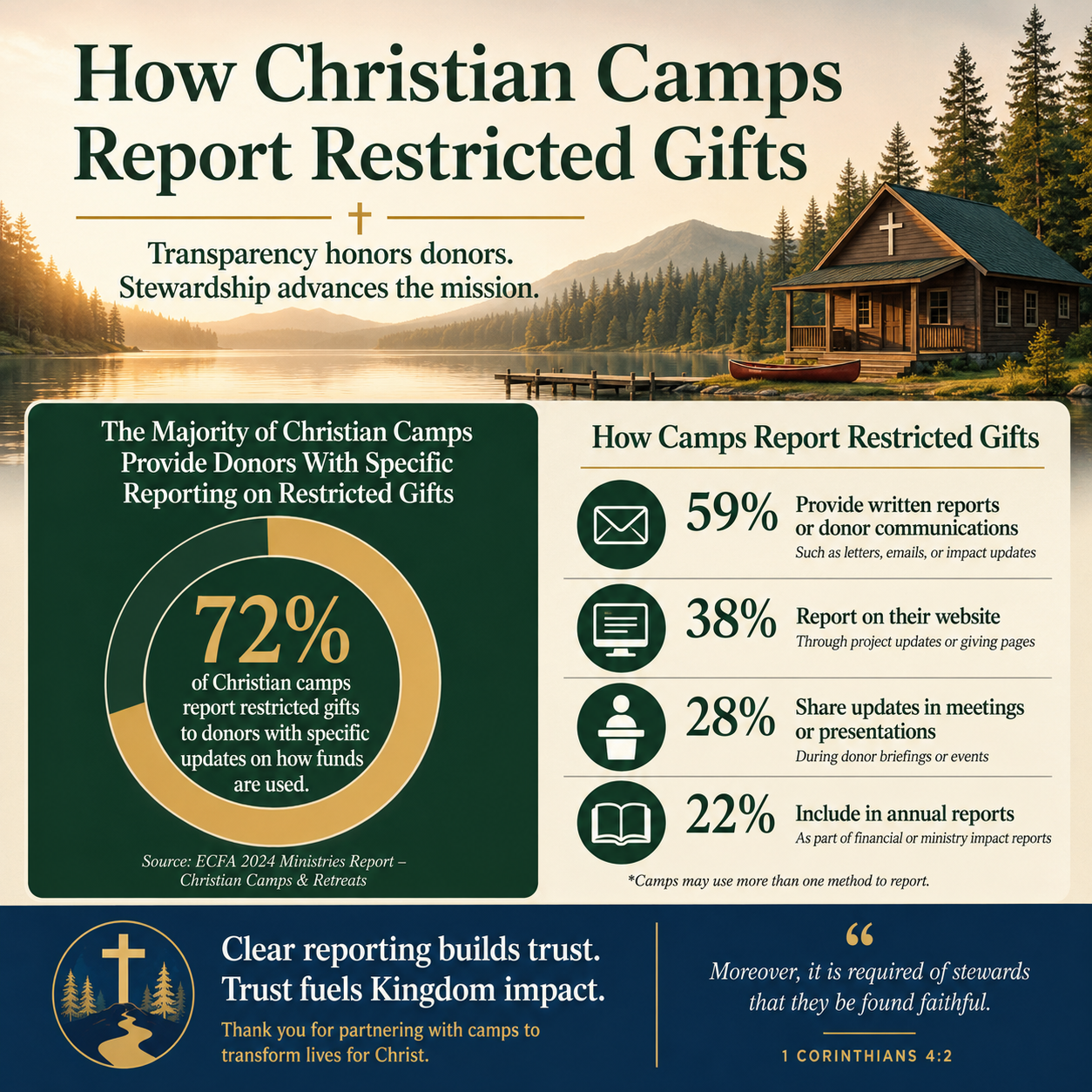

How Christian camps report restricted gifts is not a technical question only accountants should worry about. For donors, it is one of the clearest windows into whether a camp treats sacred trust as sacred—whether it will honor a gift’s purpose, tell the truth about what it can and cannot do with designated funds, and resist the quiet temptation to cover operating gaps with money that was never meant for them.

Summer ministry is inherently seasonal. Payroll, food service, insurance, transportation, waterfront safety, and facility upkeep rarely move in a straight line. That financial pressure is exactly why clear reporting matters. When restricted gifts are recorded and disclosed with integrity, donors can give boldly without subsidizing confusion. When reporting is vague, even faithful givers begin to wonder whether “camperships” or “capital improvements” are serving as donor-facing labels for general need.

Restricted gifts are a promise before they are a line item

Restriction is donor intent, not internal preference

A restricted gift is money given for a specific purpose, time period, or project. The restriction is not created by the camp’s budget; it is created by the donor’s designation (or a grant agreement) and accepted by the ministry when it receives the gift. In Christian ethics, that acceptance carries moral weight. “Moreover, it is required of stewards that they be found faithful” (1 Corinthians 4:2). Faithfulness is not measured only by outcomes, but by whether a ministry keeps its word.

In practice, camps commonly receive restrictions for camperships, program expansions, specific retreats, staff missionary support, vehicles, waterfront equipment, and capital projects. Many of those are good and necessary. The harder question is whether the camp has the internal discipline to track restrictions in a way that does not blur into the operating account when cash gets tight.

What accounting standards require and what donors should expect

In the United States, most Christian camps report under U.S. GAAP for nonprofits. The core framework for how nonprofits classify net assets is the FASB Accounting Standards Codification 958, which requires organizations to present net assets with donor restrictions and without donor restrictions. Donors can review the primary standard setter’s explanation at FASB.

What this means in practice is straightforward: restricted gifts should not be reported as unrestricted revenue simply because they have been deposited. They should be recorded with their restriction, and released to unrestricted only when the restriction is satisfied (for example, when campership awards are actually granted, or a building phase is completed in accordance with the restricted purpose).

What a transparent camp reports and where donors can verify it

The basic financial statements that carry the truth

Most donors do not need to become auditors, but donors should know where restricted gifts show up. In audited financial statements, the story is usually told across three places: the statement of financial position (balance sheet), the statement of activities, and the notes. If the camp is large enough to file a Form 990, donors can often see similar categories and disclosures there as well.

For camps that file Form 990, the IRS requires the organization to report net assets with donor restrictions and to reconcile them. Donors can confirm the reporting framework at IRS Charities and Nonprofits. A camp may describe restricted categories in Schedule D or within attachments, but the most meaningful clarity usually comes from audited notes that explain major restrictions, the timing of release, and the nature of any endowments.

Signals of mature reporting

Across our verification work at Most Trusted, the ministries that meet The Most Trusted Standard tend to treat restricted-gift reporting as a routine discipline, not a donor-relations performance. They are not afraid to name complexity, such as multi-year pledges, cost overruns, and seasonal cash-flow pressure, because their accounting and governance are built to carry those realities without quietly shifting restricted funds into general use.

Several donor-visible signals often accompany that maturity:

- Audited financial statements are posted, current, and complete, including notes.

- Net assets with donor restrictions are not presented as an embarrassment but explained plainly.

- Major campaigns include periodic accounting of funds received, funds spent, and remaining restricted balances.

- Campership reporting distinguishes between funds raised, awards granted, and timing differences.

- The board receives regular reports that compare restricted balances to planned uses and timelines.

Donors who want a broader map of how camps should operate can orient themselves through Christian Camps and Conferences, where we address the governance and reporting patterns that most consistently separate trustworthy ministries from merely compelling ones.

Common camp scenarios where restricted reporting goes wrong

Camperships and the temptation to count promises as impact

Campership funds are among the most donor-loved restrictions because they connect directly to access and discipleship. The accounting challenge is that “camperships” can be used loosely to describe several different realities: a restricted scholarship fund, a general discount policy, or a fundraising appeal meant to offset overall pricing.

A camp can report with integrity by distinguishing (a) restricted campership gifts received, (b) campership awards granted to campers, and (c) the actual timing of when those awards reduce revenue. If campership gifts are restricted but not yet spent, they should remain in net assets with donor restrictions, not treated as a general subsidy for operating costs.

Capital projects and quiet reclassification

Building projects are another frequent pressure point. Donors give for a dining hall, cabins, a ropes course, or accessibility improvements, and they expect the camp to spend accordingly. Problems arise when projects stall, costs rise, or permitting delays drag on, and leadership begins to treat restricted construction dollars as a bridge loan for operations.

In strong reporting, restricted capital gifts are tracked by project, with clarity about whether they are purpose-restricted, time-restricted, or both. If a donor gives “for the new cabins,” the camp should not treat that as a general facilities bucket unless the donor explicitly agrees to broaden the purpose in writing.

Designated versus restricted and why the distinction matters

Some camps use the word “restricted” when they mean “board-designated.” A board can set aside unrestricted money for future facility renewal, a rainy-day reserve, or strategic initiatives. That can be prudent stewardship. But board designations are not donor restrictions. They can be changed by board action, and they should not be marketed to donors as though they carry the same binding constraint.

Donors should expect a camp’s financial notes or internal summaries to be precise with terms. When language gets fuzzy, it often signals that internal controls are also fuzzy.

How to read restricted-gift reporting without becoming an accountant

Questions that surface integrity quickly

Donors can ask for a camp’s most recent audited financial statements and, if applicable, its Form 990. A camp that handles restricted gifts well will usually provide these without defensiveness. When reviewing, focus on whether the story hangs together: do the restrictions described in appeals and donor communication match the categories and movements in financial reporting?

These questions tend to be especially revealing:

- What are the largest categories of net assets with donor restrictions, and what are they for?

- How much was released from restriction this year, and what activities satisfied the restrictions?

- Are any restricted funds older than two or three years, and if so, why are they not yet used?

- Does the camp ever borrow internally from restricted funds for cash-flow timing, and what safeguards exist?

- How does the board oversee restricted funds and campaign accounting?

Seasonality is a real constraint, and donors should not confuse “cash is tight in February” with wrongdoing. The ethical issue is not the existence of pressure; it is whether the camp treats donor intent as inviolable under pressure.

When restrictions cannot be met

Camps sometimes face situations where a restriction becomes impracticable: a program is discontinued, a property purchase falls through, or a regulatory change makes a planned facility impossible. GAAP and charity law both recognize that donor intent must still be honored; the answer is not to quietly reclassify the funds as unrestricted.

In these cases, trustworthy ministries pursue a documented path: seeking donor consent to redirect funds to a closely aligned purpose, or, when donors cannot be reached and the sums are significant, pursuing appropriate legal remedies under state law. The donor deserves to be treated as a partner in truth, not a revenue source to be managed.

For donors who want more context on what financial clarity should look like within a broader accountability framework, we address the relevant expectations in Accountability and Transparency in Christian Camps and Conferences.

What Most Trusted looks for when restricted gifts are part of the risk profile

Restricted funds are a transparency test, not merely a finance test

Restricted gifts touch multiple dimensions of trust at once: theology of stewardship, internal controls, board governance, and external reporting. Under The Most Trusted Standard, we pay attention not only to whether restricted gifts are technically recorded, but whether the organization’s public communications and internal practices align with the financial statements.

When camps struggle in this area, it is often not because leaders are indifferent to integrity. It is because the organization has grown faster than its finance function, or because seasonal operations have normalized a pattern of “we will fix it after summer.” Donors should not confuse operational intensity with an exemption from accountability. Scripture does not treat busyness as a moral defense.

Practical markers that restrictions are being honored

In credible camp operations, several governance and reporting markers tend to cluster together:

- Written gift-acceptance policies that define what restrictions the camp can and cannot accept.

- Fund accounting practices or equivalent tracking that tie restricted gifts to specific uses.

- Separation of duties and review controls that make misclassification difficult to hide.

- Clear campaign reporting that distinguishes commitments, cash received, and expenditures.

- Board minutes and finance committee oversight that reflect active governance, not rubber-stamping.

Donors should also recognize the legitimate tension camps face: sometimes the most pressing need is unglamorous—insurance premiums, food costs, maintenance backlogs, staff retention. If donors restrict heavily and consistently, leadership may feel forced into contortions. The honest remedy is not accounting creativity; it is candid communication about unrestricted need, paired with disciplined reporting that honors restricted gifts precisely because they are restricted.

FAQs for How Christian camps report restricted gifts

Should a camp ever use restricted gifts to cover operating expenses if it plans to repay them?

As a rule, donors should view that practice as a serious warning sign. Internal borrowing from restricted funds is not a normal feature of healthy nonprofit controls, and it can easily become a habit that is functionally indistinguishable from misuse. If a camp claims it does this, donors should ask for written board policy, documented approvals, repayment timelines, and how the practice is disclosed in audited financial statements.

If a donor gives to a camp’s building campaign, can the camp use the gift for general facilities maintenance?

Only if the donor’s restriction was written broadly enough to include that purpose, or if the donor later provides explicit written consent to broaden or redirect the gift. A “building campaign” is a fundraising label; the binding constraint is the actual donor intent as documented in the gift instrument, solicitation language, or correspondence. Trustworthy camps treat that documentation as determinative.

Stewardship that can be tested

Donors are not asking Christian camps to achieve perfection in complex operations. Donors are asking for faithfulness that can be examined: reporting that tells the truth, governance that resists quiet exceptions, and accounting that keeps promises made in God’s name. When a camp reports restricted gifts with clarity—showing what was received, what remains restricted, and what has been released for the purpose intended—it honors both the donor and the Lord who sees every stewardship in full light.