus’ parable of the talents commends faithful investment toward the master’s purposes and condemns fearful or negligent preservation (Matthew 25:14–30).

In practical terms, donors should ask their sponsor: What counts as inactivity? How many months or years without grants triggers intervention? Does the sponsor have a process for contacting the estate or family, and what documentation is required?

Your fund can become a family discipleship tool or a family conflict point

For many Christian donors, the most compelling reason to continue a donor-advised fund after death is not merely tax efficiency. It is formation: training children and grandchildren to practice discernment, generosity, and trust in God’s provision. That is a worthy aim. It is also an area where naivete can do damage.

Successor advisors need more than access, they need a rule of life

A donor-advised fund can magnify either clarity or confusion. If successors inherit only a login and a balance, they are likely to default to whatever feels urgent, whatever is most emotionally persuasive, or whatever aligns with their own shifting convictions. If successors inherit a stated purpose, a grantmaking rhythm, and clear guardrails, they are more likely to practice faithful continuity rather than accidental reinvention.

Many donors leave behind some combination of these elements:

- A written purpose statement rooted in a theology of stewardship and mission

- A set of funding priorities, such as local church, mercy ministry, global missions, or Christian education

- Guidelines for what counts as a Christian ministry and what does not

- A process for evaluating ministries before recommending grants

- A plan for resolving disagreements among successor advisors

These are not legal instruments, but they often determine whether the successor era becomes coherent or contentious.

Some families should choose a committee model, not a single successor

There is no universally “biblical” answer to whether one person or a group should advise after a donor’s death. Yet wisdom literature consistently commends counsel and warns against unaccountable power (Proverbs 11:14). A committee model can protect against impulsive giving and can create space for shared discernment. At the same time, committees can also stall when members lack shared theological commitments or when conflict avoidance becomes policy.

Christian donors should be candid: are the potential successors aligned in doctrine and ministry philosophy? If not, a time-limited fund that spends down intentionally may serve the family and the Kingdom better than a multi-generational structure that becomes a recurring dispute.

Grantmaking integrity after death requires verifiable diligence

After a donor’s death, the spiritual and emotional incentives change. Successors may feel pressure to “honor” the donor by maintaining certain relationships, even when a ministry’s governance has weakened. Others may want to move the giving in a new direction with little accountability. In both cases, the core issue is discernment: whether successor grants are grounded in verifiable evidence of faithfulness.

Do not confuse Christian branding with Christian faithfulness

Christian donors are regularly targeted by compelling narratives and religious language. Some ministries are exemplary; others are sincere but poorly governed; a few are opportunistic. The difference is often visible not in the fundraising appeal but in governance practices, financial integrity, and transparency. Successor advisors need a disciplined approach that can outlast charisma.

Across our verification work at Most Trusted, we find that ministries that meet The Most Trusted Standard tend to document board oversight, publish meaningful financial disclosures, and communicate outcomes without manipulation. These are not secular demands imposed on the church; they are practical expressions of the biblical call to walk in the light and to avoid even the appearance of impropriety (2 Corinthians 8:20–21).

Due diligence becomes more important when the original donor is no longer asking questions

When a founder-donor is alive, long relationships can create informal accountability: meetings, hard questions, and a history of trust earned over time. After death, that relational accountability often fades. The successor era should therefore strengthen objective review rather than weaken it.

Many donors begin by clarifying what kind of evaluation their successors should use. Some rely on denominational accountability; others rely on audited financial statements and public reporting; others use third-party verification. Most benefit from a blended approach. For donors who want a consistent framework across diverse ministries, Most Trusted’s work is designed to support confidence by evaluating ministries against The Most Trusted Standard across faith foundation, financial integrity, governance and leadership, and transparency and effectiveness.

For broader context on how donor-advised funds function within faith-based generosity, see Christian Donor-Advised Funds.

Estate planning and donor-advised funds must be coordinated

Even though a donor-advised fund usually bypasses probate, it still sits within an overall legacy plan. A will, a trust, beneficiary designations, and the donor-advised fund succession form can easily contradict one another if they were created at different times or with different advisors. When that happens, the sponsor will generally follow the account’s governing documents and its own policies, not informal family expectations.

Three coordination points Christians often miss

First, donors sometimes name a successor advisor in the donor-advised fund paperwork but never tell the person, leaving them unprepared to carry the responsibility. Second, donors sometimes intend to “top up” the donor-advised fund at death but forget to name the sponsor as a beneficiary on the IRA, brokerage account, or life insurance policy. Third, donors sometimes name multiple successors without a tie-break mechanism, assuming unity that may not exist.

Christian stewardship is not only generosity; it is order. Paul’s instructions about orderly worship reflect a broader theological instinct: clarity is a form of love because it reduces confusion and prevents unnecessary conflict (1 Corinthians 14:33, 40).

Consider whether spend-down is the more faithful choice

Some donors assume that permanence is always better. Yet a time-limited donor-advised fund can be a strong expression of urgency and mission focus, particularly if successors are not prepared for ongoing discernment. A spend-down plan can concentrate impact, reduce administrative friction, and prevent drift. The decision is not primarily about optimism or pessimism; it is about aligning structure with spiritual reality.

FAQs for What happens to a Christian donor-advised fund at death

Does a donor-advised fund become part of the estate at death?

In most cases, no. Because the sponsoring organization holds the assets and the donor holds advisory privileges, the account typically does not pass through probate like a personally owned asset. What happens is governed by the sponsor’s account agreement and the successor designations on file, alongside applicable law and sponsor policy. Donors should confirm details with the sponsor and qualified estate counsel for their jurisdiction.

Can heirs withdraw money from a Christian donor-advised fund after the donor dies?

Generally, no. Successor advisors may be able to recommend charitable grants, but they cannot take distributions for personal use because the assets are held for charitable purposes by the sponsor. That restriction is part of what makes a donor-advised fund a disciplined stewardship vehicle rather than an inheritance tool.

A faithful end requires faithful instructions

A Christian donor-advised fund can extend generosity beyond death, but it cannot extend discernment unless donors build it into the plan. Naming successors, setting theological and practical guardrails, coordinating with the estate plan, and requiring verifiable diligence are not administrative extras. They are how a donor’s final act of stewardship becomes an ordered gift rather than an unresolved question.