Learning how to read a Christian camp ministry budget is one of the most practical acts of stewardship a donor can undertake. Camp ministries trade in sacred trust: parents entrust children, churches entrust reputations, and donors entrust resources meant to form young disciples rather than merely fund a pleasant week outdoors.

A budget is not a spiritual report card, but it is never spiritually neutral. Jesus’ teaching assumes that money reveals priorities with unusual clarity: “For where your treasure is, there your heart will be also” (Matthew 6:21). What this means in practice is that a camp’s budget can illuminate its theology of ministry, its operational competence, and its willingness to tell the truth about what it costs to disciple children and students well.

Start with the story the budget is telling

Read the budget as mission translated into math

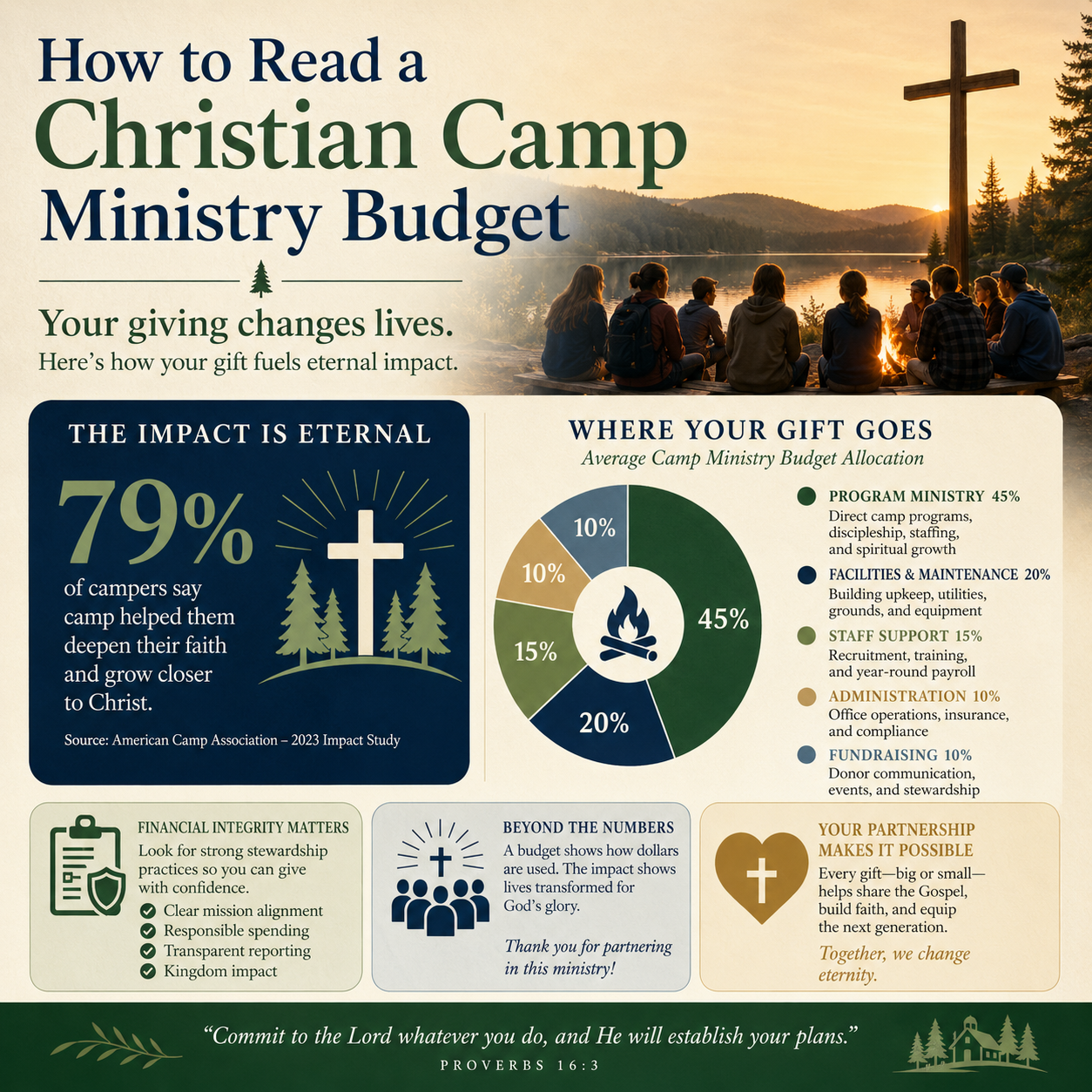

Budgets are moral documents because they convert stated mission into funded decisions. A Christian camp may say its focus is evangelism, discipleship, and safe community. The budget shows whether that focus is resourced: trained counselors, program staff, adequate supervision ratios, background checks, food service capable of meeting dietary needs, and facilities maintained to avoid preventable injuries.

Across our verification work at Most Trusted, we observe that the most trustworthy ministries can explain the “why” behind major categories without defensiveness. Mature financial leadership does not treat donors as obstacles to be managed. It treats them as stewards to be informed.

Know what documents you should ask for

A single-year budget snapshot is rarely enough. For camp ministries with a separate legal entity, donors should request recent audited financial statements when available, the current-year operating budget, and a multi-year view of capital needs (cabins, waterfront, vehicles, deferred maintenance). If the organization files a Form 990, it can often be found through the IRS Tax Exempt Organization Search irs.gov.

Even when a camp is part of a church or denomination and does not file a public 990, a serious ministry can still provide a board-approved budget, internal financials, and a clear description of oversight. The absence of a 990 is not automatically a red flag; the absence of meaningful disclosure often is.

Interpret revenue lines with donor realism

Program fees, donations, and the theology of access

Most camps rely on a mixture of tuition or program fees, donations, and sometimes conference rentals. The first question is not “Which is better?” but “What does the mix imply about the camp’s model?” A camp funded primarily by camper fees may be structurally stable but can drift toward serving only families who can pay. A camp funded heavily by donations may be able to subsidize access but becomes more vulnerable to economic cycles and donor concentration.

Many donor concerns land here: “Are we underwriting luxury?” “Are we subsidizing discipleship for those who otherwise could not attend?” “Is the camp quietly dependent on one benefactor?” These are legitimate questions, and the budget can answer them with specificity: scholarship line items, scholarship policy, and whether scholarship funds are restricted and used accordingly.

Restricted funds, designated gifts, and revenue you cannot spend freely

One of the most common misunderstandings is treating “revenue” as interchangeable with “money available for operations.” Restricted gifts are legally and ethically constrained to their intended purpose. A capital campaign for a new dining hall does not pay for counselor training, and a designated scholarship fund should not be used to cover fuel costs.

When a budget includes significant restricted revenue, donors should look for matching restricted expenses and clear fund accounting practices. Organizations that meet The Most Trusted Standard tend to separate restricted and unrestricted activity in a way a non-accountant can still follow, because clarity is part of faithfulness.

Assess expenses as indicators of integrity and competence

Personnel costs are usually the center of the ministry

In camp ministry, payroll is often the largest line item, and that is frequently appropriate. Discipleship is labor-intensive, and safety requires staffing. A low personnel line can signal under-staffing, high turnover, or over-reliance on minimally trained seasonal labor. Those conditions can quietly increase risk for campers and staff alike.

Donors should ask how staff are selected, trained, supervised, and retained. A budget that allocates meaningfully to training, background checks, and supervisory capacity is often a sign of sober leadership. It is not “overhead” in the pejorative sense; it is part of loving neighbor prudently.

Facilities and deferred maintenance are not optional for credibility

Camps sit on real assets: cabins, ropes courses, waterfront equipment, vehicles, kitchens, and HVAC systems. A budget that chronically underfunds repairs and maintenance can create a hidden debt that will be paid later through emergency fundraising, program disruption, or increased safety incidents.

Donors should look for a planned maintenance line, reserve funds, and a schedule for capital replacements. When a camp only funds maintenance through sporadic special gifts, it may be living in what fundraising research has described as the “starvation cycle,” where organizations underinvest in the real cost of operations and then struggle to perform well. The concept is widely discussed in nonprofit finance literature, including analysis in Stanford Social Innovation Review ssir.org.

Understand overhead without falling for simplistic ratios

Program versus administrative is not the whole truth

Christian donors often inherit a moral instinct that “program” spending is good and “administration” is suspect. The instinct is understandable, but simplistic ratios do not reliably measure effectiveness or integrity. Wise donors want ministries that spend appropriately on governance, accounting, safety systems, and staff development, because these enable excellent ministry at scale.

The nonprofit sector has pushed back on ratio fixation for years. Charity Navigator, Candid, and BBB Wise Giving Alliance issued a joint statement warning that overhead ratios can mislead donors and encourage underinvestment in capacity charitynavigator.org. Camp ministry is a clear case: a “lean” budget that skimps on risk management and staff training can be far more expensive in human terms than a responsibly resourced operation.

What healthy overhead can look like in a camp setting

Administrative and fundraising costs can be healthy when they fund real accountability: accurate bookkeeping, timely donor receipting, internal controls, board reporting, and truthful communications. In camps, certain cost centers may be categorized as “administration” even though they protect children and strengthen ministry outcomes: insurance, compliance, IT systems for medical forms, and professional development.

Christians genuinely disagree about what constitutes “acceptable” overhead, in part because camps vary widely in size, property complexity, and seasonality. The more reliable approach is to ask whether overhead spending is disciplined, explainable, and connected to measurable risk reduction and program quality.

Use the budget to ask governance and transparency questions

Internal controls and segregation of duties

A budget cannot prove internal controls, but it can raise the right questions. Who approves expenses? Who reconciles bank accounts? Are there limits on staff spending authority? Does the board receive regular financial reports that compare budget to actual results? These are not merely technical details; they are concrete expressions of the biblical call to honesty and accountability.

Even small camps can build basic segregation of duties, or compensate for limited staff through board involvement and external bookkeeping support. A camp that says, “We are too small for controls,” is often announcing vulnerability. A camp that says, “We have designed controls appropriate to our scale,” is demonstrating maturity.

Questions donors can ask without antagonism

Christian donors should not have to choose between being discerning and being charitable. A respectful set of questions can strengthen a ministry’s clarity and protect its witness. The following prompts tend to surface substance quickly:

- How are scholarships funded, awarded, and tracked against restricted gifts?

- What portion of staff costs are seasonal, and what portion are year-round leadership and discipleship roles?

- What is the plan for major capital replacements over the next five to ten years?

- How does the board review budget-to-actual performance during and after the camp season?

- What financial contingencies exist if enrollment or rentals fall short?

When donors want a broader framework for evaluating these questions across ministries, Most Trusted’s work in Christian Camps and Conferences reflects what we see repeatedly: transparency is rarely perfect, but it can be consistent, verifiable, and oriented toward truth rather than impression management.

For donors who want a more focused lens on disclosure practices, financial reporting, and whether an organization communicates clearly about use of funds, our analysis in Accountability and Transparency in Christian Camps and Conferences aligns with a simple conviction: Christian ministries should not require donors to make blind leaps of trust.

FAQs for How to read a Christian camp ministry budget

Should a Christian camp have an audit?

Not every camp will have audited financial statements, especially if it is small or operates under a parent organization. When a camp is sizable, handles significant restricted gifts, or runs complex operations, an independent audit can be a prudent safeguard and a credibility marker. The better question is whether the level of external financial review matches the camp’s scale and risk profile, and whether leadership can explain what oversight exists when an audit is not present.

Is a low overhead percentage a sign the camp is well run?

Not necessarily. Overhead ratios can be manipulated by accounting choices, and low overhead can signal underinvestment in safety, training, compliance, or financial controls. A healthier approach is to ask whether administrative and fundraising expenses are disciplined and connected to real accountability and program quality, while program spending reflects the true cost of responsible ministry.

Stewardship that strengthens the camp and the church

A Christian camp ministry budget repays careful reading because it reveals whether the ministry is prepared to disciple children with competence, protect them with seriousness, and speak truthfully about what that work costs. Donors do not honor Christ by demanding artificial cheapness, nor by ignoring warning signs out of goodwill. We honor Christ by giving in a way that joins generosity to discernment, so that camp ministry can remain a credible witness to the gospel it proclaims.